In traditional markets, the VIX provides traders with a way to hedge or trade against expected stock market volatility, rather than looking directly at the S&P 500. CME Bitcoin Volatility Futures offers Bitcoin traders a regulated version of that idea. In other words, it’s a way to bet on the volatility of Bitcoin without betting on its price.

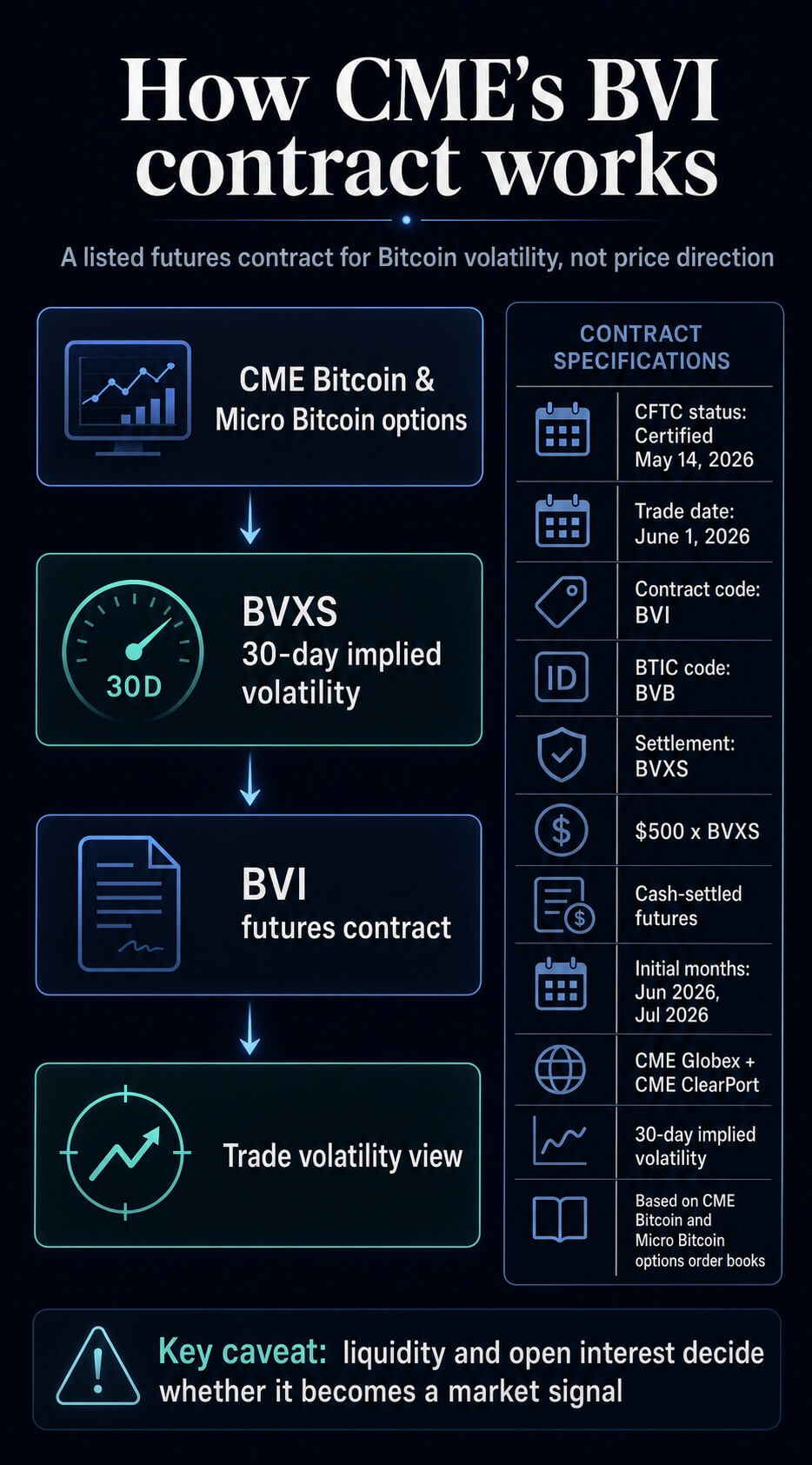

The exchange plans to list Bitcoin volatility futures and begin trading on June 1st, and the Commodity Futures Trading Commission listed the contract as certified on May 14th.

Therefore, this launch will be a test of the market structure. That is, whether Bitcoin is ready for regulated futures contracts tied to the very anticipated disruption.

This contract (ticker BVI) will be financially settled on the CME CF Bitcoin Volatility Index – Settlement (BVXS). The index is designed to reflect a 30-day forward-looking view of implied volatility extracted from the CME Bitcoin and Micro Bitcoin options order book.

In practical terms, trading desks can use Bitcoin futures, spot ETFs, or options to express whether they expect Bitcoin’s price to be more moderate or more volatile next month without looking at the price directly.

Although this product has a VIX-style feel, it does not make the BVI a proven Bitcoin fear meter before trading begins. This imposes a regulated contract centered around what traders are already focused on: how much movement the market expects Bitcoin to make, regardless of whether the next move is higher or lower.

The VIX became important in traditional finance because it turned expected volatility into a common language of risk. Portfolio managers use it to hedge against shocks, option desks use it for price stress, and analysts use it as shorthand for market fears. The BVI is looking to introduce a similar layer to Bitcoin, but traders will need to prove the scale of their use of Bitcoin.

CME’s new contract moves trading away from price direction

Certification details will update CME’s May 5th launch announcement without changing the underlying schedule. This agreement has moved from the pending regulatory review planned in the announcement to the CFTC product record marked certified.

The contract will be available on CME Globex and CME ClearPort starting Sunday, May 31, in advance of the June 1 trading session, according to CME’s corresponding May 14 filing.

This certification is a milestone for listing. CME has certified the contract under the relevant CFTC processes, but other questions remain regarding regulatory approval and future liquidity.

This provides institutional desks with a familiar trading and clearing framework for Bitcoin volatility trading.

For most readers, the key terms are simpler. BVI is a futures contract, BVXS is a settled index, and the value of each contract is $500 times the BVXS level.

The first months listed are June 2026 and July 2026.

The real difference is exposure. Bitcoin futures allow traders to know where their BTC will be traded. Bitcoin ETFs offer investors spot-linked exposure within their brokerage accounts.

Bitcoin options can express both price and volatility views, but require option execution and option risk management. BVI packages a volatility perspective into a publicly traded futures contract that moves up or down depending on the market’s expectations for Bitcoin’s movement, not just the spot price of Bitcoin.

CME’s product page makes that distinction clear, stating that the contract is intended to hedge Bitcoin’s exposure to rising or falling volatility, and to trade expectations of market disruption independently of the direction of Bitcoin’s price.

BVXS turns option prices into reference points

Futures contracts are only as useful as the benchmarks underlying them. BVXS is the daily settled version of the CME CF Bitcoin Volatility Index.

CF Benchmark describes BVXS as a once-daily benchmark representing a forward-looking 30-day constant maturity implied volatility measurement based on the CME Bitcoin and MicroBitcoin options order book.

In reality, the Bitcoin volatility index translates CME option pricing into a daily reference point for expected BTC turbulence.

BVXS does not track Bitcoin itself. It tracks which option prices indicate how much Bitcoin is likely to move over the next 30 days. Therefore, BVXS is not a spot price benchmark, but rather a Bitcoin implied volatility benchmark.

If options traders are pricing in more uncertainty, the index could rise before Bitcoin moves significantly. If options traders demand less protection or expect calmer trading, the index could fall even if Bitcoin remains directionally active.

This feature makes this product more than just an access rail. Funds that own Bitcoin exposure through spot holdings, ETFs, futures, or structured products may not want to sell the underlying exposure whenever market stress increases.

Instead, you may need a tool that targets volatility directly. Conversely, traders may anticipate confusion around macro printing, regulatory events, reversals in ETF flows, or market disruptions without being certain whether BTC will rise or fall.

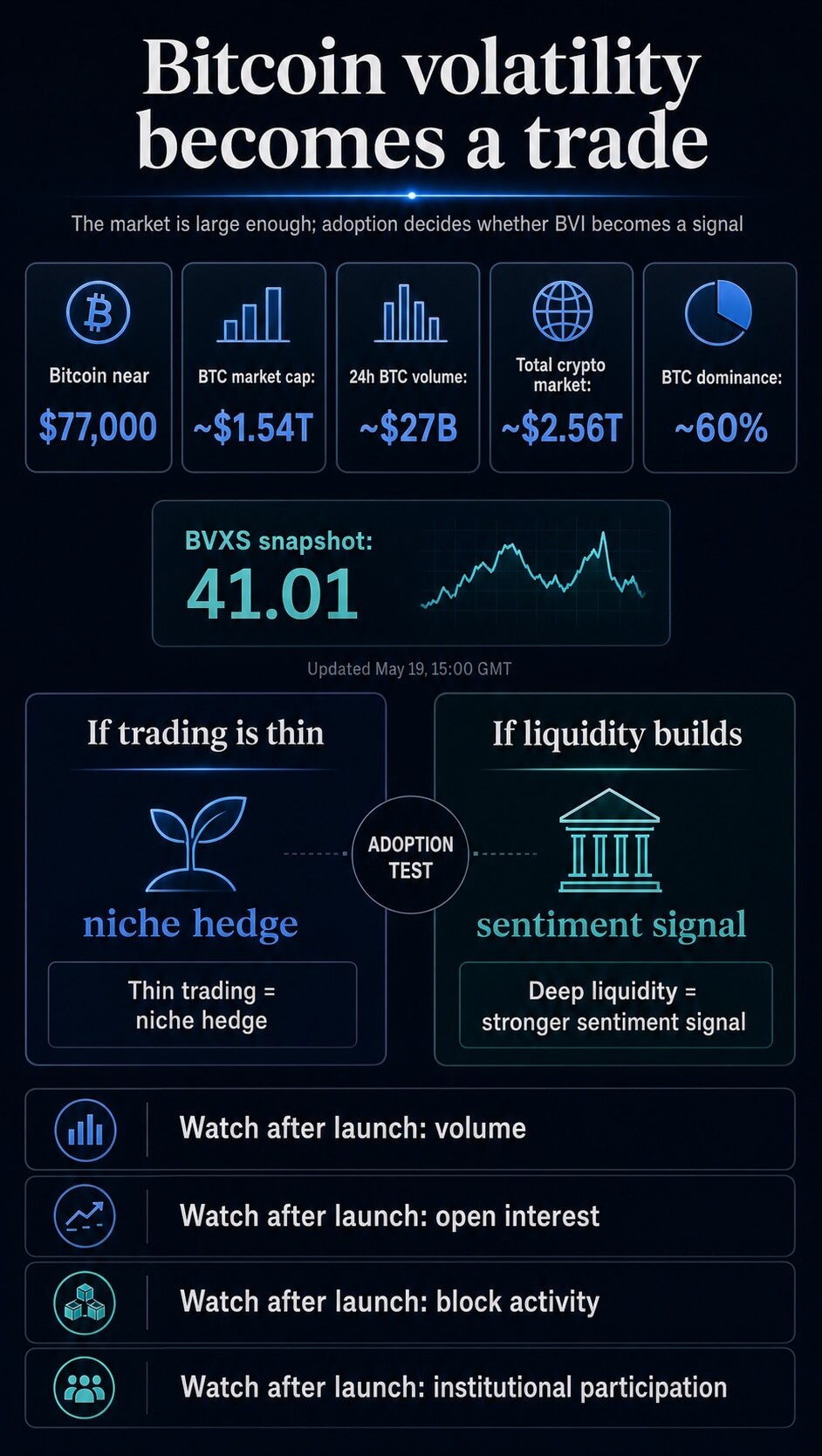

As of May 20th, the latest CF Benchmark numbers available before the session showed BVXS down 0.99% to 41.01.

Bitcoin currently has an implied volatility benchmark linked to CME under the listed futures product.

Why financial institutions care about Bitcoin fear trading

For institutional investors, the BVI provides an easy way to isolate the often mixed trades of Bitcoin futures, options, and ETFs.

In directional products, traders are typically exposed to Bitcoin levels. A long position in Bitcoin futures can make a profit if BTC rises and incur a loss if it falls. Spot ETF holders are tied to the direction of the asset.

Options can isolate volatility, but trading is more complex and involves exercise selection, expiration, time decay, and position management risks.

The BVI is posing to the desk a more concise list of questions: “Will Bitcoin move more or less than the market currently expects?”

This helps desks hedge portfolios, price instruments, manage options books, and adjust positions around events where the magnitude of the move is more important than the direction.

The timing also fits with CME’s broader crypto market structure push. According to CME, 24/7 crypto futures and options trading is scheduled to begin on May 29, just before the inauguration of the BVI. It also extends CME’s Bitcoin derivatives stack beyond directional futures, options, and ETF adjacent market exposure.

These two developments are pointing in the same direction. Regulated crypto derivatives are becoming less like a side session attached to traditional market hours and more like an infrastructure designed around how cryptocurrencies are actually traded.

igcurrencynews’s recent Bitcoin coverage is largely in line with the direction and access questions that have dominated the market: reversals in ETF flows, inflationary pressures, option liquidity around spot ETF products, institutional investor accumulation, and the declining economics of some retail ATM models.

CME’s volatility contract moves the discussion to another layer. It asks whether Bitcoin risk can become a commodity in its own right.

This question becomes meaningful when you consider Bitcoin’s size. According to igcurrencynews’s market page, as of May 20, Bitcoin was valued at nearly $77,000, with a market capitalization of approximately $1.54 trillion and 24-hour trading volume of approximately $27 billion.

The broader cryptocurrency market is approximately $2.56 trillion, with BTC controlling nearly 60%. In that context, regulated volatility futures are an attempt to allow market expectations for Bitcoin movements to be traded in a more direct manner.

Launch testing is about fluidity, not branding

However, comparing CME BVI futures to the VIX can potentially overvalue the commodity before any trading data exists.

VIX futures and options are established instruments for trading or hedging volatility risk. The BVI has not yet achieved that status.

Tests after June 1 will be practical. That is, whether the contract attracts volume, open interest, blocks of activity, and enough institutional participation to be a meaningful signal.

Trading volume, open interest levels and price information will be published daily, according to CME’s filing. These numbers have more meaning than the label at the time of release.

With more trading volumes, the BVI could offer market participants a cleaner way to hedge their Bitcoin exposure in case of expected turbulence, or to express a view that expected volatility is too high or too low.

It can also give analysts new signals about market stress, along with ETF flows, option positioning, futures basis, and spot liquidity.

If trading is thin, this product will not become a broad sentiment gauge and may remain useful to some desks. This result would still add a regulatory tool to Bitcoin’s derivatives stack, but would stop short of turning Bitcoin’s volatility into a widely followed market instrument.

CME has scheduled a CFTC-certified Bitcoin volatility futures contract on June 1, tied to a 30-day implied volatility benchmark constructed from CME Bitcoin options data.

This gives financial institutions a way to trade expected Bitcoin turbulence without directly betting on the price. Whether it becomes a Bitcoin fear trade depends on what happens when traders can actually use Bitcoin.

(Tag translation) Bitcoin