The UK’s bond unrest once again calls into question the very purpose for which Bitcoin was created: sovereign debt and trust in financial management begins to crack.

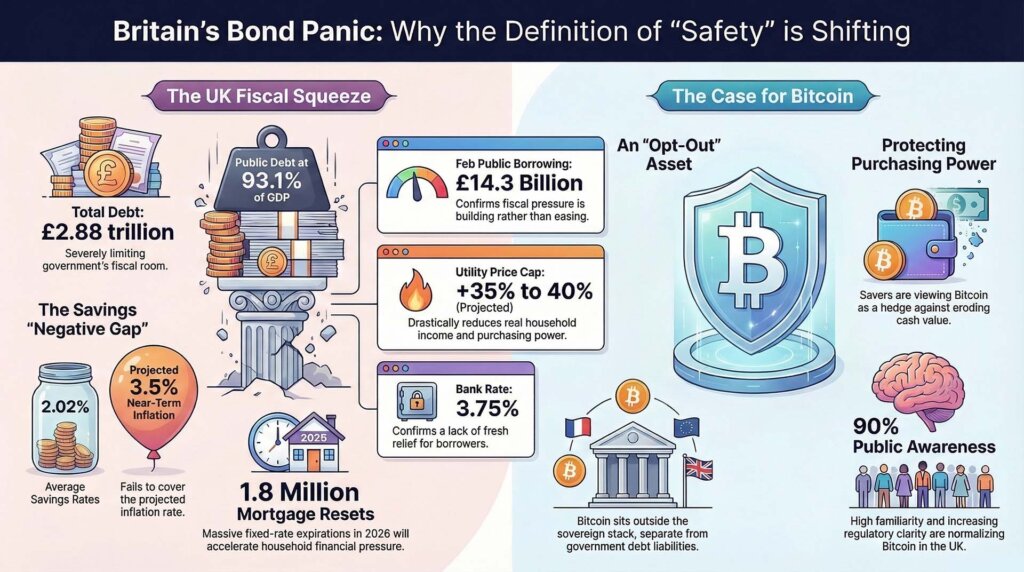

Britain’s fiscal strain deepened after official borrowing data showed public sector net borrowing rose by £2.2bn year-on-year to £14.3bn in February, making it the second-highest February figure since records began in 1993.

Net public sector debt reached £2.88 trillion, or 93.1% of GDP. On the same day, the Bank of England kept its bank rate unchanged at 3.75%, warning that the recent energy shock would cause inflation to rise again over the coming quarters, at the same time as fuel and utility bills for households would rise.

The immediate market reaction is on government bonds, interest rate expectations, and mortgages. Gradual changes appear in savings behavior. The UK does not need to rush into Bitcoin for assets to enter the conversation in new ways. New doubts about cash, government bonds and the slow pace of rate cuts are enough to change the way savers rank risk.

That change begins with arithmetic, not ideology. The Bank of England said in its latest minutes that preliminary staff forecasts are for CPI inflation to be between 3% and 3.5% in the coming quarters. He also expressed the view that increases in household fuel and utility costs will put pressure on real incomes. By January, the average interest rate on household instant access deposits was 2.02%, according to the central bank’s own data.

The easily accessible cash payments are therefore lower than the central bank’s own current expectations for inflation. The difference is clear, approximately 0.98 to 1.48 percentage points below the short-term CPI path. For savers, the definition of safety starts to change from there. Cash still protects nominal value. It does little to protect purchasing power.

The UK home channel is also making rapid progress. The UK Treasury’s latest forecasts estimate that around 1.8 million fixed rate mortgages will end in 2026. The Office for National Statistics has already shown in its Household Cost Index that inflation will be 3.6% for all households and 3.7% for mortgage holders in the fourth quarter of 2025. This was announced before the central bank recently warned that energy prices would push costs up again.

The chain of events in the UK runs through government borrowing, the re-pricing of gold and silver, and household finances. Gilt doesn’t seem very calm. Easily accessible cash undercuts short-term inflation paths. Mortgage pain will hit even more households as fixed contracts expire.

Bitcoin is gaining relevance in that setup as savers consider whether smaller assets outside of the sovereign stack should be included in the mix.

| indicator | latest figures | How the saver behavior changes |

|---|---|---|

| February public borrowing | £14.3 billion | Shows that fiscal pressures are still increasing rather than easing |

| public debt | 93.1% of GDP | There is limited room for a clean fiscal reset. |

| bank rate | 3.75% | Confirms that banks did not provide new relief |

| Central bank’s short-term CPI outlook | 3%~3.5% | Points out new pressures on real incomes |

| Deposit rates for instant access | 2.02% | Easy cash remains below banks’ inflation range |

| Mortgages will be reset in 2026 | 1.8 million | The impact of rising interest rates on household finances will accelerate |

The squeeze starts with cash flow and extends to portfolio choices.

The Bank of England’s latest explanation of the shock provides cross-market context. In a March statement, the Bank highlighted that around a fifth of global oil and LNG supplies typically pass through the Strait of Hormuz, that Brent crude and Dutch TTF gas prices were around 60% above pre-shock levels, and that UK gas futures suggested the next Ofgem cap could rise by 35% to 40%.

This is the bridge between macro data and retail savers. Unless households change the way they think about money, the government could run huge deficits for years. However, your utility bill will skyrocket every month. Mortgage resets can be completed by letter and direct debit. This is the moment when savers start weighing the trade-offs between purchasing power, liquidity, volatility, and trust in the issuer.

This distinction is useful because while Bitcoin fell by approximately 50% from October 2025 to February 2026, options volatility rose to its highest level since 2022. Even during an active squeeze, investors are still selling volatile assets to raise cash. Bitcoin remains sensitive to liquidity stress during these periods.

This pattern also reinforces the long-term nature of Bitcoin in this UK move. Government bond prices are volatile, expectations for interest rate cuts seem further remote, and yields on easily accessible cash are lower than the central bank’s current expectations for inflation. Under these circumstances, Bitcoin begins to look more like an opt-out from the promise of a national currency than pure speculation. It has its own volatility and different sources of risk than those currently facing cash and Treasury bond holders.

The UK regulatory regime makes that discussion easier than it was a few years ago. Awareness of cryptocurrencies is over 90%, with 25% of crypto users saying they would be more likely to invest in them if the market were more regulated, according to the Financial Conduct Authority’s latest consumer survey.

The findings support asset class knowledge and sensitivity to regulatory clarity. This leaves the scale and timing of new demand unresolved.

The UK is also noteworthy outside the UK because the household mechanism is unusually visible. The US still dominates crypto flows, ETF headlines, and dollar liquidity. However, the UK shows pressure points sooner.

When debt mounts, borrowing takes an unexpected turn for the worse, utility bills go up, and large mortgages are headed for reset, this problem will reach your plate sooner. What cryptocurrencies represent is a widespread willingness to treat sovereign banknotes and bank deposits as an imperfect answer to the word “safe.”

Official forecasts are also pointing in the same direction. In its March outlook, before the shock, the OBR had expected 10-year government bond yields to be 4.5% and 30-year yields to be 5.3%, while net public sector debt was expected to rise from 94.5% of GDP in 2025-26 to 96.5% in 2028-29.

The tax burden is expected to rise to 38% of GDP by 2030-31. These numbers show continued fiscal stress, leaving little room for a comforting version of the old strategy of cutting interest rates, calming bonds, and patient savers working together to solve problems.

What does the next 12 months look like?

Each plausible path for next year has a different impact on saving behavior.

The shock wears off, but it doesn’t come back.

The central bank’s 3% to 3.5% inflation range will prove about right in the coming quarters, with utility bills rising and households rebuilding their reserves, even though real profits remain low.

In that version, Bitcoin will gain a narrative foothold, but may not be able to attract large flows. The case is simple. When cash is liquid but loses purchasing power and bonds are no longer benign, non-sovereign assets look easier to justify as part of a broader savings mix.

Energy shock continues

The National Institute of Economic and Social Research has modeled a sustained shock scenario in which UK inflation rises by 0.7 percentage points in 2026, GDP falls by 0.2 percentage points in 2026 and 0.3 percentage points in 2027, and bank interest rates end up around 0.8 percentage points above the benchmark.

Before the latest move, NIESR’s winter forecast had the bank rate at 3.25% by the end of 2026. Taken together, these ranges should maintain a path above 4% even if the shock continues.

That is the scenario most likely to deepen the Bitcoin case. High debt reduces fiscal space. Cash decreases due to rising inflation. Rising long-term interest rates will hit home loans. This combination increases interest in assets outside of national debt, even though Bitcoin itself remains volatile and sensitive to broader market stresses.

Stress in market functioning

The third path would hurt Bitcoin in the short term and strengthen its attractiveness in the long term. A separate bond market note from NIESR warns that a sovereign duration shock could move from a repricing to a financial stability event, requiring central banks to support market functioning even though inflation is still uncomfortable.

That is the institutional contradiction that Bitcoin was designed to solve. It’s also the kind of market period that could still put pressure on Bitcoin if investors rush for liquidity.

This tension explains why the UK’s recent bond movements have been so striking. Business is troublesome. The mechanism is clear. As countries borrow heavily, energy costs rise, inflation picks up again, and households face mortgage resets, the social meaning of security begins to change. The discussion moves from macro theory to monthly outflows and maintenance of purchasing power.

The UK’s recent bond moves could be a development for Bitcoin before many Americans see it as such.

UK data already shows elements of that: £14.3bn borrowed in February, debt to GDP at 93.1%, policy rate held at 3.75%, short-term inflation returning from 3% to 3.5%, accessible cash at 2.02%, 1.8m mortgages scheduled to reset in 2026.

None of these numbers suggest that Bitcoin will win anytime soon. Together, these represent growing pressure on old definitions of safety.

If energy prices remain high, the next utility bill cap rises as futures suggest, and mortgage resets continue to suffer from high yields and slow interest rate relief, more savers may decide that cash and government notes can no longer solve the whole problem.

(Tag Translation) Bitcoin