Public Bitcoin miners have spent years competing to add hashrate to the network. In the first quarter of 2026, many companies did the opposite.

This article first appeared in Miner Weekly, Blocksbridge Consulting’s weekly newsletter featuring the latest energy, computing, infrastructure, and data analytics news from The Energy Mag. The original article can be found here.

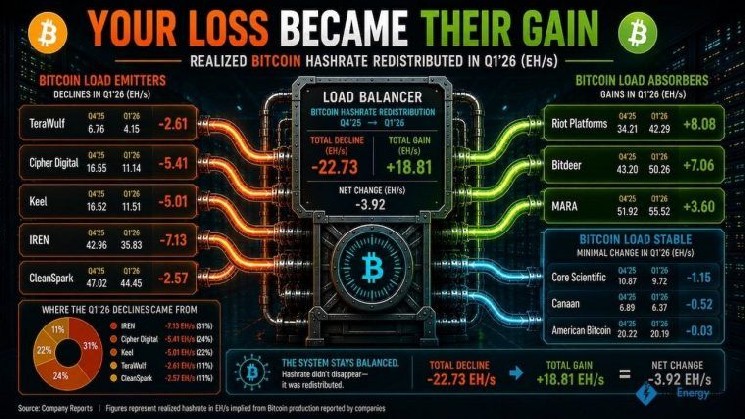

Bitcoin’s average network hash rate, based on public blockchain data, has fallen from approximately 985 EH/s in Q4 2025 to 873 EH/s in Q1 2026. Separately, TheEnergyMag compiled quarterly production disclosures from major publicly traded miners and calculated their respective realized hashrates implied by Bitcoin production results.

At first glance, the overall changes among large public miners seemed relatively modest. The total realized hashrate of the 10 major companies tracked by TheEnergyMag decreased slightly from approximately 297 EH/s in Q4 2025 to 291 EH/s in Q1 2026. HIVE and Cango (NYSE: CANG) were excluded from the comparison due to incomplete production data for the first quarter.

But beneath that seemingly stable aggregate number was a more notable redistribution of industrial-scale hashing power.

Companies such as Core Scientific (NASDAQ: CORZ), IREN, Cipher Digital (NASDAQ: CIFR), TeraWulf (NASDAQ: WULF), and Keel Infrastructure (NASDAQ: KEEL) have significantly reduced their realized hashrate when dismantling or repurposing their mining fleets for AI and HPC infrastructure, as have companies such as Bitdeer (NASDAQ: BTDR), MARA (NASDAQ: MARA), and American Bitcoin. (NASDAQ: ABTC) has expanded aggressively to absorb some of the stolen network share.

Among the companies that fell the most, IREN’s realized hashrate fell from 42.96 EH/s to 35.83 EH/s, while Cipher’s realized hashrate fell from 16.55 EH/s to 11.14 EH/s after it completely discontinued mining operations at its Black Pearl facility in February and began renovating the site for HPC infrastructure. Keel Infrastructure (formerly Bitfarms) decreased from 16.52 EH/s to 11.51 EH/s as it continued to wind down its traditional mining operations and transition to AI infrastructure development in North America.

CleanSpark (NASDAQ: CLSK) witnessed a modest decline, but similarly signaled its intention to continue monetizing its Bitcoin infrastructure while selectively pursuing AI opportunities. Executives said the old ASIC fleet could eventually be sold or transferred once the AI implementation is fully operational, but the company acknowledged that future site conversions could result in additional impairment charges.

In contrast, Riot Platforms (NASDAQ: RIOT) increased its realized hashrate from 34.21 EH/s to 42.29 EH/s during the quarter. Bitdeer rose from 43.20 EH/s to 50.26 EH/s due to the activation of SEALMINER, while MARA rose from 51.92 EH/s to 55.52 EH/s despite the business’s simultaneous expansion efforts centered on AI and HPC initiatives.

This divergence highlights growing fragmentation within the public mining sector, with changes particularly evident in corporate filings and financial statements, with several miners disclosing large-scale fleet demolition operations, asset write-downs, and impairments to mining infrastructure directly related to AI transformation.

Core Scientific said its mining operations will continue to shrink through 2026 as the company prioritizes Coreweave’s (NASDAQ: CRWV) high-density colocation infrastructure, and management said it expects only one or two sites to remain operational for Bitcoin mining by the end of the year. The company recorded impairment charges of $266.5 million in the first quarter of 2026, including $151.6 million related to mining equipment and $114.9 million related to mining infrastructure.

Cipher Digital separately disclosed $30.8 million worth of mining rigs classified as held for sale following the closure of its Black Pearl mining operations. TeraWulf had about 54,100 Bitcoin miners as of March 31, but only about 35,500 were operating at its Lake Mariner campus. The remaining approximately 18,600 miners were classified as undergoing maintenance, awaiting disposal, or waiting to replace units undergoing repair.

Rather than simply leaving rigs idle during periods of economic downturn, operators are permanently repurposing substations, cooling systems, and data center layouts for AI deployments. Once your infrastructure is converted for GPU workloads, it’s hard to imagine going back to Bitcoin mining any time soon.

American Bitcoin, one of the few companies that continues to expand its mining fleet, argued that this transition could create long-term opportunities for avid Bitcoin miners willing to continue expanding while competitors retire their fleets.

The company increased its fleet capacity from 25 EH/s to 28.1 EH/s in April following the reactivation of its Drumheller site, which had been offline since 2024. Much of that growth, as well as the 2025 production increase, was financed through an unconventional structure that used pledged Bitcoin rather than cash to acquire a new generation of ASIC miners from Bitmain.

As of March 31, 2026, ABTC has pledged a total of 3,090 Bitcoins to Bitmain for the purchase of 18 EH/s of computing power, which alone represents almost 64% of ABTC’s 28.1 EH/s proprietary mining fleet. ABTC mined 817 Bitcoins in Q1 2026, an increase of 505% year-over-year. At its current production pace, assuming the Bitcoin network’s hash rate remains roughly stable, the company could theoretically mine back the amount of Bitcoin collateral it initially pledged in about six quarters.

If the network hashrate continues to decline as industrial miners extract more hashrate to pivot to AI infrastructure, the payback period for ABTC in Bitcoin terms could further accelerate as the remaining miners capture a larger share of the block reward.

Overall, the ongoing migration has changed the financial logic of the mining industry. In previous downcycles, miners typically powered down their rigs because falling Bitcoin prices and rising energy costs made operations uneconomical. However, in 2026, miners will increasingly decommission fleets as AI infrastructure offers more stable long-term cash flows, stronger financing terms, and higher expected returns on power capacity.

It will be worth watching to see how the dynamics play out in the coming quarters. But for now, the system remains balanced.