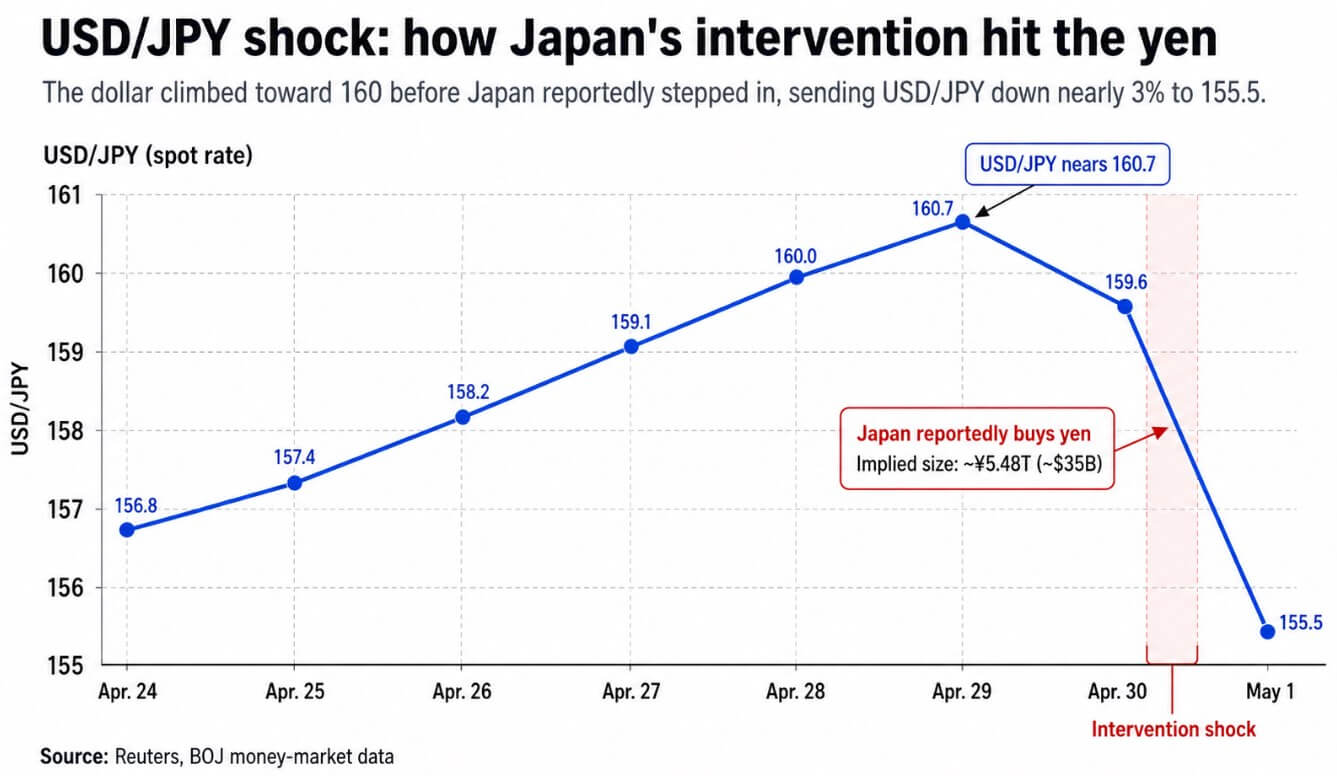

Japan reportedly entered the currency market with about $35 billion in yen purchases, sending the dollar down nearly 3% to $155.5.

Money market data from the Bank of Japan (BOJ) suggests that the scale is accurate. If confirmed in the Ministry of Finance’s monthly announcements, it would be Japan’s first official yen support measure in nearly two years and the second largest in history.

The Bank of Japan’s own forecast in April predicted that the CPI excluding fresh food would be between 2.5% and 3.0% in fiscal 2026, and economists expect inflation to accelerate again as lower oil prices and a weaker yen increase import costs.

The figures show that 95% of Japan’s crude flows through the Strait of Hormuz, and the Bank of Japan’s base case assumes Dubai crude heads towards $70-$80 without major supply disruptions.

There are limits to Tokyo’s political tolerance for inflationary imports amid a weakening yen, and those limits were broken this week.

On April 28, the Bank of Japan kept the policy interest rate unchanged at 0.75%, but three board members opposed it and insisted on keeping it at 1%. The Federal Reserve kept its policy interest rate unchanged at 3.50% to 3.75% on April 29th.

The reality of short-term interest rates, around 275-300 basis points, is the mechanical reason why the carry trade continues to restructure. Yen borrowing costs remain low compared to most countries around the world, and the spread with U.S. yields makes it attractive to invest that money in high-yielding assets.

Interventions that do not involve interest rate convergence only buy time. Reuters reported that in an April 16 poll, 65% of economists expected the Bank of Japan to reach 1.0% by the end of June 2026, with further hikes planned through 2027.

Why is the yen everyone’s problem?

According to BIS triennial survey data for 2025, the yen accounted for 16.8% of all foreign exchange transactions worldwide.

A separate BIS study on the August 2024 episode estimated carry trades in yen funds before easing to be around $250 billion, while UBS estimates the total to be closer to $500 billion, which is only about half done at this point.

Another BOJ paper pointed out that the balance sheet expansion of yen debt funds is being driven by hedge funds and financial intermediaries, long-term assets far removed from Japan’s currency markets.

According to CFTC positioning data on April 21, leveraged funds in CME Yen futures held 80,220 contracts short compared to 148,717 contracts, with total short interest increasing by more than 16,000 contracts from the previous week.

If the yen suddenly rises, you will need to cover your shorts and you will need to reduce the assets you were financing with your trades.

| metric | bank of japan | federal reserve system | Why is it important for carry trades? |

|---|---|---|---|

| policy interest rate | 0.75% | 3.50%~3.75% | Due to the large gap, yen funding is cheap and US assets are relatively attractive. |

| Latest policy decision date | April 28, 2026 | April 29, 2026 | Indicates that the rate divergence is current, not historical. |

| Current short-term interest rate gap | Approximately 275-300 bps | This spread is the central mechanical driver of carry trades with yen funds. | |

| policy bias | Three Bank of Japan board members oppose interest rate of 1.0% | Fed remains unchanged | Japan may be moving slowly towards policy tightening, but it suggests it is not yet fast enough to eliminate the spread of infections |

| market expectations | Reuters poll: 65% of economists expect the Bank of Japan interest rate to be 1.0% by the end of June 2026 | There is no equivalent immediate shift in drafts. | Bank of Japan rate hike could compress carry spreads and make short yen positions less attractive |

| Impact of carry trade | low cost funding currency | High-yield destination markets | Investors can borrow cheaply in yen and seek higher returns elsewhere. |

| Article excerpt | Interventions can shock the foreign exchange market, but only buy time in the absence of interest rate convergence | Rising US yields maintain carry incentives | Explaining why a weak yen continues to rebuild, and why a sudden yen rebound weighs on risk assets, including Bitcoin. |

BIS data also shows that yen-denominated foreign currency credit contracted by 4.9% during 2025, so the carry complex may already be slightly smaller, meaning the mechanical force for unwinding will be smaller.

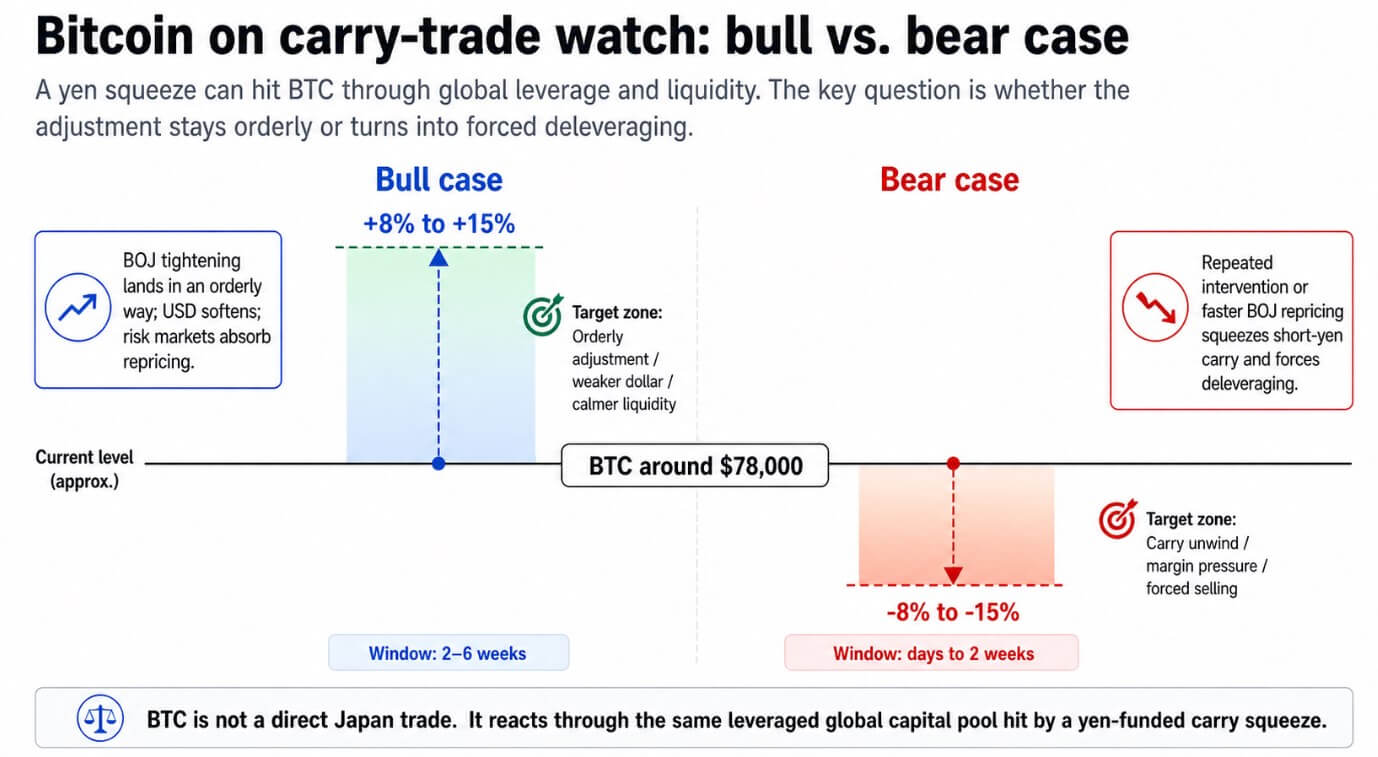

Bitcoin sensitivity is threaded through global leverage, as the same macro fund balance sheets, margin calls, and risk appetite simultaneously short the yen and long high-yield assets.

BIS’ August 2024 review found that procyclical deleveraging and margin increases amplified shocks across risk assets, causing Bitcoin to plummet 13% during the washout.

Bitcoin traded in the $78,000 zone on May 1st, reaching an intraday high near $79,000. The sudden tightening of the yen forces leveraged macrobooks to reduce their total exposure, allowing traders to sell their Bitcoin because it is liquid and held by leveraged books that need to raise cash quickly.

bull incident

If the BOJ’s three opponents are right and the June rate hike goes ahead, it would compress carry spreads, making new additions to yen short positions less attractive, and concomitantly weakening the dollar in a credible tightening cycle.

The intervention has already caused the dollar index to fall by 0.8%, while the euro, pound and Swiss franc have all strengthened. This widespread dollar weakness is a historically constructive backdrop for Bitcoin, which tends to follow global dollar liquidity.

In an orderly correction where the Bank of Japan’s June rate hike lands without triggering a chaotic unwinding, USD/JPY settles into a tighter range and global risk markets absorb reprices without cascading margin calls.

Bitcoin could overcome the initial volatility and return to the weak dollar-friendly liquidity regime that drove its rally through early 2024.

Coinbase Research’s Q2 outlook notes that 75% of institutional investor respondents believe BTC is undervalued at current levels, arguing that there is buying interest on the other side of the short-term turmoil.

In this scenario, an 8-15% recovery from current levels over a 2-6 week period would be a reasonable outcome.

bear incident

Repeated interventions, or more rapid re-pricing of the BOJ’s policy expectations, could squeeze yen short trades fast enough to force VAR and margin reductions simultaneously across macro portfolios.

In this setup, traders sell Bitcoin because it is liquid and held by a leveraged book under pressure.

The August 2024 analog serves as a reference frame, driven by the same carry mechanism and amplified by forced selling, resulting in a drawdown of around 15% in a few days.

When Bitcoin is in the $78,000 zone, holders with large profits have less cushion as they can survive a downturn.

Drawdowns of 8% to 15% are consistent with historical patterns of repeated interventions without policy support.

(Tag translation) Bitcoin