Bitcoin is trading below $78,000 as weak demand from U.S. spot exchange-traded funds (ETFs) collides with an accumulation of leveraged positions that could deepen the sell-off if key support levels fail.

data from crypto slate The largest digital asset was shown trading around $77,400 after briefly topping $82,000 earlier this month. Traders weighed speculation about a possible US-Iran deal and its impact on risk assets, retreating on the back of a more cautious macro environment.

However, market analysts point out that there are serious structural imbalances within crypto exchanges that could dictate Bitcoin’s near-term trajectory.

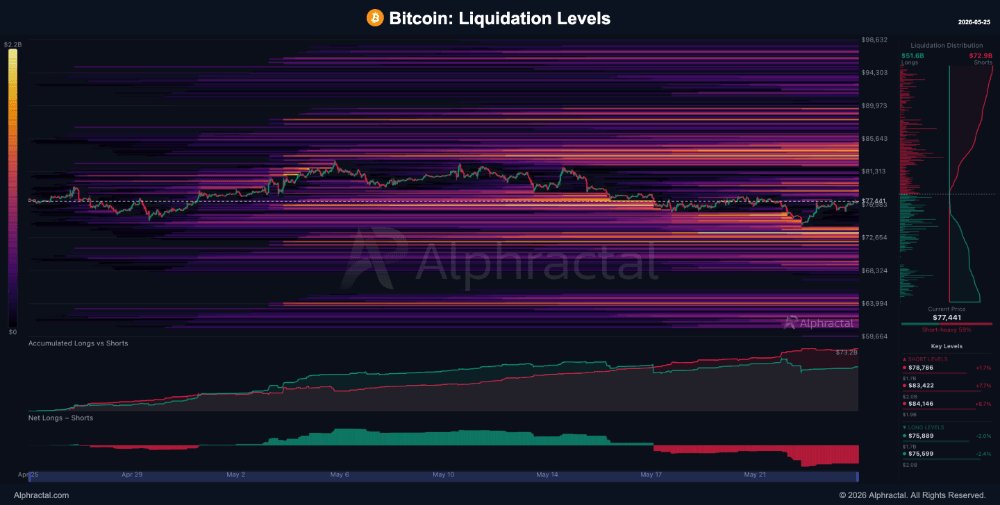

Alpharactal data shows that there is approximately $14.3 billion of potential liquidation pressure around Bitcoin’s current levels.

The company said the total is divided into bullish and bearish positions, but the distribution is uneven. Long-term liquidations are concentrated in a range below the current spot level, while short-term liquidations are spread over higher price levels.

Liquidation pressure increases below spot

The most pressing risks are in the derivatives market, where long leveraged positions have accumulated around several downside levels.

According to Alphactal’s Aggregated Liquidation Heatmap, static long liquidity stands at $1.61 billion at around $73,716, and the cumulative amount rises to $3.85 billion at around $73,281.

This volume grows rapidly, reaching $5.42 billion at $72,702, and $7.14 billion when assets reach $72,122.

This structural setup means that a 6% to 7% decline could trigger an intensive liquidation cascade, as exchanges automatically sell the underlying assets to close leveraged accounts.

In contrast, pressure from short sellers is significantly less concentrated. A rise to $78,786 would result in the liquidation of $1.66 billion of short positions, but subsequent thresholds are further apart.

The cumulative short interest will not reach $3.68 billion until the price reaches $83,422, and it would need to rise to $88,202 to liquidate $7.20 billion of short interest.

Market analysts have observed that this particular structure typically results in downward price movements accelerating faster than upward recoveries, as dense long positions create localized pockets of forced selling.

In fact, leveraged longs have already suffered most of the recent damage. Over the weekend, crypto slate Long traders reported losing about $870 million as the price of Bitcoin briefly dipped below $75,000 for the first time since mid-April.

ETF outflow weakens institutional bids for Bitcoin

This leverage risk is amplified by the apparent lack of spot market demand to absorb potential selling.

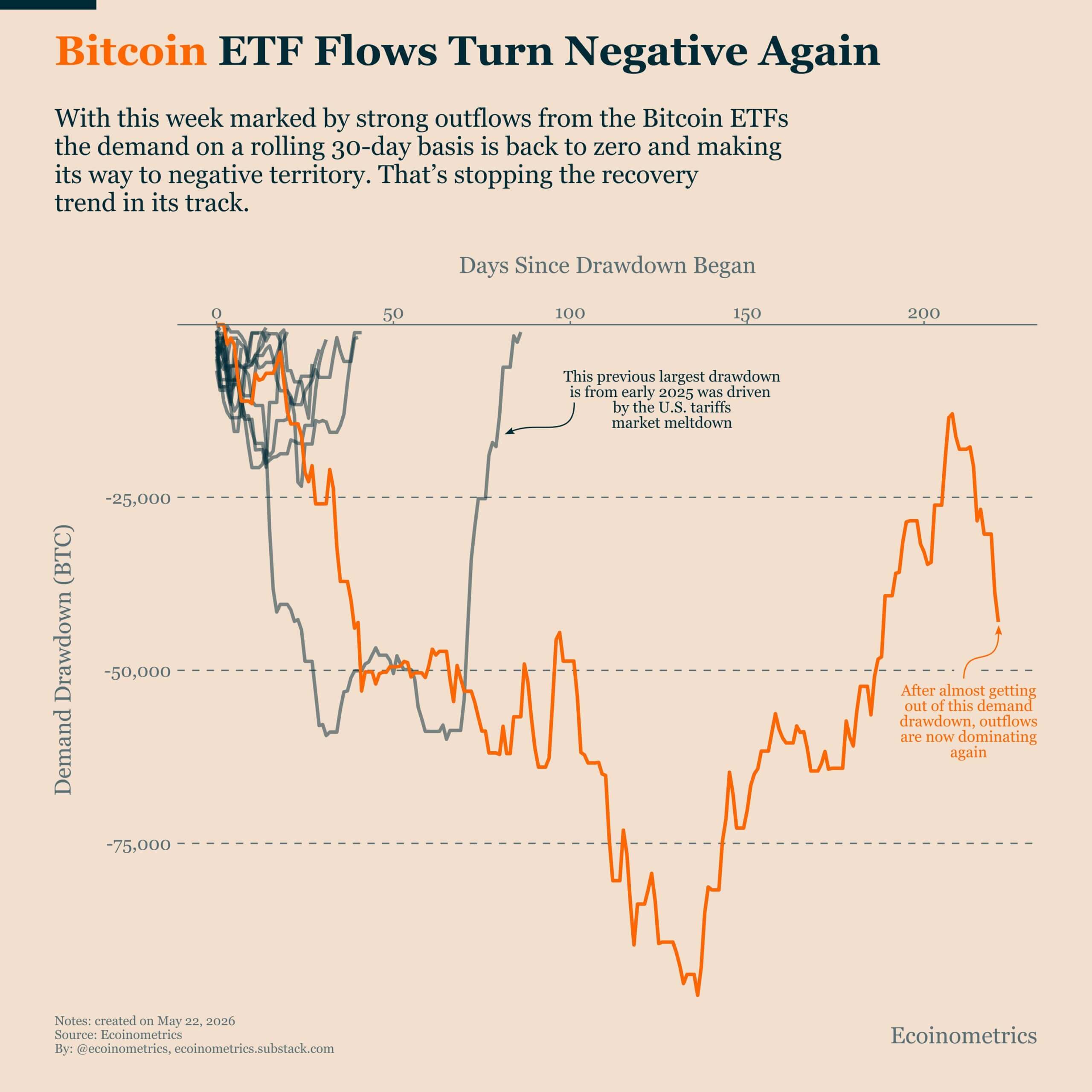

This is evidenced by the US Spot Bitcoin ETF, which recorded net outflows of approximately $2.26 billion in two weeks after Bitcoin briefly topped $82,000. Withdrawals caused ETF holdings to decline again, interrupting the recovery that had helped stabilize the market.

Ecoinometrics, a Bitcoin-focused analytics platform, said demand trends remain subdued, even though the Bitcoin price has not yet fully corrected.

The firm said 30-day ETF flows have returned to negative territory, indicating that institutional demand is no longer providing the support seen during previous rallies.

ETF flows have been one of the clearest measures of marginal demand for Bitcoin since the fund’s inception. When there is high inflow, it provides stable spot buying and helps absorb selling from traders and miners. If capital outflows continue, the market loses a large cushion.

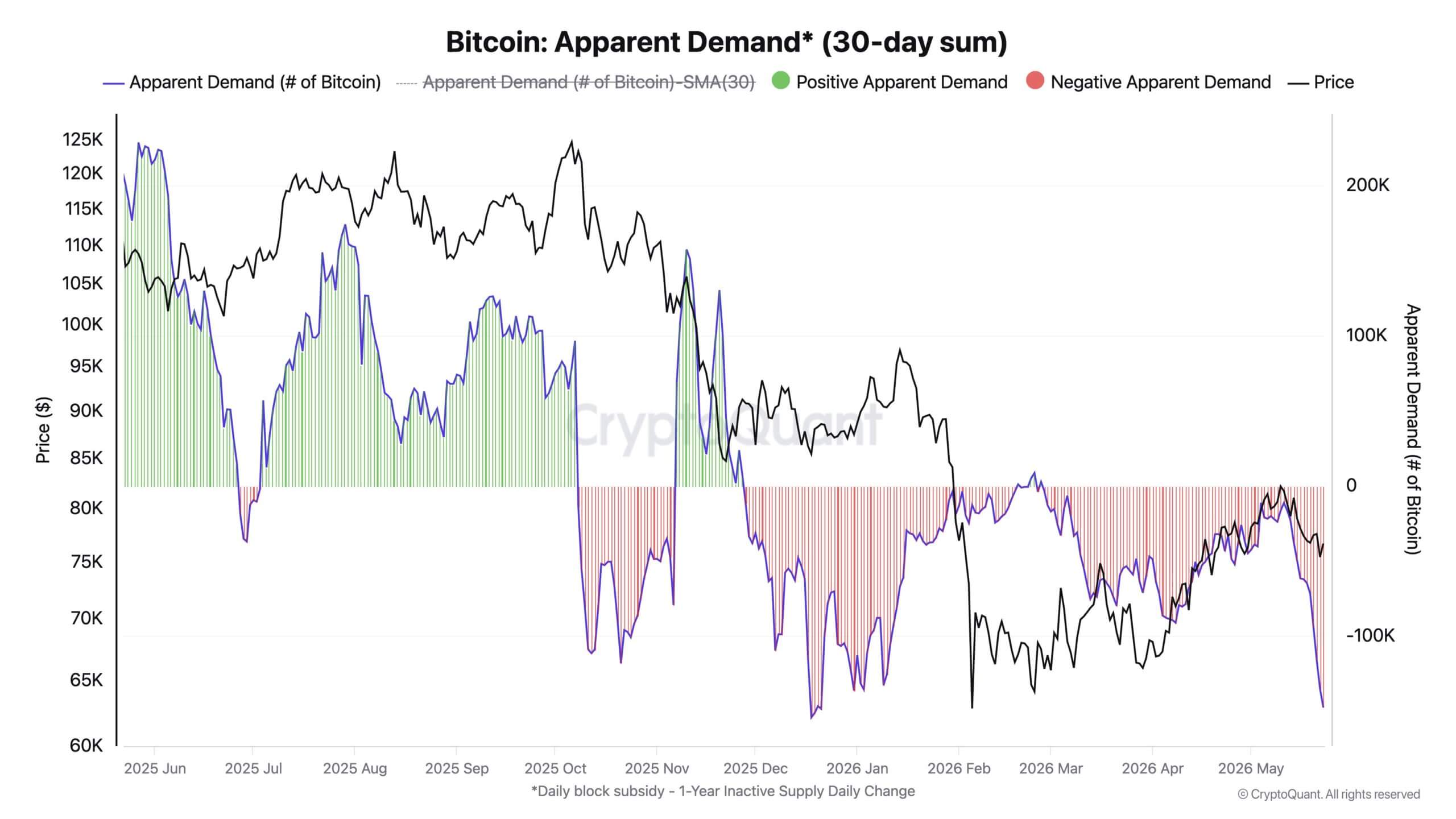

This institutional decline is reflected across broader on-chain demand metrics.

According to data provider CryptoQuant, Bitcoin’s “apparent demand” has plummeted to -147,000 BTC, its lowest level since the beginning of the year. This metric compares new Bitcoin issuance with supply that has been inactive for more than a year and provides a way to estimate whether long-term accumulation is strong enough to absorb new supply.

The data reflects an uncomfortable reality for digital asset bulls. While derivatives and futures speculation can amplify short-term upward momentum, a sustainable and durable bull market requires true spot accumulation. Without it, the market lacks a solid foundation.

Compounding this lack of demand is the steady depletion of stablecoin liquidity. CEX.io noted that the exchange’s stablecoins have recorded an average daily net outflow of -$332 million over the past week.

This indicates that sideline capital, the digital dollar liquidity that traders typically use to buy market dips, is being actively drained from trading platforms. As a result, the market becomes highly vulnerable to supply shocks.

Short-term holders lose their profit cushion

Short-term investors are bearing the brunt of the pain as capital leaves the ecosystem.

Short-term Bitcoin holders went from modest gains to rock bottom in less than seven days, according to a May 25 note from CEX.io. Short-term BTC holders are defined as entities that hold coins for less than 155 days.

The company said the group’s realized P&L profile deteriorated at a similar pace to that seen during the stressful weeks of January and February.

Notably, this group of investors often reacts quickly when prices fall below their cost basis. This is because they typically have less tolerance for drawdowns than long-term holders and are more likely to sell when they fail to rebound or when losses increase.

More importantly, a fundamental structural change has occurred in the chart. Bitcoin’s short-term holder cost standard has fallen below the asset’s “true average price,” which is the anchor for long-term valuation.

Historically, this particular technological crossover has served as a significant macro warning pattern. In previous market cycles, this very event occurred in the midst of a broad bear market and served as a direct precursor to a significant decline.

A similar crossover occurred in 2014, before a 20% weekly decline. 2018 saw a 21% weekly decline. In 2022, that signal preceded a 34% weekly decline.

Volatility has decreased in the current cycle, making a repeat of this move less likely. However, this signal still shows that recent buyers are submerged relative to long-term valuation metrics.

Support may weaken as the price decline causes more holders to suffer losses and increases the risk of further selling.

If the historical pattern repeats more fully, Bitcoin could face pressure towards the $60,000 area. Unless buyers return to the high $70,000 range soon, the market will remain fragile even with a benign outcome.

Whale purchases provide a counterweight

Despite the overall bearish indicators, there is a clear disconnect between the institutional retail channel and long-term crypto natives.

Although the Crypto Fear and Greed Index is in “panic” territory at 28, large BTC holders known as whales are actively taking advantage of this discount.

CEX.io noted that these long-term holders added approximately 30,000 BTC last week, extending an accumulation trend that had been going on for several months.

Although the pace has slowed from last week’s roughly 80,000 BTC and the large additions seen in April, this direction still indicates some long-duration investors are buying bearishly.

Alphactal also cited on-chain cohort data showing that addresses holding at least 1,000 BTC have accumulated 47,000 BTC in the past 14 days.

Evidence of this can be seen through BTC treasury company Strategy, which added 24,869 BTC last week for approximately $2.01 billion at an average purchase price of $80,985.

Whales appear to view Bitcoin’s current decline as a mechanical, programmatic portfolio rebalancing rather than a fundamental rejection of cryptocurrencies.

Much of this contrarian optimism is tied to legislation in Washington, where U.S. lawmakers recently pushed through the CLARITY Act. This is a bill widely expected to provide definitive regulatory guardrails for digital assets in the United States.

Essentially, Urge buyers are effectively betting that the bill’s prospects will eventually reverse short-term spot market weakness.

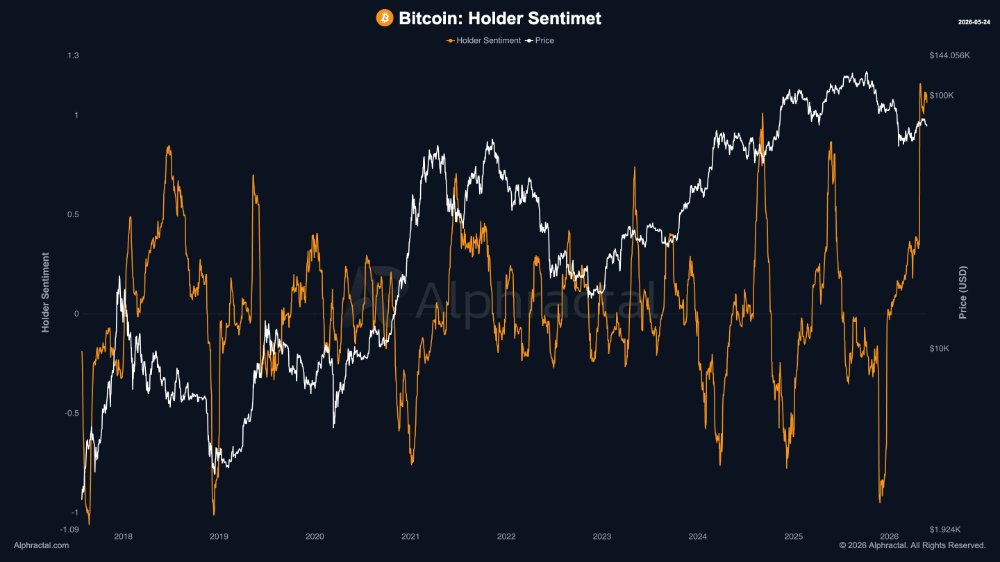

This optimism is not surprising given that the underlying sentiment indicator, which weights investor confidence by holding period, has increased to 0.82.

Historically, during retail panics when the Fear and Greed Index is below 30, when this index crosses the 0.80 threshold, it indicates that the bottom of the business cycle is near.

The last time this exact setup occurred was in March 2024, after which Bitcoin rose 67% over the next 90 days.

What Bitcoin Traders Are Watching Next

In the short term, Bitcoin’s path of least technical and structural resistance appears to be biased to the downside.

Funding rates in the derivatives market have turned slightly positive, indicating that the aggressive short positions that prevailed throughout the spring have been fully unwound.

While this sounds positive, it eliminates the possibility of a “short squeeze” as a short-term upside factor.

Bullish traders will face a tough uphill battle to regain control and stabilize the market.

BTC buyers will need to quickly move the spot price above the double resistance line of the short-term holder cost basis and the true average price (both currently converging around $78,000). Success here would open the door to testing the all-important 200-day moving average of $80,000.

However, if this overhead resistance cannot be asserted in the coming days, the macro technical picture is likely to darken, potentially reinforcing the deeper correction signaled by the historical cycle.

For market bears, the immediate target remains $74,500, where the 128-day moving average is located.

A clean and decisive break below this support level would strip Bitcoin of its last line of near-term defense, activating a compressed liquidation trap of $14 billion below it, and likely re-establishing severe downward momentum not felt by the market since February.

(Tag translation) Bitcoin