Bitcoin’s Iran deal rally based on renewed optimism in the US-Iran deal is a reliable primary macro signal. Oil flows, gasoline prices, inflation compensation, and Fed pricing decisions still need to be confirmed for traders to treat this move as a path back to rate cuts.

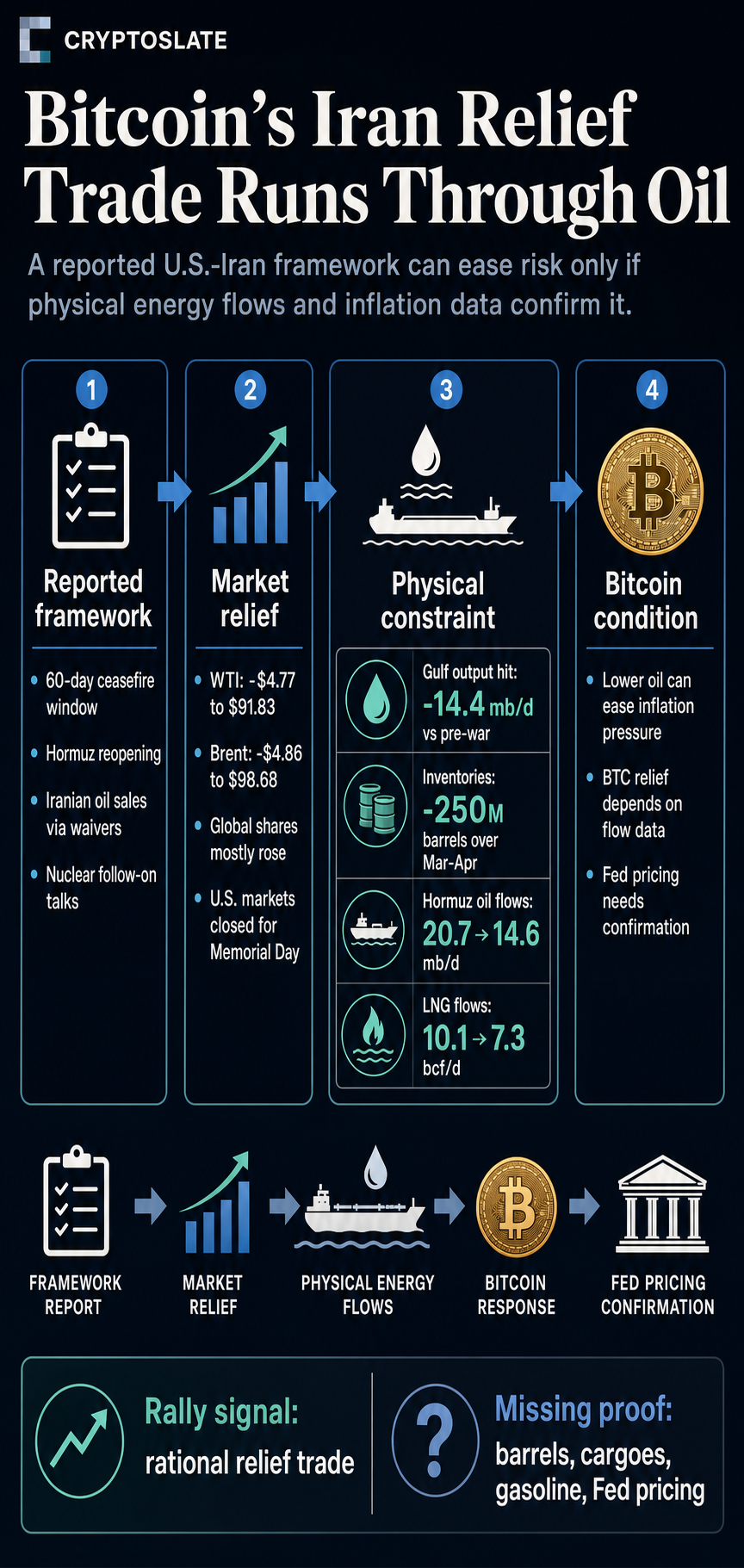

The immediate market logic is simple. The reported framework would extend the ceasefire for 60 days, reopen the Strait of Hormuz, allow Iranian oil sales through sanctions waivers, and potentially bring nuclear concessions into subsequent negotiations.

If this order holds, the war premium for crude oil is likely to fall. Gasoline pressures could ease, inflation could fall, US Treasury yields could fall, and Bitcoin could stop trading like an asset trapped in real interest rate pressures.

The rebound is therefore as much a liquidity signal as it is a geopolitical signal. BTC is trading between $77,400 and $77,500 as of May 25, still well below its October 2025 high of $126,198.

In that context, a large-scale bailout could be triggered if there is a signal that the market is moving away from high oil prices or aggressive Fed policy.

A stronger interpretation is that the market is paying up front for deals whose value depends on facts that are not yet determined, such as physical shipping through the Strait of Hormuz, oil and LNG flows, gasoline pass-through, inflation compensation, Fed communications, and durable nuclear limits.

Oil becomes first rally test for Bitcoin-Iran trade

The fastest reported transmission path from transactions to Bitcoin is through crude oil. Global stocks mostly rose after President Donald Trump said Iran negotiations were progressing, but WTI crude oil fell $4.77 to $91.83 and Brent crude fell $4.86 to $98.68.

With U.S. markets closed for Memorial Day, the move is best read as a reaction to global markets and oil futures rather than an all-out trade in U.S. risk assets. Despite such warnings, the direction was clear: lower oil prices, less immediate inflationary pressures, and more room for risk assets to recover.

Reported deal terms explain the move. The draft framework includes extending the ceasefire, reopening the Port of Hormuz, allowing Iranian oil sales, and starting negotiations to curb Iran’s nuclear program.

A similar outline includes the gradual reopening of waterways, exemptions from sanctions on oil sales, and unresolved details regarding enrichment and nuclear materials.

For Bitcoin, the oil channel is the center of transactions. The asset has spent much of the Iran war period behaving like a liquidity-sensitive risk asset, under pressure from rising energy costs and tighter Fed pricing.

A solid easing of the oil crisis could help cryptocurrencies by reducing the likelihood that policymakers will need to maintain restrictive policies for a longer period of time or respond more hawkishly to a new pulse of inflation.

Therefore, relief rallies are rational and conditional. Initial movements in oil prices suggest to traders that geopolitical premiums could ease quickly once the market sees a path forward for the reopening of the port of Hormuz.

The second movement must be derived from physical energy data and inflation measurements. Without these, the rally remains a bet on execution rather than a definitive macro turn.

This difference keeps market signals locked into the data. Bitcoin could react immediately to futures pricing, but the Fed will need evidence from energy flow and inflation indicators before treating the shock as temporary.

Physical normalization is necessary to save Hormuz

The physical energy background is still large enough that the diplomatic framework still needs to make the oil market work.

The International Energy Agency said Gulf production, affected by the Hormuz closure, was 14.4 million barrels per day below pre-war levels, and observed global inventories fell by about 250 million barrels in March and April.

Oil flows through the Strait of Hormuz have fallen from 20.7 million barrels per day in the fourth quarter of 2025 to 14.6 million barrels per day in the first quarter of 2026, according to chokepoint data from the U.S. Energy Information Administration.

During the same period, LNG flows decreased from 10.1 billion cubic feet per day to 7.3 billion cubic feet per day.

These numbers explain why Hormuz’s reopening instantly registers across risk assets. It also shows the size of the implementation gap.

Oil and LNG flows, Gulf production and inventories need to return to normal before futures price declines signal permanent inflation control.

| distress signal | Why Bitcoin is useful | What still needs to be resolved |

|---|---|---|

| Ceasefire extension and Hormuz reopening | Reduces immediate oil risk premium and supports risk assets | Oil and LNG flows need to be restored with real data |

| Iranian oil sales under exemption | Adds potential supply and reduces pressure on crude oil futures | Exports, sanctions mechanisms and regional security provisions remain implementation risks |

| Nuclear continuity talks | Verifiable concessions could reduce the geopolitical premium | Enrichment limits, uranium removal, testing and duration remain unresolved |

| reduce oil and gasoline pressure | Can ease inflation and real interest rate pressure on cryptocurrencies | April inflation data already shows significant energy pass-throughs need to be reversed |

The good case is clear. Reopening the Port of Hormuz and restoring oil flows will reduce the inflationary impulses weighing on liquidity expectations.

Unresolved cases are equally important. A slow recovery in flows, continued disruptions to Gulf production, or higher gasoline prices will leave the Fed with less room to test market relief trades.

Bitcoin-Iran deal rally goes through Fed rate cut path

Bitcoin is rising because de-escalation could shift the interest rate debate through energy prices. Cooling energy markets could move inflation metrics and inflation compensation away from the worst-case Iran war scenario, making it less likely that the Fed will further delay rate cuts or maintain the risk of rate hikes.

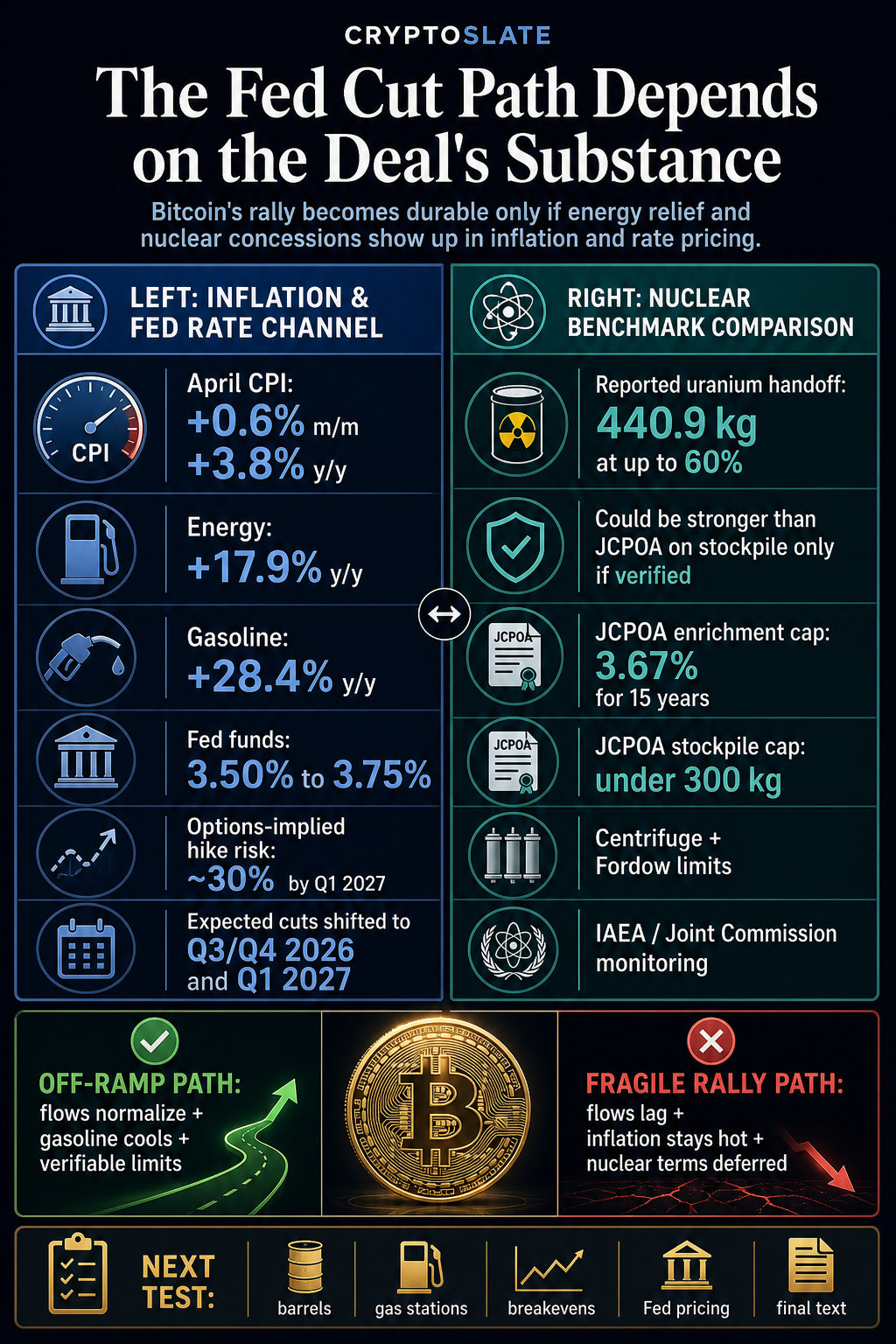

April’s inflation data illustrates that sensitivity. According to the Bureau of Labor Statistics, CPI rose 0.6% month over month and 3.8% year over year, while energy rose 17.9% and gasoline rose 28.4% over the 12-month period.

This is a type of pass-through that converts foreign policy shocks into domestic interest rate pressures.

The Fed was already reacting to this backdrop. The April statement left the federal funds target range unchanged at 3.50% to 3.75%, citing rising inflation that is partly a reflection of global energy prices, and indicating internal tensions over the language of easing.

Minutes from the April meeting said that while expected rate cuts would shift to the third and fourth quarters of 2026 and late in the first quarter of 2027, option pricing suggests a rate hike would occur with about a 30% probability by the first quarter of 2027.

That last point is the crux of the problem with Bitcoin. Cryptocurrencies can more easily absorb geopolitical shocks if they cause interest rates to fall or liquidity to become a focus again.

The company will struggle if the same shock pushes up oil prices, raises inflation compensation, keeps yields high and delays production cuts. On the back of recent Fed minutes, the worst macro twist in the market is already a move away from lower prices to pricing in some rate hike risk.

A deal between the United States and Iran can only reverse that pressure if it changes the path of inflation that inflation data and markets suggest. This will be supported by lower crude oil futures prices. Lower gas prices will further help.

A decline in breakeven inflation and an easing of the Fed’s communication channels would be the strongest signals that the central bank can weather the oil crisis before the 2026 midterm elections.

This sequence of events is why the movement of Bitcoin should be interpreted as a conditional interest rate transaction. Assets could rebound before all geopolitical issues are resolved. Sufficient energy easing is still needed to shift the inflation-to-Fed price balance away from the rate hike risk scenario that has dominated since the April minutes.

Nuclear endurance limits will determine the duration of oil relief

The political battle over whether the reported framework is stronger than the Obama-era Joint Comprehensive Plan of Action has direct market implications for the sustainability of oil risk premiums.

The most defensible answer is specific. If Iran verifiably relinquishes some 440.9 kilograms of uranium enriched to up to 60%, the reported framework could be stronger than the JCPOA in some important respects.

It would directly address near-weapon-grade stockpiles, which did not exist in the same form when the original JCPOA was negotiated.

The reported frameworks remain incomplete as an overall comparison. The JCPOA capped Iran’s enrichment at 3.67% for 15 years, kept the stockpile of enriched uranium below 300 kilograms of 3.67% material, restricted centrifuges, restricted activities at Fordow, and included oversight and dispute mechanisms involving the International Atomic Energy Agency and the Joint Commission.

President Obama touted the deal as reducing Iran’s uranium stockpile by 98% and extending the time for a breakthrough. The Council on Foreign Relations notes that President Trump later withdrew the United States from the agreement after criticizing it as insufficient.

This benchmark fleshes out the current comparison. A 60% handover or dilution of uranium, if verified, would be a meaningful concession.

The pledge to never pursue nuclear weapons is also politically important. However, if enrichment moratoriums, long-term caps, access to verification, duration, and Fordow regulations remain unresolved or non-existent, the market lacks solid evidence that the new framework has removed the risks that drove oil prices higher.

That’s where the Bitcoin rally intersects with political debate. If the final document looks like a ceasefire plus a postponement of nuclear talks, immediate oil relief could still disappear into another risk premium.

Holmes normalization combined with verifiable uranium removal and enforceable limits gives the Fed a better chance of treating the shock as temporary.

Next is the data test

While the rise in Bitcoin’s Iran trade is reliable as a relief trade, it is too early to make a complete macro judgment.

The bullish version is easy to map. The tanker returns. Sales of Iranian oil will increase supply. Brent and WTI continue to fall. Gasoline prices will follow suit. Breakeven point Inflation subsides.

The premium that existed during the oil crisis no longer exists in government bond yields. Fed officials are regaining confidence that energy pressures will not undermine inflation expectations. In that world, the market could bring forward the timing of rate cuts, and Bitcoin’s rally could be more than just a geopolitical headline trade.

The bearish version requires only enough unresolved risk for the energy market to continue with price turmoil. If the Hormuz River flow remains impaired, if Gulf Coast production remains suppressed, if gasoline prices remain high, or if the final nuclear language on enrichment and verification appears weaker than the JCPOA, the Fed and midterm voters will face much the same inflation problem under a more moderate label.

That’s the test. Since the rate channel is real, it is correct for Bitcoin to react to a drop in oil pressure.

Traders would be going too far if they treated the reported political framework as already equivalent to disinflation. By November 2026, when this trade shows up in barrels, freight, gas stations, inflation compensation, and Fed pricing, this rally becomes a permanent macro off-ramp.

Until then, Bitcoin’s Iranian trade rally is a reasonable bailout trade pending data evidence.

(Tag translation) Bitcoin