Bond markets, not just oil, could decide Bitcoin’s fate this week

Markets are still treating oil as the center of the current macro shock.

After this weekend, market conditions will likely be heading in a different direction. Oil is the flashpoint, the bond market is the channel, and Bitcoin trades within that channel as the week begins.

That’s the situation facing investors now.

Geopolitical shocks are still having an impact. A single move in oil could reshape inflation expectations, complicate central bank decisions and hurt risk sentiment. But the bigger question is how that energy shock is impacting sovereign debt markets, at a time when investors were already questioning how much inflation relief they could realistically expect in 2026.

This shift in focus moves the conversation from oil to yields, from yields to global bond prices, and then directly to Bitcoin.

Bitcoin operates in a market where the long end of the curve can no longer be ignored.

The long end is under pressure right now.

The core theme is simple and clear. While markets have already priced in the risk of war through energy, the next re-pricing phase will focus on whether the energy shock persists enough to keep long-term yields rising, delay policy easing, and tighten financial conditions overall.

All risk assets feel that process, and Bitcoin is particularly close to it because it still straddles two roles. In the short term, it behaves like a liquidity-sensitive macro asset. Over longer time horizons, it still has an appeal as a hard asset hedge.

That tension is at the heart of the current setup.

The Kobisi letter came close to getting the right frame this weekend, arguing that oil prices are no longer the only threat to markets and that bond markets will play a major role in determining how long the US can maintain pressure on the Iran conflict. The key takeaway from this discussion lies in how markets work.

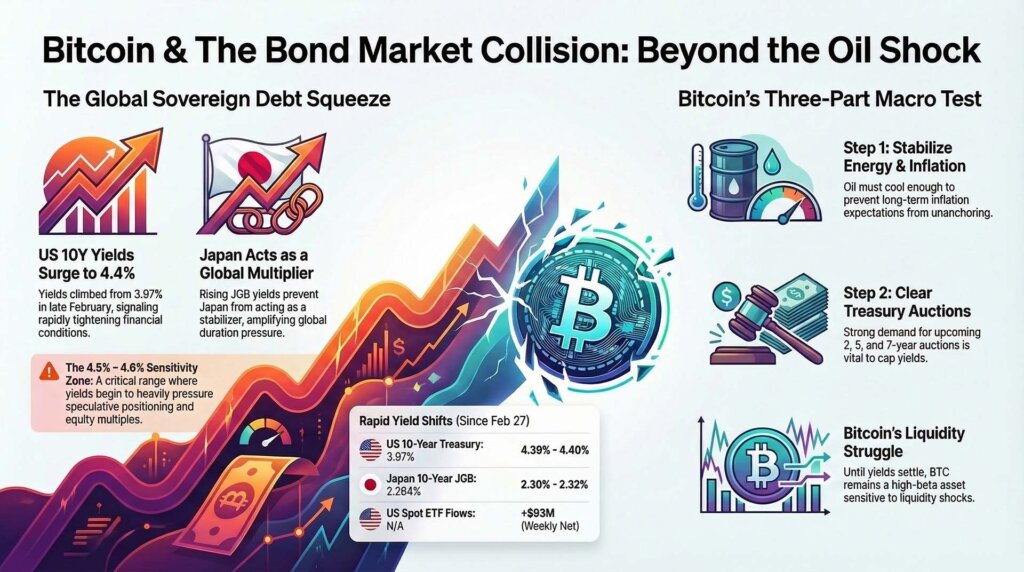

The yield on the US 10-year Treasury note has risen sharply since the war began on February 28th. It rose from 3.97% on February 27 to 4.39% by March 20, according to official Ministry of Finance data, before pushing back to around 4.4% in live trading on Monday. This move is large enough to confirm that yields are rising rapidly and bond markets are putting real pressure on broader financial conditions.

Yield zone becomes a binding constraint on risk assets

The 10-year 4.50% to 4.60% zone requires more careful discussion. This is best interpreted as a politically and fiscally sensitive area rather than a fixed tripwire that forces an immediate response.

Markets rarely move with such precision. Still, recent experience suggests the White House is paying close attention should the long end rise enough to threaten the broader risk picture.

In the case of Bitcoin, the meaning is clear. The central question is no longer limited to whether oil prices will rise. The more important question is whether oil remains strong enough to sustain inflation concerns and push yields into a range that simultaneously weighs on duration, equity multiples, and speculative positioning.

That’s why the yield response deserves investors’ attention.

The broader macro background offers little reassurance.

Last week, the US Federal Reserve kept interest rates unchanged at 3.75% from 3.50%, signaling that the situation in the Middle East was adding further uncertainty to the policy outlook. Surrounding data reinforced that sense of caution.

The CPI in February was 2.4% compared to the same month last year, and the core was 2.5%. PPI rose further on a monthly basis in February. Employment growth slowed and consumer sentiment weakened. Preliminary figures from the University of Michigan for March also showed inflation expectations rising, with gas prices standing out as a visible pressure point for household finances.

This combination will leave the market in a difficult situation, with a resurgence of inflation fears and a modest growth signal.

Bitcoin tends to struggle when its combinations start directly impacting the term premium.

Japan deserves a bigger place in the conversation now

One of the most underappreciated risks in the current environment is that this extends beyond the U.S. Treasury’s actions. Japanese government bond yields have also been rising since Friday, with the 10-year government bond rising from 2.264% on March 20 to a range of approximately 2.30% to 2.32% on Monday.

Long-term bond yields rose as well, with both 30-year and 40-year bonds rising.

At the same time, 10-year Treasury futures failed to rebound convincingly after Friday’s selloff, remaining locked near recent lows.

This development adds a new layer to macro pressures.

Japan is important in global duration markets because rising government bond yields can impact capital flows, relative rate pricing, hedging decisions, and broader costs around the world.

As Treasury prices rise while U.S. Treasuries and Treasuries remain under pressure, markets begin to treat the energy shock as a global bond market event rather than a localized oil panic.

This change brings new challenges to Bitcoin.

The Bank of Japan reinforced this theme last week, acknowledging that oil prices have risen significantly and warning that higher oil prices will put upward pressure on consumer prices.

The Bank of Japan did not signal panic, but it also failed to allay the sense that inflation risks are widening. Markets are already pricing in a high probability of another Bank of Japan rate hike, and reports that Japan is considering cutting back on its inflation-linked bonds have added to the sense that domestic inflation expectations are rising again.

As a result, Japan will function less as a stabilizer and more as an amplifier.

Bitcoin traders often desire to treat their assets as digital gold during times of geopolitical stress. Price trends so far point to a more mixed reality. When the oil shock occurred, traders sold their Bitcoins rather than transferring them to traditional havens. This response does not invalidate hard asset litigation over the long term. You can see that timing plays an important role.

Bitcoin could attract more defensive bids later on, especially if policy responses to slowing growth become more aggressive, or if investors start to focus more on the credibility of fiat currencies and the sustainability of sovereign debt. In the first stage of the liquidity shock, rising yields are still creating a difficult backdrop.

The coming week will carry an unusual weight.

This week does not include the usual PCE inflation anchor as the February US PCE has been postponed to April 9th.

As a result, markets become more dependent on secondary signals. This has increased the importance of inflation expectations based on Treasury auctions, PMI data, unemployment claims, and surveys.

These releases form the scoreboard for the week.

Tuesday’s preliminary PMI will give us an early indication of whether business activity is absorbing the shock or is starting to wobble. Two-year bond auctions will be held on the same day, followed by five-year bond auctions on Wednesday and seven-year bond auctions on Thursday. On Friday, the University of Michigan will release its final sentiment measure and updated view on inflation expectations.

If the auction results are weak and inflation expectations data remain strong, the 10-year interest rate could quickly move towards the mid-4% range. In that environment, Bitcoin will remain under pressure even if oil supplies are temporarily suspended. In that scenario, BTC is likely to remain within the market’s liquidity bucket as investors reprice higher in a longer-term situation.

Other paths are also possible. If auctions go well, PMIs soften enough to dampen the long end, and inflation expectations cool, yields could stabilize even without a dramatic collapse in oil prices. That would open up a more constructive path for Bitcoin.

Markets could begin to shift from near-term concerns about persistent inflation to a broader view that shock-hit growth will eventually outpace the energy surge itself.

That’s the point at which Bitcoin’s hard asset appeal could start to come back into the conversation more strongly.

Bitcoin market structure still appears to be intact

Although spot prices have retreated from recent highs, institutional demand remains evident in some parts of the market. U.S. spot ETF flows for the week ending March 20 were still net positive overall (+$93 million) despite a weak final session.

The futures basis also remained positive. This combination suggests that the market is not facing a widespread implosion, but is still engaged and highly sensitive to the macro environment.

So the focus returns to bonds.

Bitcoin’s next move may depend less on the next oil price spike and more on whether the bond market deems the inflation shock to be temporary or persistent. The oil caused the first shock. How tight the financial situation will be is determined by the Ministry of Finance, and Japan is increasing its repricing rather than easing it.

Bitcoin faces a three-part macro test this week.

- Will oil stabilize quickly enough to prevent inflation concerns from escalating further?

- Can government bond auctions prevent long-term interest rates from rising further?

- Can Japan avoid turning the decline in US Treasuries into a broader global duration squeeze?

If these pressures continue to build, Bitcoin will likely remain under stress and trade like a high-beta macro asset. As markets begin to uncouple the stress of an impending war from the broader financial path ahead, Bitcoin has room to recover if these pressures begin to ease, even partially.

Therefore, the current setup runs deeper than crude oil alone. Oil is lighting the fire, bonds are determining how far it spreads, and Japan adds to the evidence that sovereign debt repricing is global.

Until the interest rate market calms down, Bitcoin will remain in limbo.

(Updated 11:23 GMT: Interest rates approaching 4.5% coincided with President Trump issuing a statement declaring that “the United States and the State of Iran have had very good and productive discussions over the past two days regarding a complete and complete resolution of hostilities in Iran.” In the Middle East, Bitcoin immediately rose 4.5%.)

(Tag translation) Bitcoin