Fintech and stablecoin companies should consider looking outside the U.S.-Mexico corridor to capture the $174 billion Latin American remittance market, according to Bybit executives.

Claudia Wang, Bybit’s chief marketing officer, said in a post on X on Sunday that most companies are too narrowly focused on the $61.8 billion U.S.-Mexico remittance market, overlooking the rapidly growing U.S.-Central America corridor and intra-Latin America remittances.

“The corridors that look ‘hot’ now are not the corridors that most fintech companies are optimized for,” he said, citing Venezuela to Colombia, Argentina to Bolivia, and Spain to Ecuador. The market for remittances to Mexico from outside the United States is approximately $112 billion.

“Stop treating Latin America as one market,” Wang said, adding that he had studied the region for six months.

“Brazil, Mexico, Argentina, Colombia, each requires different licenses, different rails, different stablecoins, different marketing. The companies that win here are running country-specific stacks rather than regional stacks.”

Money transfers across the United States have primarily been facilitated through bank rails by companies such as Western Union and MoneyGram. However, following the passage of the GENIUS Act in July, both companies revealed plans to deploy stablecoin infrastructure.

Western Union is building its own USD-backed stablecoin, USDPT, which is in the final stages of preparation and expected to launch this month.

Wang pointed out that crypto-native companies such as Binance, Bitso, Strike and Felix Pago are also competing in the Latin American remittance market, as are banks and retail and telecom companies such as Walmart and Tigo.

U.S. immigration policy is impacting the Latin American remittance market

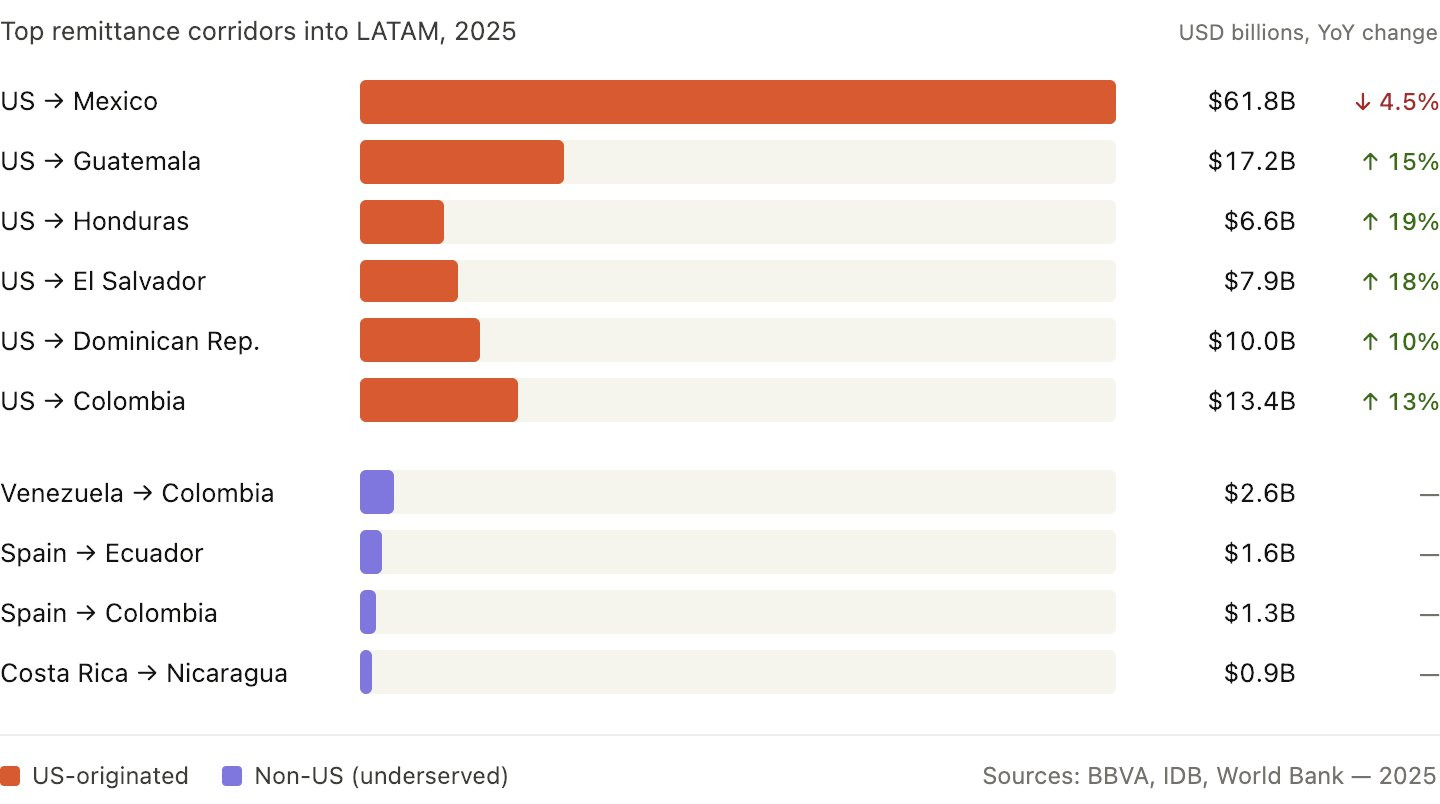

Wang pointed out that the corridor from the United States to Central America is “exploding”, with remittances to Honduras, El Salvador and Guatemala expected to increase by 19%, 18% and 15%, respectively, in 2025.

In contrast, saturated remittances between the U.S. and Mexico fell 4.5% to $61.8 billion.

Wang said the disconnect between the increase in Central American inflows and Mexico’s decline is the result of U.S. immigration policy: “Central American migrants are repatriating in larger numbers, faster, and in greater quantities to avoid the risk of deportation.”

In contrast, in Mexico, where “the diaspora is more established and documented,” Wang said, “we don’t see any behavior that would cause panic.”

Top remittance corridors in 2025. source: Claudia Wang

Regarding remittance markets outside the U.S., Wang noted that while some of these remittance markets are absolutely small, they are “barely serviced” by U.S. remittance providers and are “barely touched by the crypto rails.”

Latin Americans want to hold stablecoins, not just move them

Wang also said that many Western fintech companies are unaware that “killer apps” in Latin America hold stablecoins without moving them.

“Users don’t want to ‘use’ stablecoins for transactions and convert back to their local currency; they want to keep their dollars. Trading is a side effect.”

Wang said there are no clear winners in the Latin American remittance market, adding: “The fintechs that win in the region over the next decade will combine local rail, stablecoin liquidity, trust, and closed-loop economics, send->hold->spend->earn.”

Related: Australian Bill Settlement Vision focuses on stablecoin interoperability

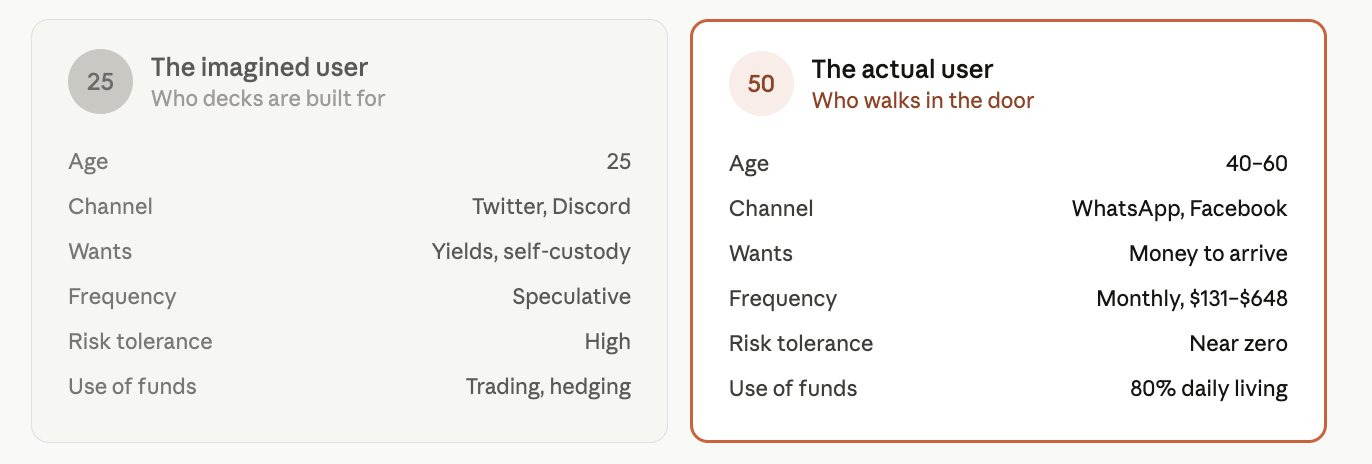

He added that many fintech companies in this space are building products for the typical 25-year-old crypto trader, rather than the average 40- to 60-year-old remittance sender who is perhaps less tech-savvy.

Profiles of an imaginary Latin American remittance user (left) and a real user (right). sauce: Claudia Wang

“If your product makes a 50-year-old factory worker in New Jersey think more than 30 seconds before sending $300 to his mother in Honduras, you’ve already lost,” Wang says.

“The cryptocurrency industry has spent five years optimizing for the wrong users. Latin American retail remittance customers don’t want ‘self-custody.’” They want to know if their funds have arrived. ”