The European Union is racing towards the deadline for its side of the existing US-EU trade deal, with the next formal triumvirate scheduled for May 19 in Strasbourg.

President Donald Trump on May 2 threatened to raise tariffs on EU cars and trucks from 15% to 25%, which the Kiel Institute for the World Economy estimates could cost German production nearly 15 billion euros in the short term.

Bitcoin’s exposure to this trade war is driven by US inflation, Federal Reserve policy, and risk appetite among assets.

On March 26, the European Parliament introduced an implementing bill that would link EU tariff reductions to US compliance, a sunset clause that would end concessions on March 31, 2028, and a suspension mechanism in the event of a US breach of the agreement or a surge in US imports.

Some EU governments have resisted these conditions as too restrictive and want faster implementation with fewer safeguards. Bernd Lange, parliament’s chief trade negotiator, said on May 7 that “there is still a way to go.”

The deal would eliminate tariffs on U.S. industrial goods and open preferential access to some U.S. agricultural and seafood exports, while the EU would receive a 15% tariff cap on affected items, which President Trump is now threatening to replace with a 25% tariff on cars.

| date | event | Why is it important to the market? |

|---|---|---|

| March 26th | European Parliament advances implementation of law with sunrise, sunset and suspension safeguards | A deal is in progress, but it shows there are political conditions attached. |

| May 2nd | President Trump threatens to raise EU car tariffs from 15% to 25% | Changing the trade story to real inflation and risk-off threats |

| May 7th | Bernd Lange says: “We still have a ways to go” | Indicates that the transaction is in progress but not yet completed |

| May 19th | The next official tri-low round will be in Strasbourg | Key negotiation deadlines for short-term market forecasts |

| May 28th | Next US PCE Inflation Release | A key test of whether tariff concerns are reflected in Fed expectations |

Macro Bridge to Bitcoin

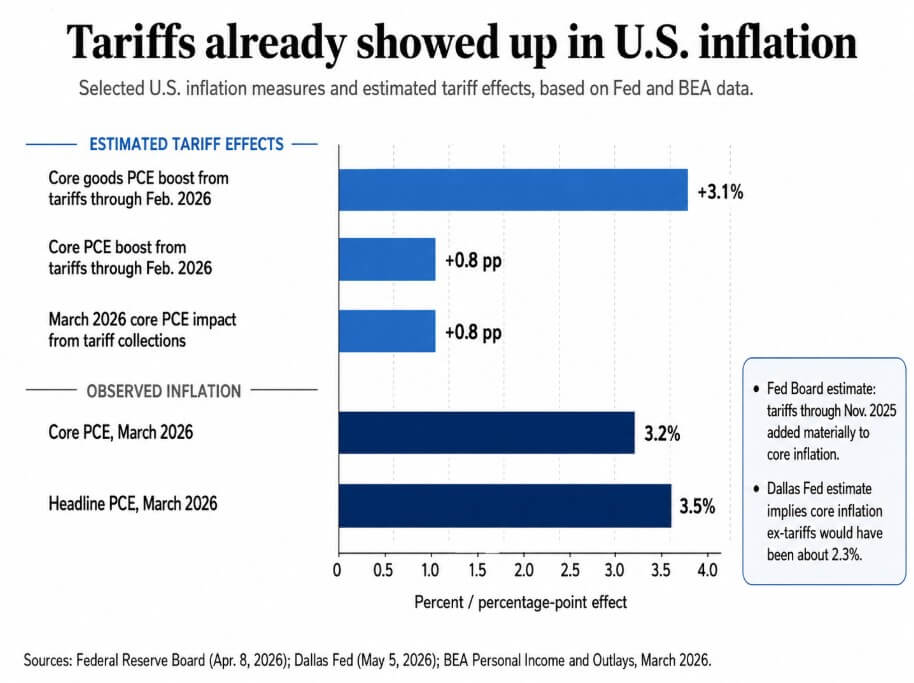

An April 8 Federal Reserve memo estimated that tariffs implemented through November 2025 would increase PCE prices for core products by 3.1% by February 2026, and overall core PCE by 0.8%.

A Dallas Fed study released on May 5 estimated that the tariff collection would increase core PCE inflation by about 0.8% for the 12 months ending March 2026, and used a different methodology to back up this figure. The results suggested that core inflation, excluding the impact of tariffs, would be around 2.3%. Composite PCE in March 2026 was 3.5% year-on-year.

These numbers show that the 2025 wave of tariffs significantly boosted core inflation, even though the Fed said on April 29 that it kept rates unchanged at 3.5% to 3.75% and that inflation remained high.

A 10% tariff hike could initially compress demand enough to lower headline inflation, before product inflation peaks about 1.2 percentage points higher in the second year, and services inflation rises about 0.6 percentage points in the third year, according to research from the San Francisco Fed.

This nonlinear path could create the kind of ambiguous macro signal that could keep Fed policy on hold for longer than markets expect, eliminating the risk of the easing cover that assets need.

In the case of Bitcoin, lengthening the Fed’s holding period would tighten dollar liquidity and reduce the scope for the speculative risk appetite that has historically supported Bitcoin’s rise.

An IMF study found that 80% of crypto price fluctuations are explained by a single common “crypto factor” and that the volatility of Bitcoin and Ethereum is four to eight times more correlated with major U.S. stock indexes than before the pandemic, which is directly related to institutional capital inflows.

The Kiel Institute estimates the long-term loss of German production due to the threat of tariff hikes is around 30 billion euros, at a time when forecasters expect German growth to be only 0.8% this year.

Growth concerns in Europe and inflation fears in the US could create a mix between markets and trigger a broader pulse of risk aversion, potentially impacting Bitcoin as it trades with higher equity correlations.

what to expect

Tariff overhangs will fade as a short-term macro variable once Congress and member states resolve the safeguard dispute and the U.S. government backs away from the 25% auto threat.

| scenario | macro effect | Fed involvement | BTC read-through likely |

|---|---|---|---|

| The deal progresses and the 25% threat fades. | Reducing inflation concerns and trade stress | There is further room for the market to factor in future easing. | Mild risk-on mitigation |

| Negotiations drag on, with no clear solution | continuing uncertainty | Fed remains cautious, headlines matter more | BTC becomes more sensitive to headlines |

| 25% Tariff Threat Gives Credibility or Comes into Effect | Rising inflation concerns + slowing EU growth | The probability of a reduction becomes lower and the macro background becomes more severe. | Risk-off pressure on BTC |

Once inflation fears are marginally eased and stock markets and interest rate cut expectations stabilize, Bitcoin will be able to participate in a broader risk-on reaction.

While ETF inflows, regulatory news, and internal market structure still have a significant direct impact on Bitcoin’s medium-term price direction, the removal of macro headwinds within a month with the next PCE release scheduled for May 28th will create a cleaner environment for risk assets in general.

This trend is less favorable if auto tariffs rise to 25% or if the market evaluates the outcome as reliable. In an environment where core PCE is already running at 3.2% and the Fed currently has no basis for cutting rates, goods inflation becomes the new source of upside.

Germany’s slowing growth adds a global slowdown to inflation concerns. Bitcoin, which trades with high equity correlations documented by the IMF, will absorb any risk-off activity due to growth concerns and a reduced likelihood of Fed easing due to strong inflation.

Assets can be maintained or recovered, but the macro winds will be in the opposite direction and the May 28 PCE print will be a referendum on how much the tariff threat is already reflected in prices.

Crypto-specific catalysts such as ETF inflows, spot market structure, and regulatory news have a more direct impact on Bitcoin’s medium-term price behavior.

If the tariff hike reignites inflation fears at a time when markets were expecting a return to disinflation, May could be another month in which the Fed’s calendar takes precedence over crypto’s internal momentum.

Two dates could confirm or close that risk window: the May 19 negotiation round and the May 28 PCE release.

(Tag translation) Bitcoin