On-chain fees paid by users in the first half of 2025 were $9.7 billion, an increase of 41% year-over-year and the second highest total on record.

1kx predicts on-chain fees will exceed $32 billion in 2026 due to accelerating application growth. This growth has made the word “revenue” a part of every crypto investor pitch deck, every sector report, and every valuation conversation.

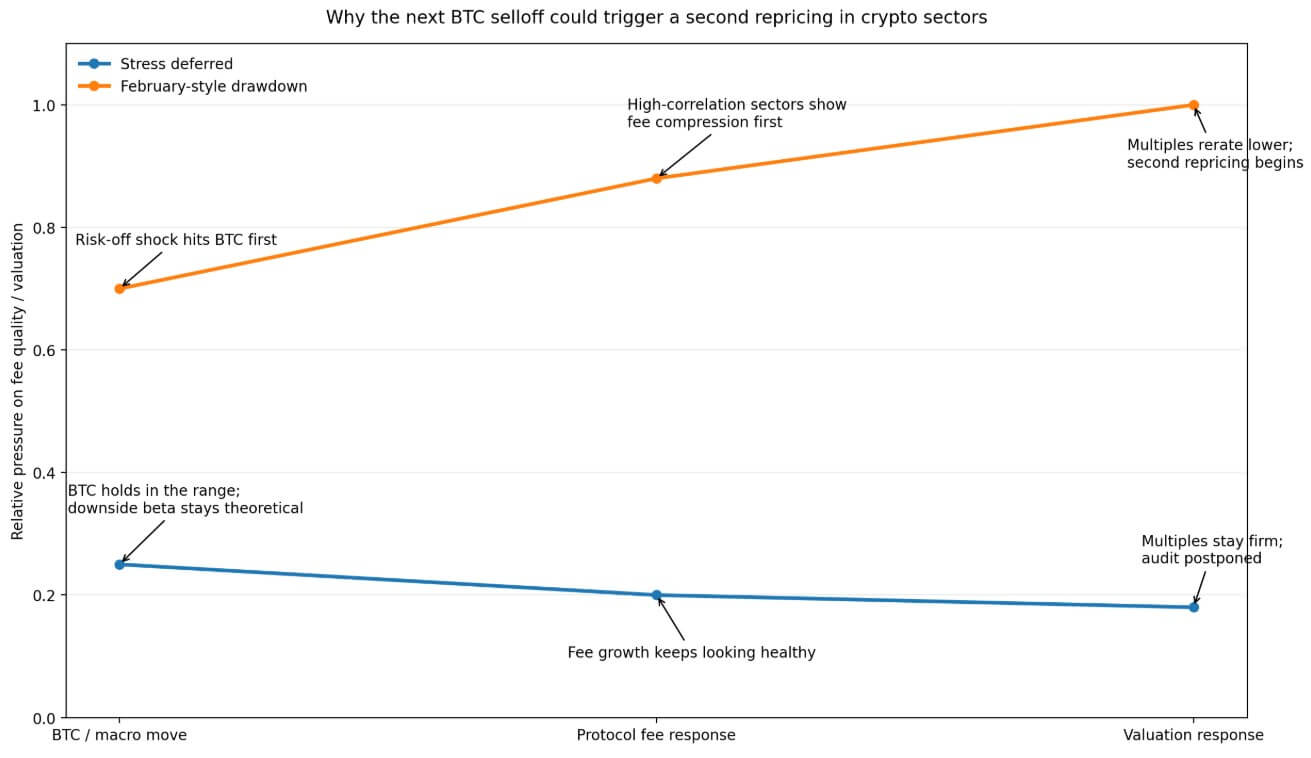

The report added that Bitcoin’s drawdown could result in a stress test for protocol fees.

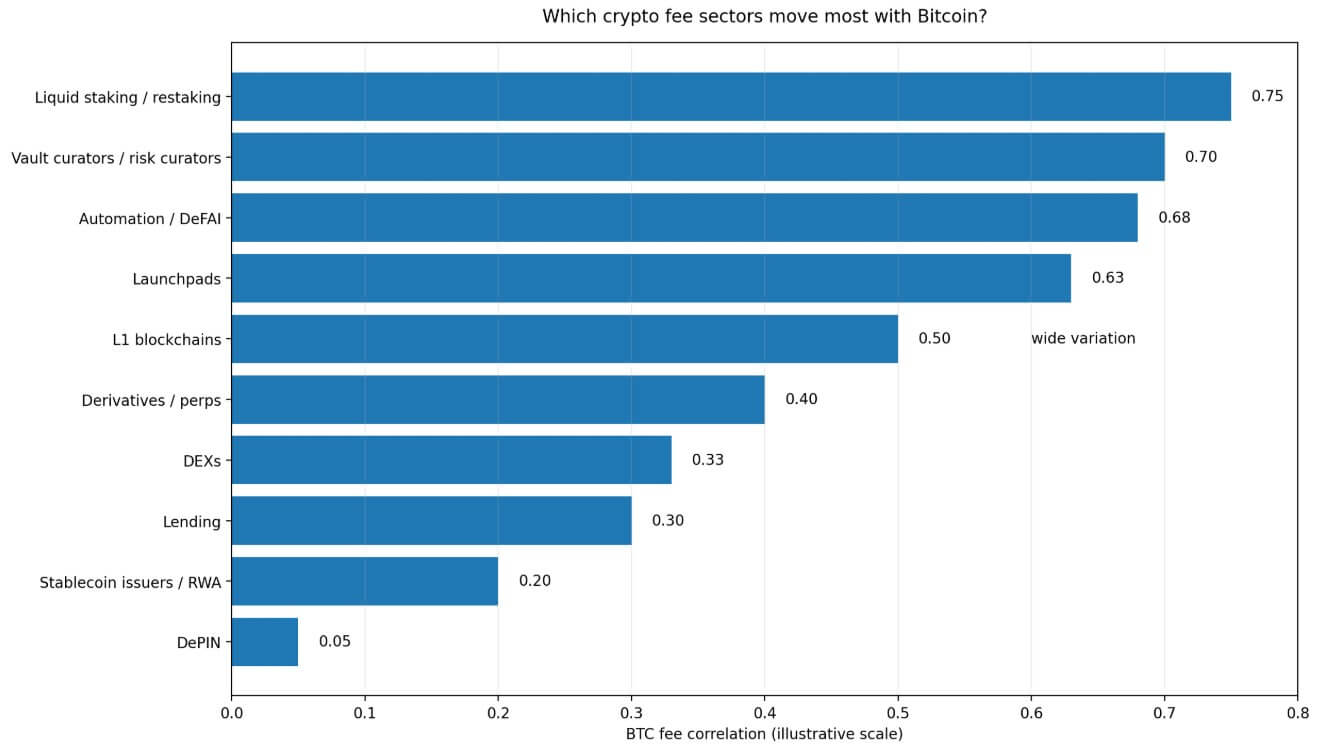

1kx’s April sector analysis found that nearly all cryptocurrency fee categories are positively correlated with BTC price. There is also wide variation across sectors, and the key variables of downside beta are still unresolved.

The company notes that a 0.6 correlation means very different things depending on whether sector fees fall at 0.8x or 1.5x the pace of Bitcoin, and that the sensitivities of up and down fees can be decomposed and identified.

In cryptocurrencies, fee lines can look like bull market business but trade like amplified BTC beta when macro fears arrive.

reflexive price cluster

The sectors that 1kx has identified as most correlated with Bitcoin price share a common economic structure that improves as prices rise and worsens as prices fall, often faster than the underlying asset itself.

Liquid staking and restaking sit at the top of that cluster, with fee streams dependent on yields that expand as borrowed capital and risk appetite expands, and contract as they retreat.

Vault curators face similar temptations, as assets flow in when price momentum is positive and assets flow out when sentiment reverses. Launchpad is the most sentiment-driven category in the report, with launch activity accelerating when there is a bullish trend and stalling when confidence collapses.

Automation protocols and DeFAI protocols that earn fees related to transaction activity and strategy deployment also track the same directional pulse.

According to 1kx, the correlation of fees to BTC for Layer 1 (L1) blockchains varies widely, with many inheriting market direction through the price movements and activity mix of their native tokens, while others exhibit more independence depending on their application base.

This volatility means that most L1s still retain meaningful BTC sensitivity to the fee line due to directional increases in the token price in on-chain activity.

Reflexivity unites these categories, as these fees are primarily the product of the same speculative, position-driven activity that powers Bitcoin itself.

When investors talk about rising fees in these sectors when markets are up, they are partly explaining business momentum and partly the same macro tailwinds that have pushed up all risk assets in their portfolios.

Service layer provided

DePIN stands out as the lowest correlation category within 1kx’s framework and is distinguished as a standout for non-directional crypto revenue exposure.

The reason is that DePIN fees track the amount of compute, bandwidth, storage, and other services provided. Demand for these services comes from users with real operational needs, and while token prices influence the incentive structure, they do not directly set commission rates the way asset prices do for yields and starting activity.

1kx projects DePIN fees to exceed $450 million in 2026 and maintain triple-digit growth.

Stablecoin issuers and real-world asset protocols similarly sit in the low correlation range, with 1kx estimating their BTC correlation to be around 0.2. The economics of their fees depend heavily on issuance, reserve management, and assets under management, as well as speculative trading.

A low correlation indicates that the fee structure is not very tied to the direction of BTC price. 1kx’s framework supports “more differentiated return exposure” and is far from claiming immunity from declines.

A more accurate argument is that businesses linked to DePIN and issuance have a better structural basis for defending the fee line during BTC-specific drawdowns.

| sector group | main fee driver | Action in a rising market | Possible stress during drawdown | Article excerpt |

|---|---|---|---|---|

| Liquid staking/re-staking | Yield, leverage, risk appetite | Prices grow rapidly | Compression occurs and activity weakens | most reflective |

| Vault Curator | AUM, momentum, inflows | AUM increases with price | Outflows may occur faster than BTC | High downside sensitivity risk |

| launchpad | emotions, start an activity | Strong in bullish situations | Boot volume may stop rapidly | Highly cyclical |

| Automation / DeFAI | Strategy development, trading activities | Benefit from an active market | Risk appetite may reduce usage | Directional fee exposure |

| Depin | Compute, bandwidth and storage demands | Growth based on service usage | Additional protection from BTC-specific shocks | the most differentiated |

| Stablecoin / RWA | Issuance amount, reserves, balance of assets under management | slower growth | Not directly related to BTC movements | Lower correlated fee exposure |

| DEX / Financing / PERP | Volume, rate, volatility, leverage | can benefit from the activity | mixture. Volatility helps, but lessens the pain | A contested middle ground |

Decentralized exchanges (DEXs), lending protocols, and perpetual platforms occupy a contentious middle ground. At 1kx, the median DEX correlation is around 0.33, loans around 0.3, while derivatives show large fluctuations, exceeding 0.4 in some cases.

Volatility supports trading volumes even in down markets, providing a partial buffer for these sectors. Still, compression of commission rates and relaxation of positions during stress episodes makes the return line more volatile than simple average correlation can capture.

Why is valuation really profitable?

1kx’s extensive earnings report shows that price-to-fee ratios across the crypto sector span orders of magnitude. The median P/F ratio for blockchain in Q3 2025 was 3,902x, compared to around 7,300x for L1 and 17x for DeFi and finance.

DePIN’s median P/F ratio fell to 211x from approximately 1,000x in the year-ago period. Even though DeFi and finance generate the majority of fees, blockchain valuation still accounts for over 90% of the analyzed fee-generating market capitalization.

1kx also notes that changes in fees will drive valuations in DeFi, finance, and to a lesser extent blockchain.

If this directional relationship remains downward, with fees initially declining and multiples compressing in the weeks following the initial price move, a BTC drawdown exposing fee vulnerabilities in highly correlated sectors could trigger a secondary valuation correction.

Investors who had assigned a Business Quality rating to a Beta published fee stream will now face rapid price changes.

test is postponed

If the macro environment continues to ease, including falling oil prices, sustained expectations for Fed rate cuts, and declining geopolitical risks, Bitcoin could remain solid in the mid-to-high $70,000s and move toward Citi’s 12-month benchmark target of $112,000.

In that environment, fee lines for most sectors will continue to widen and downside beta will remain theoretical. 1kx predicts that application-driven fee growth will accelerate through 2026, with DeFi and finance expanding by more than 50% year over year.

The risk in this scenario is that the market continues to treat periodic strong fee growth as evidence of sustained business quality. Launchpad activity remains high in a buoyant market, restaking yields look solid when risk appetite is healthy, and Vault curators are reporting high AUM numbers.

Audits are postponed and capital continues to flow into sectors where the quality of fees has never been tested under real stress. The environment of falling oil prices, easing inflation concerns, and a resurgence of bets that the Fed will cut interest rates is exactly the kind of environment in which that postponement will increase.

February repeats on a grand scale

On February 5, Bitcoin fell 14.1% in a single session to an intraday low of $62,254.50 as risk sentiment weakened, tech stocks sold off, and ETF outflows accelerated.

During this episode, the cryptocurrency market lost about $2 trillion from its October peak. Launchpad activity has cooled, debt capital positions have been unwound and restaking yields have been compressed.

The price line, which was impressive until the end of 2025, showed directional dependence within a few weeks.

If this pattern repeats, questions about downside beta will move from the next step stated by 1kx to a live market event.

Sectors with reflexive fee structures will face the most scrutiny. The market is looking for a launchpad, we are seeing a decline in launch volumes, re-staking yields are compressed as borrowed capital exits, and vault curators are seeing AUM fall faster than token prices.

Businesses related to DePIN and issuance will still face headwinds, but for the first time the relative fee resilience will become discernible in the data.

The same mechanism works in reverse when DeFi and financial valuations increase due to fee changes.

Protocols that report fee compression in the first quarter of the next down cycle give the market a reason to compress fees before the overall picture is resolved.

Investors who had assigned a Business Quality rating to a Beta published fee stream will now face rapid price changes.

Bitcoin currently sits at around $78,000, near the top of its recent range from April’s geopolitical relief rally, precisely during the period when the quality of fees issue remains unresolved.

(Tag translation) Bitcoin