Publicly traded Bitcoin miners liquidated more than 32,000 Bitcoins in the first quarter of 2026, marking a record decline as the industry’s biggest operators channeled billions of dollars of capital into artificial intelligence.

This historic shift is unfolding just as the economics of Bitcoin validation reach a critical pressure point.

As mining profitability hovers near cyclical lows, weighted production costs soar, and network hash rates continue to show signs of strain, the infrastructure giants that defined the last crypto boom are fundamentally redesigning their business models.

Public BTC miners turn to their balance sheets

The magnitude of liquidations in the first quarter reflects the severity of the capital pivot.

Public mining companies unloaded more Bitcoin in the first three months of 2026 than in all of 2025.

To put the scale of the crash into context, offloads in the first quarter easily exceeded the roughly 20,000 Bitcoin released by the industry during the chaotic Terra-Luna collapse in the second quarter of 2022.

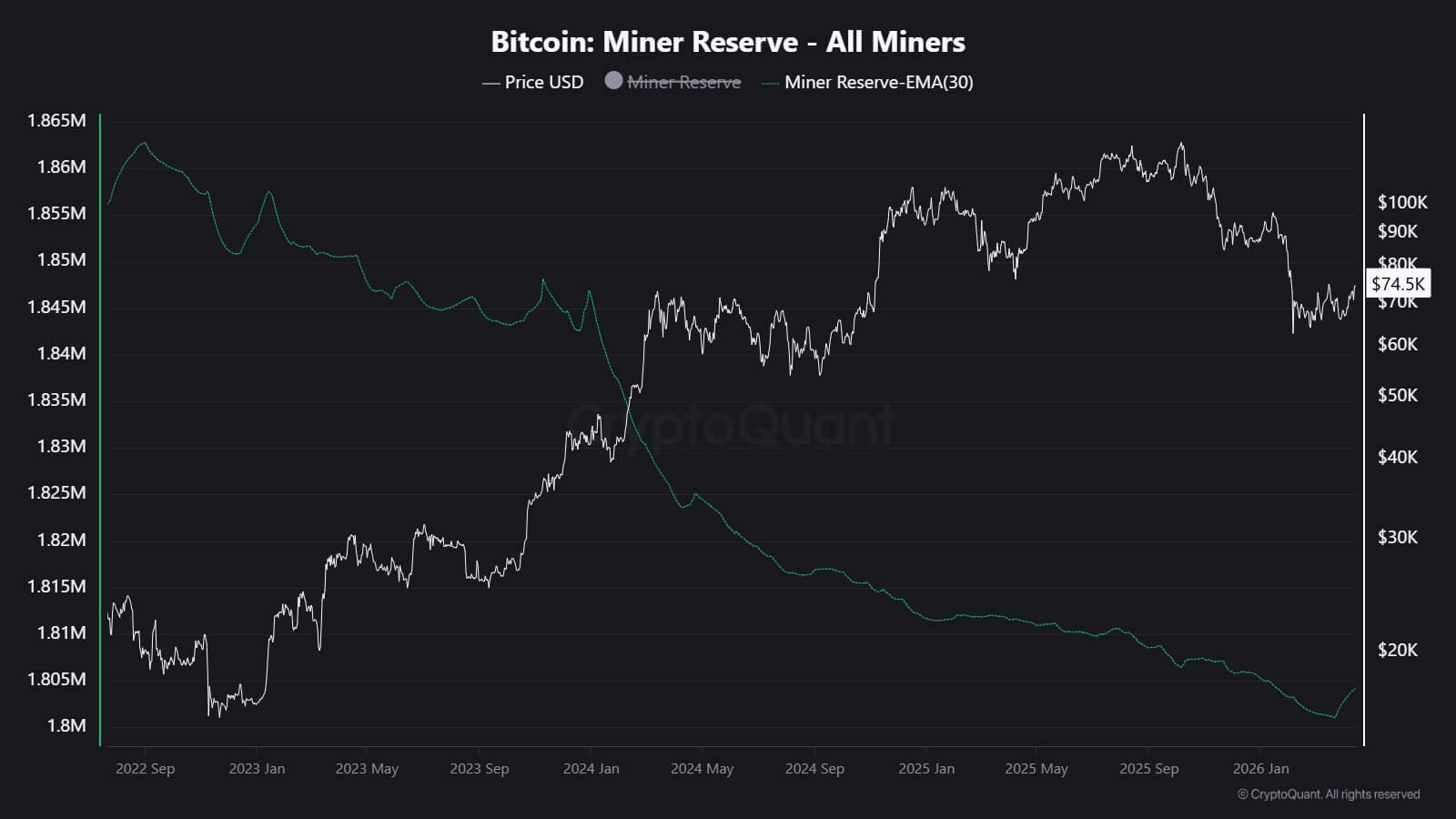

According to CryptoQuant’s on-chain data, miners’ reserves have steadily declined throughout the cycle, and prominent operators are now using digital treasuries as key liquidity engines rather than long-term strategic holdings.

The company noted that miners have recorded a net short position of 61,000 BTC since the start of the current cycle. This heavy selling activity was led by Marathon Digital, which offloaded over 13,000 BTC but has since fallen out of the top three Bitcoin holders.

Other BTC miners selling their holdings include Cango, which sold 2,000 Bitcoins for about $143 million to wipe out Bitcoin-backed debt and liquidate its balance sheet. Core Scientific unloaded around 1,900 Bitcoin in January to raise $175 million, while Riot Platforms sold 4,026 BTC.

Post-halving economics breaks old models

The driving force behind this mass exodus of capital is a broken economic model, made worse by the April 2024 halving that reduced the block reward from 6.25 BTC to 3.125 BTC.

The programmatic 50% block subsidy reduction fundamentally changes the revenue baseline price for the entire sector, leaving operators highly vulnerable to market fluctuations.

Since that cut, the economics of BTC mining have been defined by relentless downward pressure.

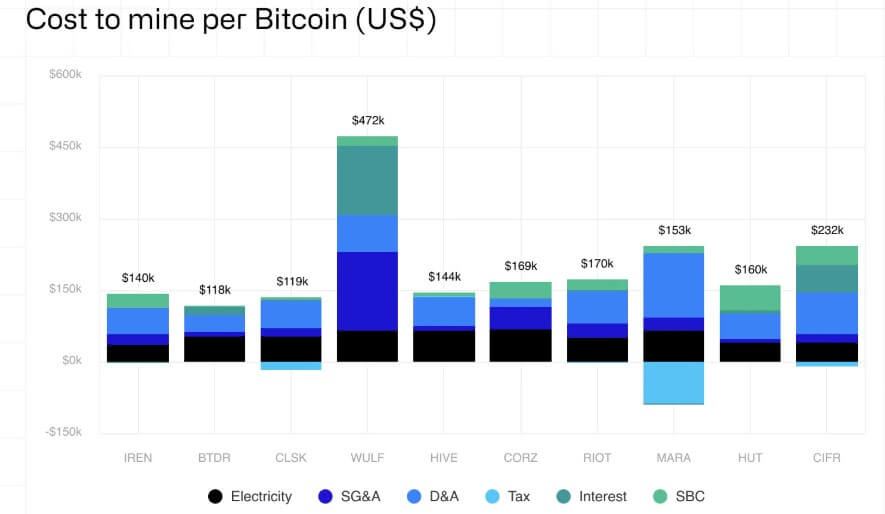

James Butterfill, head of research at digital asset management firm CoinShares, said the weighted average cash cost of producing a single Bitcoin for a utility has soared to nearly $80,000 in the final quarter of 2025.

On the other hand, profitability continues to deteriorate. HashPrice, a metric that tracks expected revenue per unit of computing power, plummeted from $28 to $30 per petahash per day in Q1 2026, hitting an all-time low in profitability.

Miners are highly dependent on spot price increases as transaction fees remain structurally weak at less than 1% of the total block reward.

However, with Bitcoin hovering around $77,000, well below the cycle peak of around $126,000 reached in October 2025, miners are in a vise.

Rising debt burdens and huge power costs have strained cash flow to breaking point, forcing executives to look elsewhere for revenue.

Why Wall Street rewards AI pivots

Pure-play companies facing shrinking profit margins are finding that boards of directors and institutional investors are willing to reward transformations to AI and high-performance computing.

Unlike the volatile, spot market nature of Bitcoin mining, AI data centers offer stable, predictable, multi-year revenue contracts with tech giants like Google, Microsoft, and Anthropic.

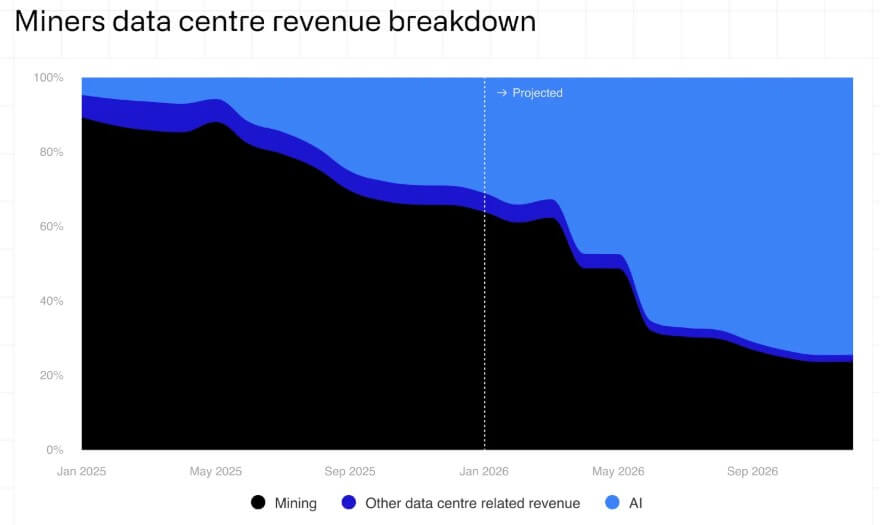

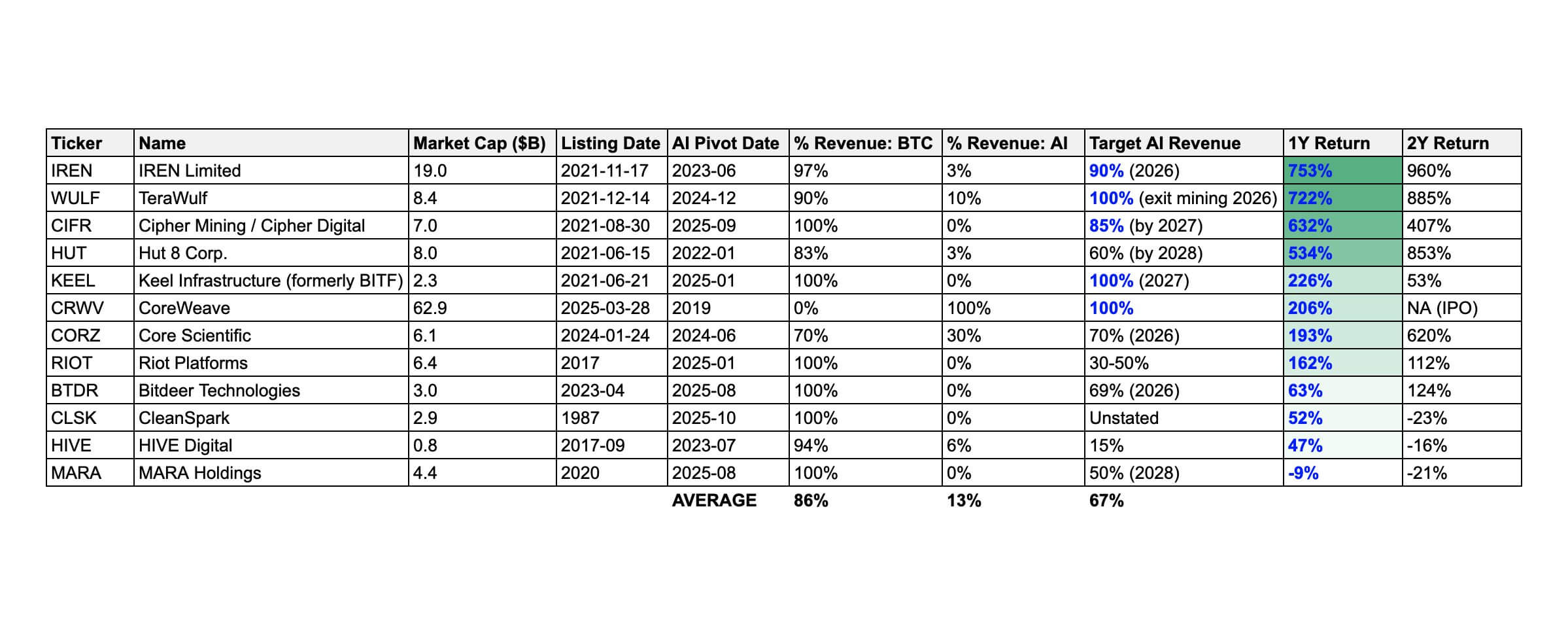

The stock market’s judgment is clear. Mining companies with AI revenue targets of 80% or higher have seen their stock prices soar an average of 500% over the past two years, commanding exceptional market multiples compared to their pure-play mining peers.

Butterfill predicts that public miners could derive up to 70% of their revenue from AI by the end of this year, a sharp jump from around 30% currently.

More than $70 billion in AI and high-performance computing contracts have been announced across the public mining sector, with funding tied up in next-generation ASIC replacement.

Instead, debt and equity are being aggregated into data center-style infrastructure. Operators such as TeraWulf, IREN, and Cipher are taking on billions in collective debt to fund these ramp-ups based on underlying unit economics.

While electricity accounts for about 40% of Bitcoin mining revenue, energy costs for AI cloud operators that lease high-performance chips are in the low single digits.

Will less investment in Bitcoin mining mean less security?

The massive shift in computing infrastructure has sparked intense debate over the long-term security of the Bitcoin network.

On the other hand, bearish theories argue that the network’s security backbone risks being hollowed out at a critical juncture, as public miners stop reinvesting in mining hardware and put their vast energy capacity into AI.

Charles Edwards, founder of Capriol Investments, views this trend with deep alarm, pointing to predictions that the average Bitcoin revenue share among top public miners will collapse to just 30% within three years.

He observed:

“If these numbers are even half accurate…the energy and commitment to Bitcoin is under serious threat.”

Adding a cultural component to this change, Bitcoin researcher Paul Stork pointed out that the industry is quietly shedding its original roots.

He said mining-specific publications were rebranded to focus on broader energy themes, and mining stages at major industry conferences were replaced with energy-focused platforms, reflecting a sector actively distancing itself from pure cryptocurrency workloads.

But protocol veterans argue that this is exactly how the system was designed to survive.

Blockstream CEO Adam Back refuted this alarmist theory by pointing to Bitcoin’s self-adjusting difficulty mechanism. Once the computing power is removed, mining difficulty decreases, instantly increasing profit margins for the remaining operators.

Buck argued.

“This is an arbitrage transaction and is balanced when the mining margin is the same as the AI workload.”

He also described a “positive reflexivity” in which higher profit margins reduce the amount of Bitcoin that surviving miners sell to cover their electricity costs.

Meanwhile, James Check, on-chain analyst at CheckOnchain, views this transition through the lens of pure capitalism. He pointed out:

“Massive turnover is literally the intended design of the difficulty adjustment.”

In his view, an AI pivot is a very logical diversification strategy for infrastructure companies that simply “buy power and compute,” noting that while AI serves as a constant baseload, Bitcoin mining remains an intermittent tool to balance grid loads.

second half of half-life

As the Bitcoin network advances into the second half of this halving era, recently surpassing 945,000 blocks in April 2026, the public mining industry is facing a serious identity crisis.

Hashrate Index argued that the next two years until its halving in 2028 will severely test the protocol’s self-correcting mechanisms against the gravitational pull of Wall Street’s AI capital.

The unresolved issues facing markets are now structural rather than cyclical. It remains to be seen whether Bitcoin’s spot price can recover enough to comfortably clear cash costs near record production costs, or whether network transaction fees will remain a small portion of total revenue forever.

If the underlying spot economy does not improve significantly, markets will be forced to consider whether the current unprecedented pace of debt liquidation can be sustained without permanently lowering asset prices.

Additionally, the industry must determine the baseline at which the network’s computing power will eventually stabilize after marginal players exit the ecosystem.

Ultimately, the most pressing tension is an existential one. By 2027, the publicly traded companies that have largely driven the industrialization of Bitcoin verification over the past five years may no longer be miners in the traditional sense.

Rather, these companies retain only residual legacy exposure to the digital assets on which they were originally built and are on track to become diversified energy and high-performance computing conglomerates.

(Tag translation) Bitcoin