A recent paper by the Bitcoin Policy Institute on Taiwan begins with the familiar argument that the country’s foreign exchange reserves are overly concentrated in the dollar. Gold is below its potential and Bitcoin could complement both.

Readers who stop there will miss the more important arguments buried within the blockade and invasion framework of pages five to seven. There, the paper attempts to redefine the causes of reserve asset failure.

Traditional reserve analysis judges assets based on liquidity, price stability, and credit quality. BPI’s paper adds a fourth test. Can assets still be moved, consumed, and mobilized if a sea route is blocked, a host country withdraws storage access, or another state becomes politically hostile?

By that measure, gold can stay, dollar reserves can become conditional, and Bitcoin can remain electronically portable regardless of physical access or diplomatic status.

This is a bigger conceptual move than claiming Taiwan’s BTC position.

Why this is important: This marks a shift from traditional reserve thinking. Assets such as government bonds and gold, while remaining valuable on paper, can become difficult or impossible to use under sanctions, conflict, or political pressure. If reserve managers start prioritizing access over stability, Bitcoin will enter the discussion as an emergency asset rather than a return play.

From macrobets to sovereign insurance

For years, state-level Bitcoin discussions have moved along a single path: hedge against currency depreciation, diversify reserves, and capture upside from adoption momentum.

This argument still appears in BPI papers, particularly in its pages on U.S. debt accumulation and the expansion of the Federal Reserve’s balance sheet. A more original contribution lies elsewhere, with the paper ranking reserves by whether they are accessible under duress.

Governments simply need to accept that the Treasury, correspondent banking networks, physically stored metals, and foreign government debt have different dependencies.

Policy questions focus on which assets remain accessible if management, transportation, or host country politics go awry.

Official reserve movements have already confirmed that the framing extends far beyond Bitcoin supporters. According to a report by the IMF, total international reserves, including gold, reached SDR 12.5 trillion at the end of 2024.

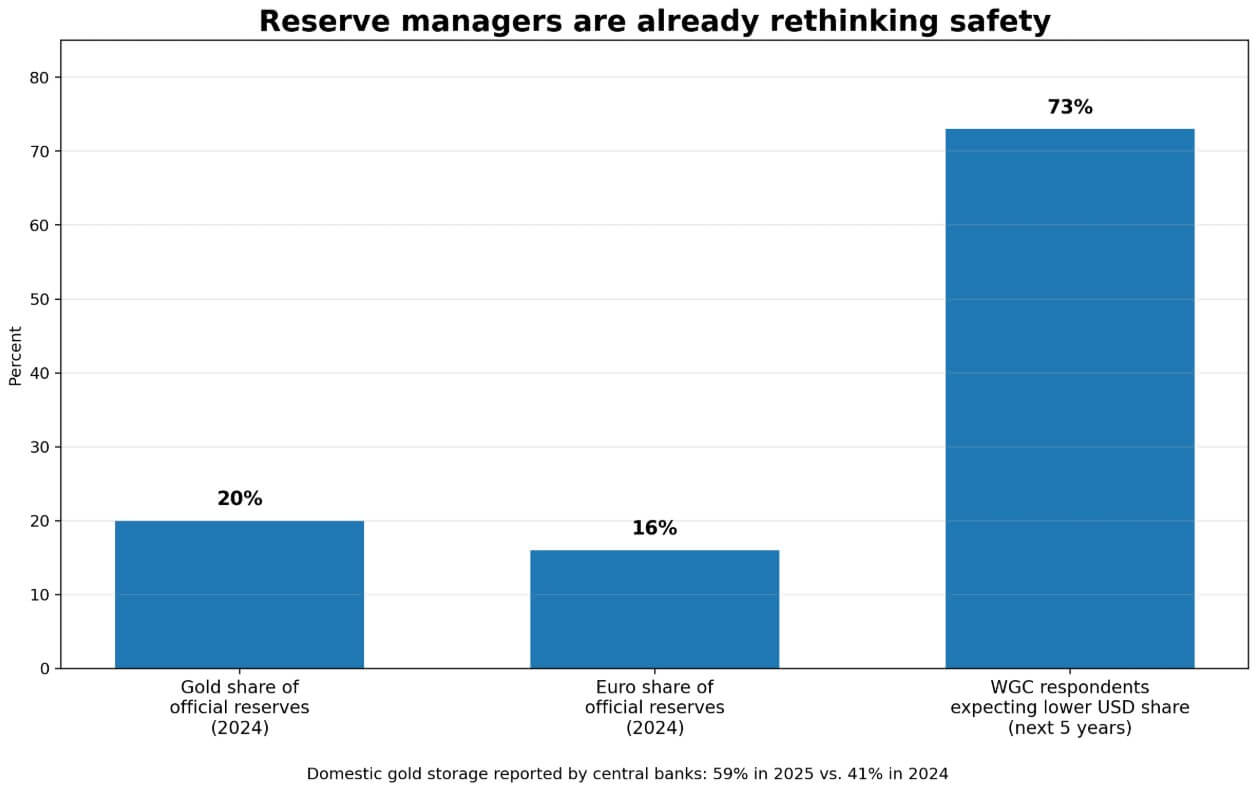

The ECB reported that gold’s share of the world’s official reserves will reach 20% in market value terms in 2024, exceeding the euro’s 16%, with central banks purchasing more than 1,000 tonnes that year.

The World Gold Council’s 2025 survey found that 73% of respondents expected US dollar holdings in global foreign exchange reserves to decline over the next five years, and the proportion of central banks reporting domestic gold storage rose to 59% from 41% a year earlier.

Reserve managers have already expanded their definition of reserve risk, and the BPI paper extends that logic to Bitcoin as well.

| assets | Strength in normal times | critical vulnerability | Failure modes under stress | Why is it important in the article? |

|---|---|---|---|---|

| US dollar reserves / government bonds | Abundant liquidity, high creditworthiness, and global reserve standards | May be politically constrained by host country policies, sanctions, or custody implications | Freeze / Conditional Access / Political Pressure | It shows that while reserves remain “safe” on paper, they become harder to spend in practice |

| gold | Long-standing reserve ballast widely accepted by public institutions, inflation hedge | Difficult to move quickly, easily trapped physically, prone to seizures and transportation bottlenecks | Stranding/seizure/logistics failure | Learn why portability and physical control are becoming more important in reserve analysis |

| Bitcoin | Digitally portable and mobile, like a courier, without the need for transport routes or physical transport. | High volatility, governance burden and limited public sector acceptance | Institutional reluctance/policy hesitationrather than physical immobilization | Rather than a traditional safe stockpile, it enters the story as a potential asset for accessibility as a last resort. |

| Diversified Non-Dollar Sovereign Paper | Fits into traditional reserve frameworks while reducing dependence on a single reserve issuer | Still dependent on external sovereign systems, payment infrastructure and market access | External dependence/decreased neutrality | Acts as an alternative in case of bears: reserve managers may prefer this to BTC even after accepting access risk |

| gold stored domestically | Improve control over storage management while maintaining gold reserve role | Still suffering from transportation friction and limited portability during acute crisis | movement restrictions Rather than a pure custody risk | Showing why gold can benefit from the same access risk logic without completely resolving it |

Living proof of access risk

The access risk debate draws strength from concrete recent events.

In March, Russia’s central bank objected to an EU freeze that affected about $300 billion of sovereign funds. This conflict keeps the central premise in play. Reserve assets can become politically immobile, retaining their par value.

Assets that are owned on paper but frozen in practice no longer serve as reserves, regardless of their credit rating.

Brazil’s central bank drew a similar conclusion. On March 31, Brazil increased the proportion of gold in its reserves from 3.55% to 7.19% in a single year, while lowering the proportion of the US dollar to 72, as a driver of diversification.

BPI’s paper argues that Bitcoin belongs to similar decentralized calculations, particularly reserve determinations based on geopolitical logic.

The US Strategic Bitcoin Reserve adds a separate data point. The White House order prioritizes confiscated BTC reserves, prohibits outright sales, and considers additional acquisitions only on a budget-neutral basis.

This would pull the language of the Bitcoin reserve into an actual sovereign control structure, setting a precedent regardless of its unconventional funding source.

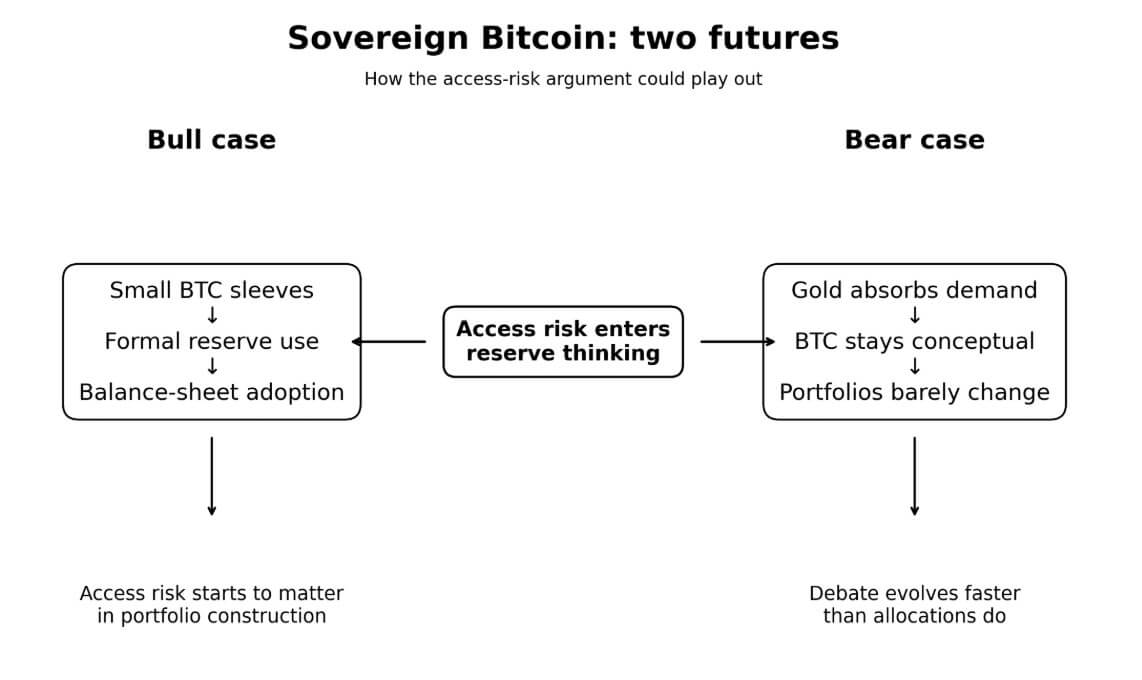

Two futures in the sovereign Bitcoin debate

The scale makes the bull’s case concrete. Taiwan’s foreign exchange reserves total approximately $602 billion, with a 1% Bitcoin sleeve of approximately $6 billion and a 5% sleeve of $30 billion.

More extensive calculations are more rigorous. 0.1% of global reserves, roughly $16.25 billion, represents about 1.2% of Bitcoin’s total market capitalization at its current price of nearly $68,000.

Participation in the reserve system, however small, will affect prices long before central banks make major allocation decisions.

In a bullish case, a small number of politically exposed or sanctions-conscious states would first need to formally form small BTC positions in the 0.25% to 1% range, or treat already seized or mined Bitcoin as reserve assets before making additional purchases.

Ferranti’s sanctions risk modeling supports this direction. In one sanctions scenario, his model generates an optimal Bitcoin share of approximately 5% for exposed sovereigns. The discussion around sovereign Bitcoin will then move from advocacy documents to actual balance sheet inclusion.

The bear case accepts the access risk criticism and still concludes that Bitcoin will lose.

Recognizing the logistical dependencies of physical gold and the political dependencies of dollar reserves, reserve managers determined that Bitcoin’s volatility, governance burden, and near-zero acceptance by government departments meant that Bitcoin’s holding power was weaker than that of domestically custodial gold or diversified non-dollar sovereign paper.

Gold will absorb the demand for diversification that access and risk arguments were thought to create for BTC, and Bitcoin’s role as a reserve asset remains conceptual. The discussion evolves while the portfolio maintains its composition.

Where discussions are successful and where there is tension

The BPI thesis is strongest when it treats portability and seizure resistance as true reserve properties based on observable reserve behavior.

The framework tracks official data. Geopolitics is now visibly influencing the composition of foreign exchange reserves, and the desire to hold assets that are not concentrated in a single counterparty is real and is already driving portfolios.

If adoption momentum or price increases are included as evidence that a policy case has been resolved, the paper goes too far. Public authorities continue to focus on acceptability, legal clarity, and operational practices alongside access risk, making these factors important factors not addressed in portability rankings.

The most reliable version of this paper’s argument is the position stated by the paper itself. In other words, Bitcoin is a little access-optimized insurance sleeve alongside gold.

For most of Bitcoin’s history as a reserve policy topic, the central question for government officials was whether Bitcoin was safe enough to hold. This framework consistently penalized BTC as its volatility was lower than that of U.S. Treasuries and gold by every conventional measure.

Reserve managers are now focused on which assets can be deployed even in the event of a hostile geopolitical environment. The resurgence of gold, preferential treatment of domestic vaults, reserve disputes due to sanctions, and fragmentation of payments infrastructure all indicate that reserve managers are already seeking traditional assets.

Bitcoin proponents have inserted BTC into the same conversation, and BPI’s paper shows how that argument works in its most sophisticated form.

(Tag translation) Bitcoin