Bitcoin has seen repeated mid-month strength this year, making it increasingly difficult to distinguish it from Strategy’s (formerly MicroStrategy) expanding preferred stock machine. This funding channel has helped the company continue to purchase its flagship digital assets, while increasing the cost layer on its balance sheet.

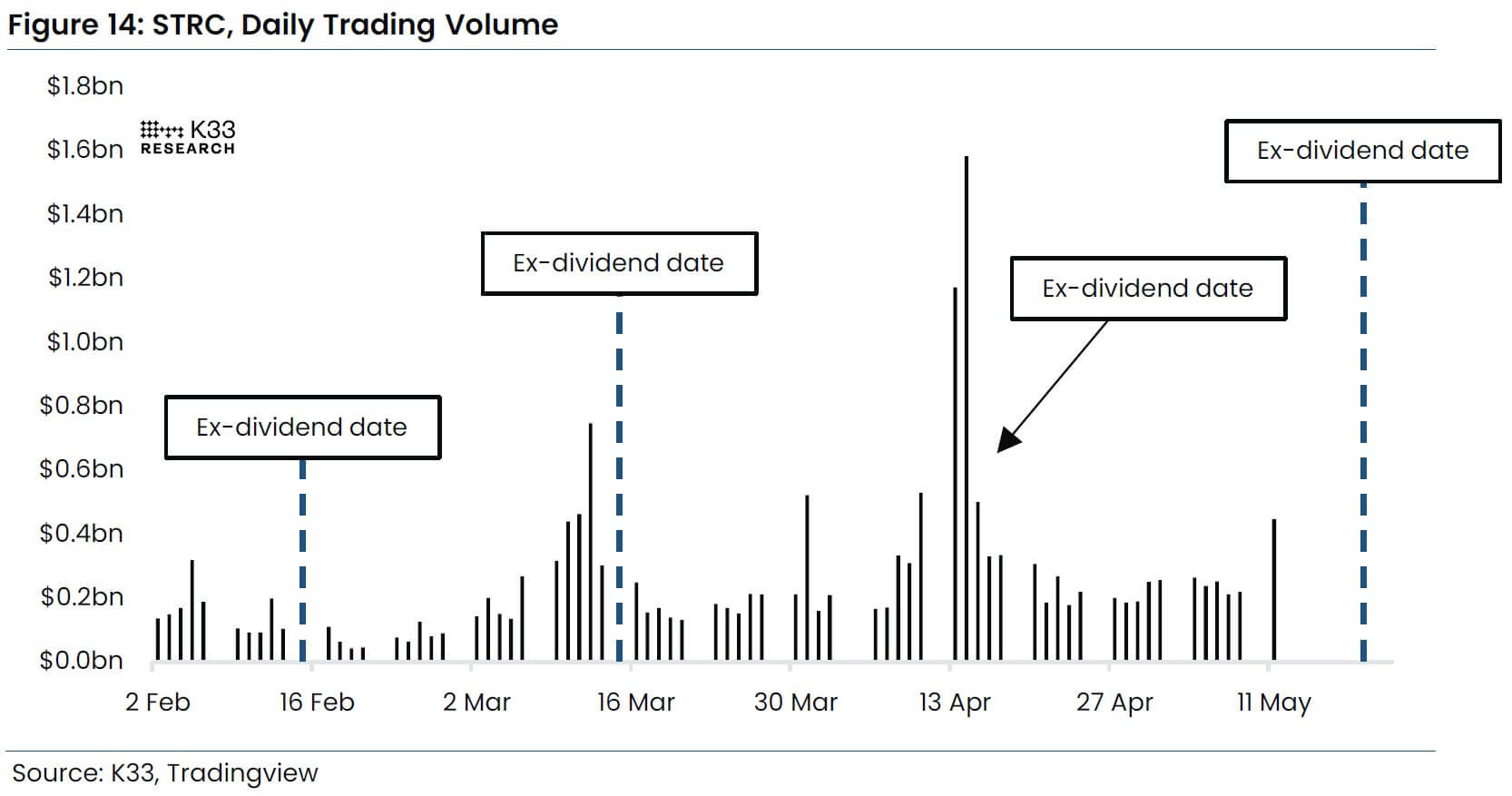

Research firm K33 has linked this pattern to STRC, Strategy Inc.’s perpetual preferred stock, which has become a key source of liquidity for the world’s largest corporate Bitcoin holder. This product pays a dividend at the end of the month, but investors must own the stock by the 15th to receive the dividend.

This deadline has made the middle of each month a predictable time for demand. Investors buy STRC ahead of the cutoff, trading volume increases, and the stock price moves back toward its $100 par value.

Once STRC trades above par, Strategy can issue new shares through its market program and use the proceeds to buy more Bitcoin.

According to data from STRC.live, this loop has been active this week, giving STRC plenty of room to return to par and give the strategy the funds to buy more than 5,000 Bitcoin before the next ex-dividend deadline on Friday.

This move extends the pattern that makes the strategy’s capital market activity a recurring feature of Bitcoin spot market flows. This also confirms why STRC has become the most dominant preferred stock on the market.

STRC turns dividend demand into Bitcoin purchases

The amount of Bitcoin acquired through this particular funding channel has been accelerating aggressively since the beginning of the year.

According to K33 research, Strategy used STRC proceeds to purchase 4,467 Bitcoin in January. By March, the amount of purchases related to preferred stock had increased to 22,131 Bitcoin.

In April, this number rose again to around 46,872 Bitcoins, demonstrating how quickly Bitcoin has transitioned from a funding tool to a major driver of the company’s accumulation strategy.

Vettle Lunde, head of research at a cryptocurrency research firm, explained that this mechanism is a mechanical demand source.

He said STRC attracts yield-focused investors before the ex-dividend date, helps the preferred stock recover its par value, and gives Strategies the market depth it needs to issue more shares. The company then converts that demand into spot purchases of Bitcoin.

Meanwhile, Strategy is currently trying to tighten the cycle. The company proposed changing STRC’s dividend schedule from monthly payments to bi-monthly distributions, arguing that more frequent payments would reduce reinvestment delays and improve market efficiency.

This change will result in more frequent funding opportunities. While this will strengthen mid-month buying patterns, it may also increase the strategy’s reliance on products with much higher costs than previous financing tools.

Strategy’s low capital era gives way to preferred stock

While the STRC mechanism has helped shape BTC’s short-term market performance, institutional researchers are sounding the alarm about the long-term sustainability of the trade.

The company, led by Michael Saylor, has relied on common stock issuance and convertible debt for much of Bitcoin’s accumulation history.

Both were attractive because Strategy’s stock was trading at a significant premium to the value of its Bitcoin holdings, and bond investors were willing to accept a lower coupon in exchange for the potential for stock price appreciation.

However, these conditions have weakened significantly over the past year.

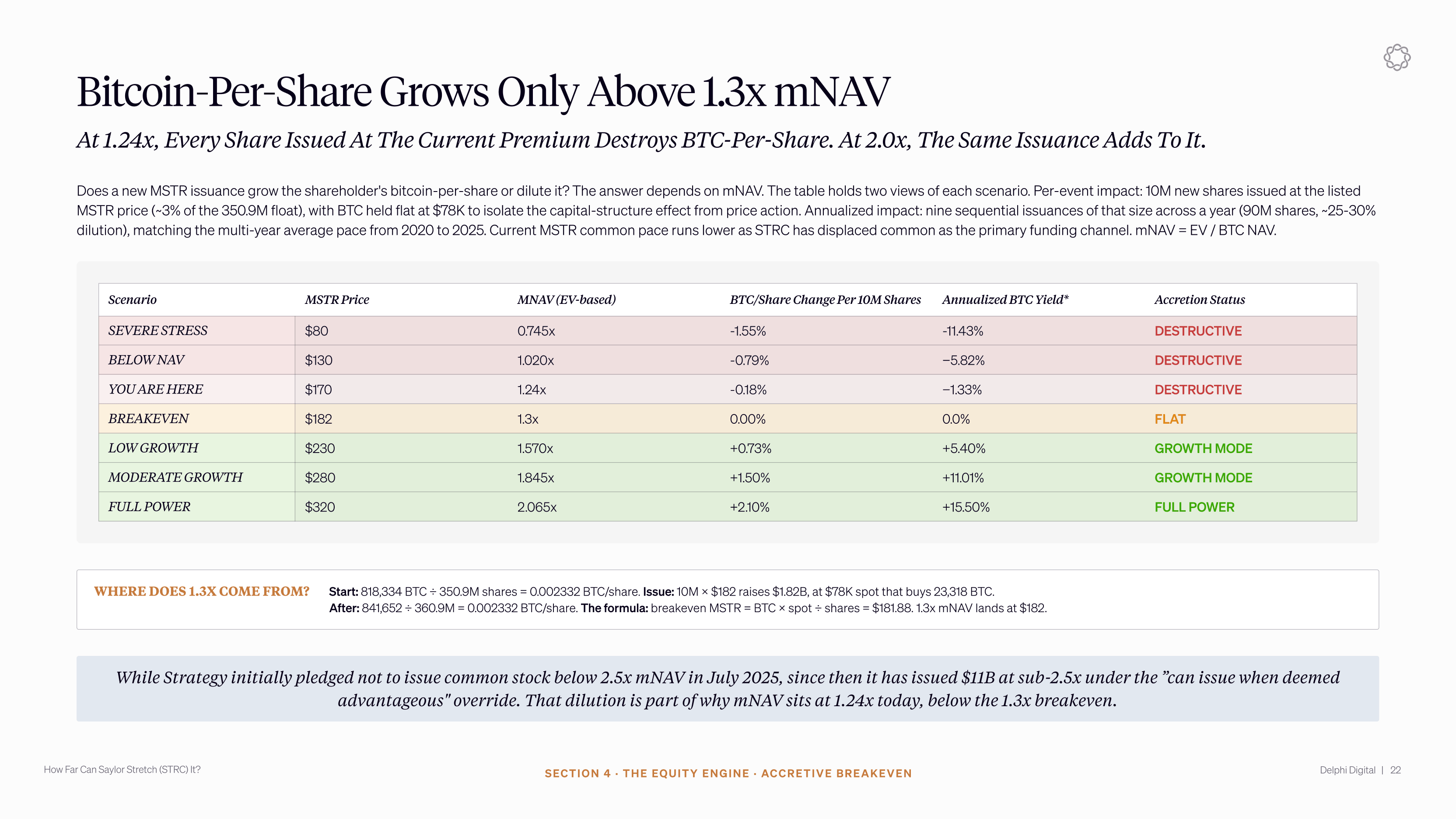

Delphi Digital estimates that Strategy’s common stock premium currently trades at approximately 1.24 times enterprise value-based net asset value. At that level, there is much less benefit in issuing common stock to get more Bitcoin per share.

Furthermore, the limits for convertible bonds are narrowing. Strategy has approximately $8.2 billion in principal outstanding from previous transactions, with repayments scheduled to begin in September 2027.

This makes STRC the primary funding engine for Strategy’s recent BTC purchases. Because preferred stocks sit lower in the capital stack than preferred and convertible bonds, investors need more compensation for risk.

STRC’s annualized yield has already risen to 11.5%, a significant increase from the cheap financing that supported Strategy’s initial Bitcoin purchases.

The trading price per Bitcoin share will increase

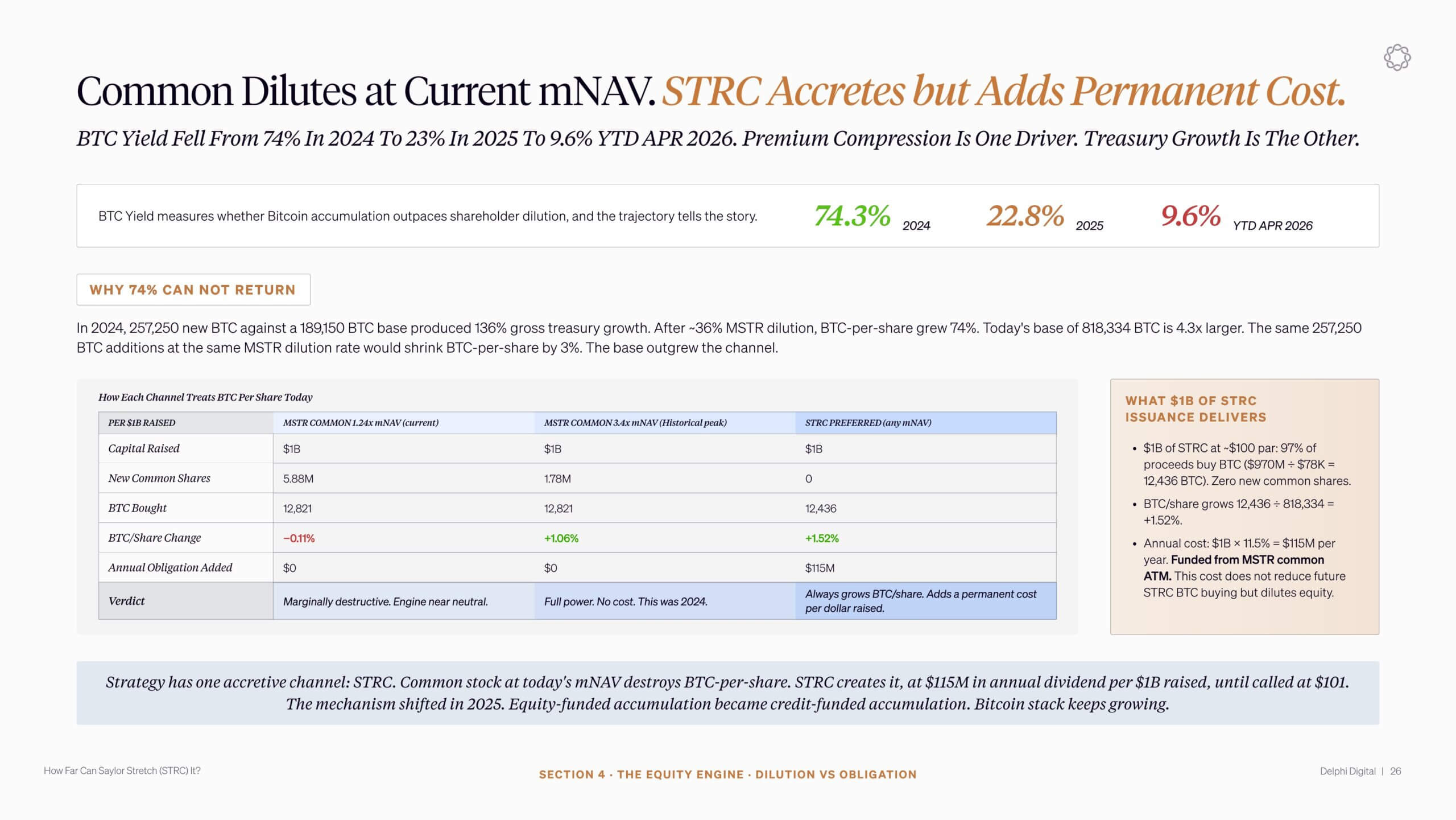

STRC is still helping Strategy buy Bitcoin without directly issuing common stock for purchase. This is central to the company’s claim that the program can support Bitcoin per share growth.

Delphi estimates that approximately 97% of every $1 billion raised through STRC could be invested in Bitcoin. At the current price, Strategy’s Bitcoin per share index at the time of issuance could rise.

You will receive the cost later. Each $1 billion in STRC results in an annual dividend obligation of approximately $115 million. These payments will need to be processed and Delphi expects the strategy to rely on the issuance of common stock to satisfy those payments.

This turns the priority program into a delayed dilution mechanism. Bitcoins purchased with STRC proceeds may initially provide higher per-share exposure, but as more common shares are issued to fund payments, regular dividend claims will gradually offset that gain.

The Delphi model shows that the effect fades over time. Bitcoin per share growth could exceed 7% in the first year of the program, but could decline to just over 3% by the third year due to growth in the preferred stock base and increased dividend obligations.

The pressure becomes even more acute as we approach the STRC authorization limit of $28.3 billion. Once the strategy reaches its limit, the preferred stock engine will not be able to continue funding new purchases at the same pace. However, the dividend bill still remains.

Under these circumstances, Delphi predicts that net Bitcoin per share growth could turn negative, shrinking by nearly 6% annually, as regular issuance is used to pay for preferred dividends rather than expanding holdings.

Bear markets can stress the loop

The bigger risk is that the STRC mechanism works best when Bitcoin is rising and investor appetite for yield remains strong.

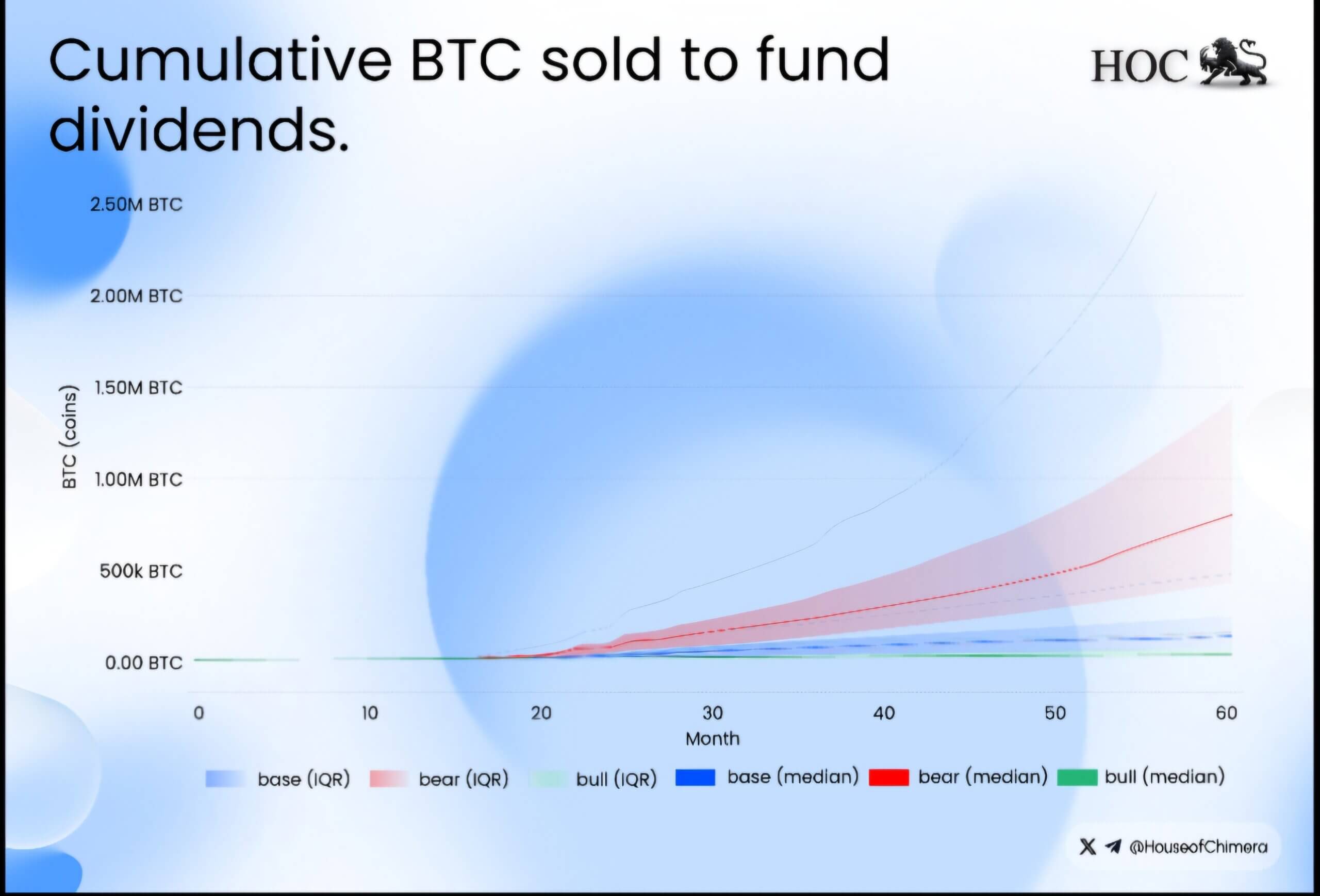

Blockchain research firm House of Chimera has warned that a continued economic downturn could create a negative feedback loop.

According to the company,

“As Bitcoin declines, STRC may need to raise its dividend to maintain investor demand. However, as yields rise, the strategy’s monthly cash obligations also increase at the very moment the value of its BTC holdings declines. This creates a structurally weak feedback loop where deteriorating market conditions force the structure to commit to ever-larger dividends.”

House of Chimera’s test suggests that under pessimistic market conditions, Strategy’s $2.5 billion cash reserves could be depleted within 17 to 22 months.

If that happens, the company will have the weakest market access and at the same time face a liquidity crunch.

Additionally, the bigger risk is that Strategy may eventually be forced to sell Bitcoin to meet its dividend obligations.

A forced sale would increase pressure on the spot market, weakening demand for STRC and potentially requiring higher yields to restore investor confidence.

In the most severe scenario, House of Chimera could end up being forced to sell close to 800,000 Bitcoin due to its stack of preferred stock.

Strategy shifts from accumulation to balance sheet management

Recognizing changing financial realities, Strategy’s corporate stance has evolved.

The company’s recent disclosures signal a more proactive approach than its previous “never sell” stance associated with founder and chairman Michael Saylor.

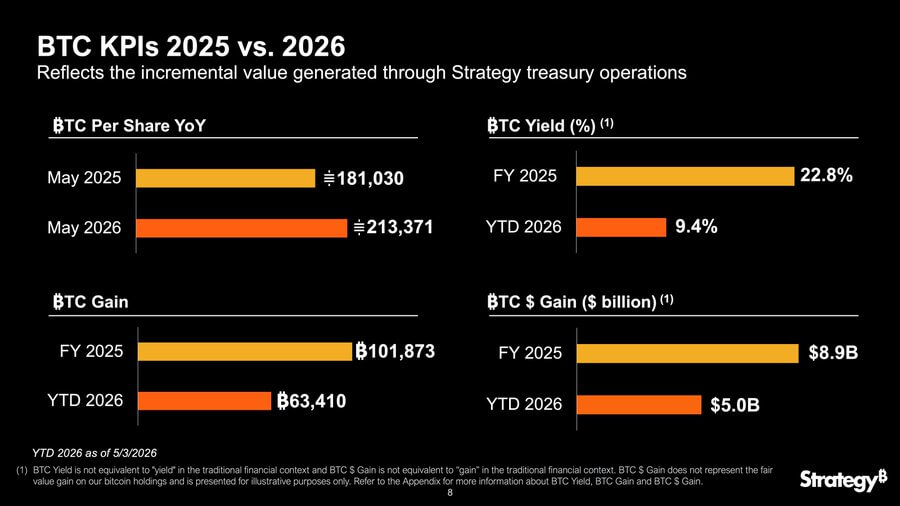

The focus has shifted to maximizing BTC yield, a corporate metric that tracks the growth in physical Bitcoin holdings relative to the number of shares outstanding. In a post on X, the company’s president and CEO von Leh said:

“Bitcoin per share (BPS) is our true north. Every day, the strategy uses multivariate models to optimize capital, equity, debt, and credit decisions to maximize annual BTC yield (BPS growth). Year-to-date, we have achieved a 9.4% BTC yield and $5 billion in BTC gains.”

As cheap debt decreases, preferred dividends expand, and the cost of each new Bitcoin purchase increases, it will become harder to keep these numbers positive.

For now, STRC will continue to support reliable mid-month Bitcoin bidding. This instrument converts demand for yield into new capital, which continues to flow into the spot market.

But trade is becoming more volatile. While the strategy’s funding machine may still drive Bitcoin higher in the short term, the same structure is building a larger dividend burden on each purchase.

As STRC grows, the question for shareholders and Bitcoin traders will be whether the company can continue to generate more Bitcoin per share after fully accounting for the cost of the machines.

(Tag Translation) Bitcoin