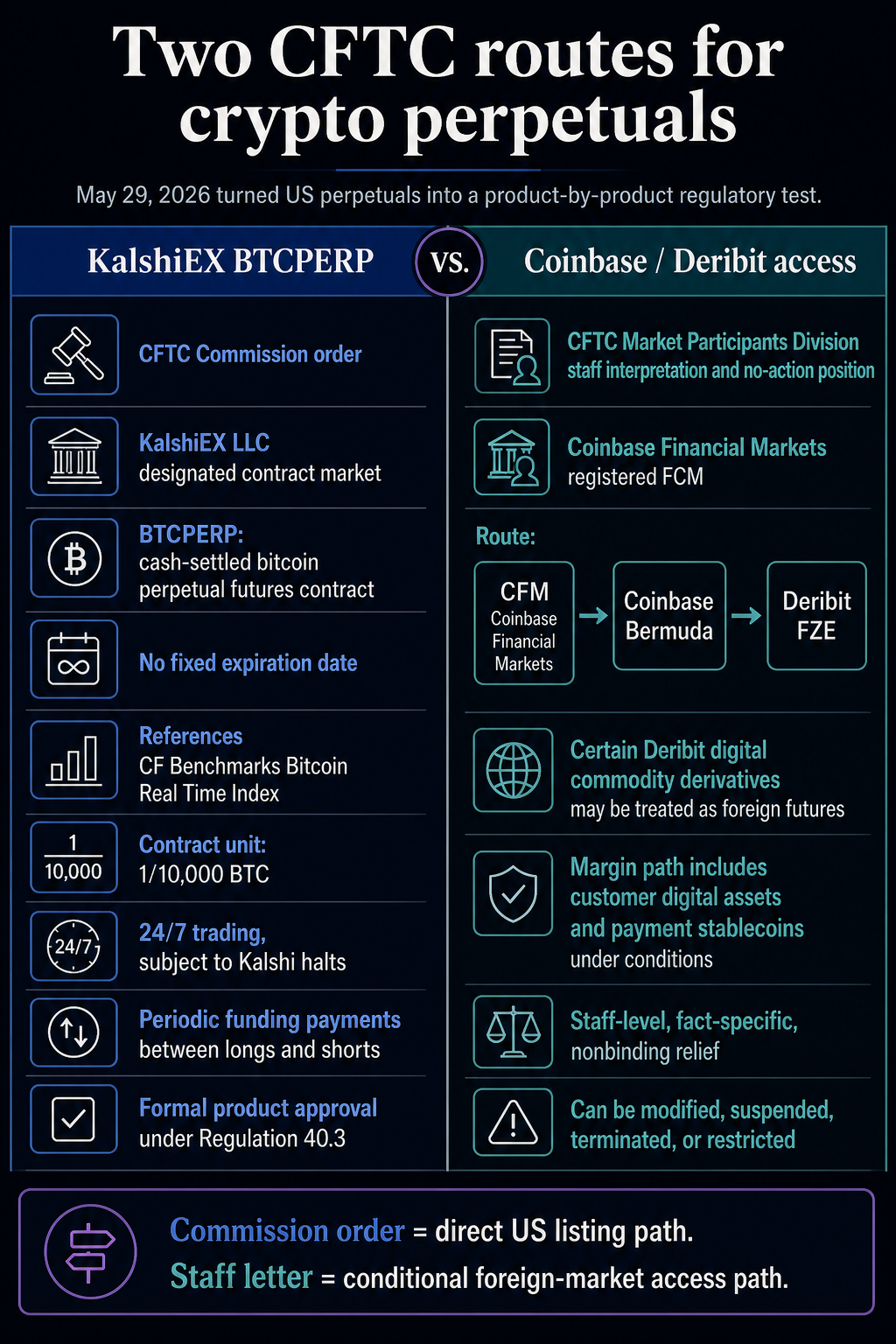

CFTC moves true Bitcoin perpetual futures from offshore liquidity debate to US regulatory test case, KalshiEX LLC is approved to list on BTCPERP, and Coinbase Financial Markets receives individual staff-level relief for access to certain Deribit products.

The European Commission has approved KalshiEX LLC’s BTCPERP contract as a futures contract, allowing a CFTC-registered designated contract market to list perpetual Bitcoin perpetual trading linked to the spot price of BTC.

In another move on the same day, CFTC staff confirmed that certain Deribit digital product derivatives described by Coinbase Financial Markets may be treated as foreign futures when routed through Coinbase’s registered futures fee merchant structure.

Chairman Mike Selig positioned the Kalsi order as a fulfillment of the promise of a domestic crypto asset perpetual motion machine and a pathway for one of the most liquid market segments of cryptocurrencies to exist within the US regulatory framework.

Together, these actions transform the US perpetual motion debate from a theoretical onshoring promise to a test of actual market structure. One method involves placing your Bitcoin Permanent Bits directly on a US-regulated exchange. The other provides Coinbase with a conditional staff-level route for U.S. customers to obtain global cryptocurrency derivatives liquidity through affiliates of CFM, Coinbase Bermuda, and Deribit.

The industry response leans toward market access points and illustrates how public companies and exchanges view the same CFTC actions differently.

CFTC guidance advances Bitcoin capital markets, including 24/7 trading, BTC collateral, perpetual futures, options, and regulated access.

Michael Saylor connected this guidance to Bitcoin holders and MicroStrategy’s extensive Bitcoin-backed credit strategy. Coinbase CEO Brian Armstrong highlighted the customer access angle and global market size that US users have not previously been able to reach through regulated domestic channels.

Until now, US users were locked out of about 80% of the global cryptocurrency market.

Those reactions are useful market context. Legal boundaries remain in CFTC orders and staff letters.

This distinction is central to market implications. Perpetual futures are one of the most frequently traded instruments in cryptocurrencies because they allow traders to hold directional exposure without rolling out expiring contracts. The regulatory question is whether the structure can comply with U.S. futures rules while limiting the leverage, liquidation and collateral risks that have made offshore companies so dominant and so volatile.

2 routes open simultaneously

Kalsi’s approval carries different legal weight because it is a commission order. The CFTC issued an order pursuant to Section 5c(c)(4) of the Commodity Exchange Act and Commission Rule 40.3, determining that listing BTCPERP as a futures contract is consistent with the CEA and the Agency’s rules.

The CFTC’s announcement says Mr. Kalsi filed the contract on May 29th, but the order specifies the filing date as May 28th, and the approval itself is dated May 29th.

Coinbase’s path is different. The CFTC’s Division of Market Participants has issued an Interpretation and No Action Position against Coinbase Financial Markets. Staff stated that the Deribit products described in the request may be classified as foreign futures under Regulation 30.1.

Staff also said they do not recommend enforcement actions under certain conditions related to customers’ digital assets or payment stablecoins pledged as margin through Coinbase affiliates.

| path | regulatory measures | Content covered | legal weight | main limit |

|---|---|---|---|---|

| KalshiEX BTCPERP | CFTC Commission Order | Cash-settled Bitcoin perpetual futures contract listed by DCM | Formal product approval under Regulation 40.3 | Case-by-case reasoning related to market depth and contract design like Bitcoin |

| Coinbase / Deribit Root | CFTC Staff Interpretation and No-Action Position | US customers can access certain Deribit digital commodity derivatives through CFM | Staff-level, fact-specific, non-binding relief | Conditional structure including Coinbase affiliates, foreign futures rules, and margin collateral safeguards |

This division determines durability and range. Calciroot will test whether U.S. exchanges can directly list perpetual securities under CFTC product approval. The Coinbase route will test whether registered FCMs can provide U.S. customers with supervised access to Foreign Trade Commission products while meeting conditions regarding margins, disclosure, and affiliate management.

Coinbase says onboarding for institutional investors can begin now, with Deribit options live through CFM, and perpetual futures to follow. According to the company, it is expected to have wide access in the future, including to retail stores.

Kalsi’s launch notes describe the product as the first perpetual product in the United States, and state that U.S. investors will soon be able to access CFTC-regulated crypto perpetual futures on its platform. The company also said it aims to launch permanent cryptocurrency issuance in more than a dozen currencies pending regulatory review.

What the CFTC has approved regarding Karshi

Kalsi’s order describes BTCPERP as a cash-settled derivative that references the USD spot price of 1 BTC as measured by the CF Benchmark Bitcoin Real-Time Index. The contract is traded in units of 1/10,000th of a Bitcoin and can be traded 24 hours a day, 365 days a year, subject to Karshi’s trading suspension.

Its feature is that there is no fixed expiration date. Traditional futures converge to the spot at expiration as delivery or final cash settlement pulls the contract into the underlying market. Perpetuals have no final settlement, so the convergence mechanism must operate continuously.

According to the CFTC order, BTCPERP will make periodic fund payments between long and short holders based on the difference between the contract’s mark price and the underlying reference price.

If the contract trades above the spot, the longs pay the shorts. If the stock trades below the spot price, the short pays the price of the long. Payment pressure gives traders an economic incentive to push the permanent price back towards the Bitcoin reference price.

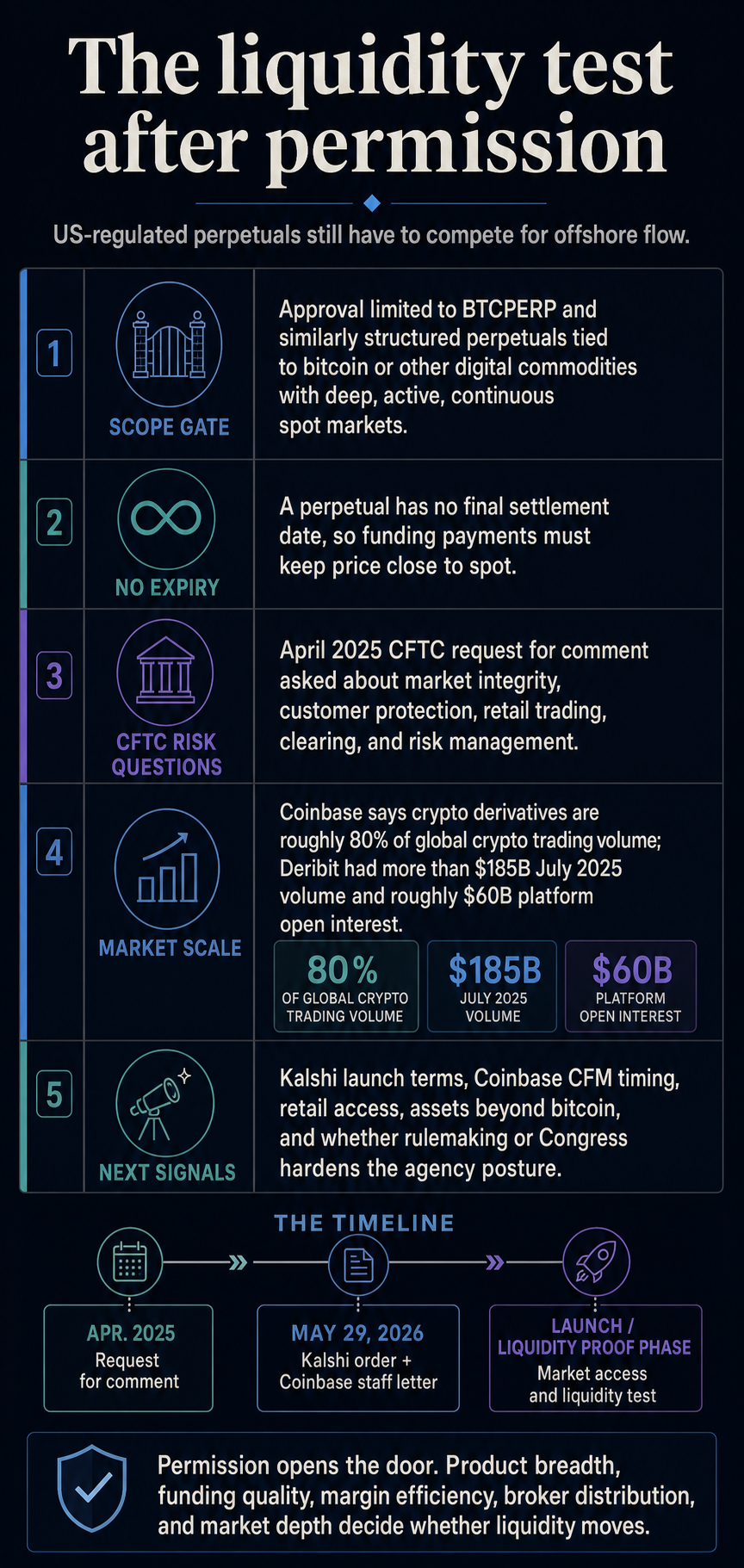

The agency’s reasoning relies heavily on Bitcoin’s market structure. According to the order, Bitcoin will be traded continuously in widely distributed venues and a reference price will be observable while contracts are traded. It also points to Bitcoin’s deep, active and continuous spot market and 24/7 spot trading that arbitrageurs can accommodate while making perpetual trades.

The order is therefore consequential and limited. The CFTC said its analysis was limited to BTCPERP and similarly structured perpetual contracts that reference deep, active, ongoing spot market trading that references Bitcoin and other digital instruments. Other asset classes are excluded from the analysis and contract classification remains on a case-by-case basis.

Novelty warnings emphasize legal significance. According to CFTC product records, a Bitnomial product labeled perpetual futures was certified in May 2026, and Coinbase Derivatives previously applied for a nanoBitcoin purpstyle futures product with a long-term expiry of December 2030.

igcurrencynews covered Coinbase’s 2025 Perp-style launch in the US and then noted that Perp with no true expiry date is different from the long-standing workaround.

Practical takeaway: While Kalshi officially received CFTC approval for Bitcoin Perpetual Bitcoin with no true expiry date, Coinbase received another staff-level route for access to global derivatives. This paves a concrete path for U.S.-regulated permanent storage, with subsequent approvals still tied to product design, market depth, and the agency’s current stance.

Why Coinbase remains part of the story

Coinbase’s action is less durable than a committee order, but could create short-term market access because it connects U.S. customers to Deribit, an exchange that Coinbase data shows has high trading volume and open interest.

Coinbase said crypto derivatives account for about 80% of global crypto trading volume, and U.S. customers lack a regulated route to access much of that liquidity. In an update to investors following the completion of the Deribit acquisition, Coinbase said Deribit had trading volume of more than $185 billion in July 2025 and approximately $60 billion in open interest on the platform.

The CFTC staff letter is technical because the route is technical. CFM is a registered FCM. It will provide customers with access to certain digital commodity derivatives listed on Deribit FZE, which the letter describes as affiliated with the Foreign Trade Commission.

Customer orders are transferred to Deribit via our affiliated overseas broker Coinbase Bermuda Limited.

Staff also worked on treating the margins. No-action positions cover certain situations where a CFM posts customer-owned digital products and settlement stablecoins to a foreign broker affiliate to provide margin on foreign futures and options positions, even if the foreign broker has the right to reuse those assets.

This relief is tied to conditions such as Coinbase’s ownership links, disclosures, operational controls, authorizations, and use of Customer Digital Assets solely for the purpose of securing margin or customer obligations.

This helps Coinbase’s pass with distribution and reach while leaving a thinner upfront footprint than Karshi’s orders. This illustrates how the staff can address foreign market access issues while preserving the Committee’s ability to review interpretations.

This distinction is practical for venues, brokers, and customers because it impacts who can trust the signal and how quickly access to the product can expand.

The legal status of staff letters is subject to conditions. Its positions represent only the Market Participant Division, are not binding on the Commission or other CFTC staff, and may be modified, suspended, terminated, or limited depending on the facts presented.

Next is the liquidity test

The CFTC has been working toward this moment for more than a year. In April 2025, the agency’s request for comment asked about perpetual derivatives, including their uses, benefits, risks, market integrity issues, customer protection issues, retail trading, clearing, and risk management.

The move also fits in with broader efforts in the United States to adapt regulated derivatives plumbing to the always-on market for cryptocurrencies. igcurrencynews previously covered CME’s move towards 24/7 crypto futures and options, another attempt to reduce the discrepancy between traditional market hours and the continuously traded crypto spot market.

The agency currently has two working models on the market. One is a domestic exchange product approved by the European Commission, and the other is a foreign futures access pass through a staff-approved registered FCM. Both could help draw persistent activity to monitored US channels. Liquidity needs to continue.

Those questions remain unanswered. Regulated exchanges must offer sufficient product breadth, margin efficiency, funding quality, and broker distribution to compete with offshore exchanges. If Kalsi’s BTCPERP launches with competitive funding and access terms, and Coinbase is able to expand access to Deribit from institutions to a wider range of customers, some flows could shift to channels that the CFTC can monitor more directly.

If the product remains limited, expensive, or operates more slowly than offshore venues, this approval may carry more weight as a regulatory precedent rather than as an immediate liquidity shift.

The next signal is realistic. The terms of KALSI’s launch, the timing of perpetual futures through Coinbase’s CFM, the treatment of retail access, what assets the CFTC will allow beyond Bitcoin, and whether formal rulemaking or Congress will later change the agency’s stance to one that is difficult to reverse today.

(Tag translation) Bitcoin