If you want to understand the AI and data center boom in 2026, look no further than announcements of GPUs, megawatts, and backlogs.

Look at the bond market.

This article first appeared in Miner Weekly, Blocksbridge Consulting’s weekly newsletter featuring the latest energy, computing, infrastructure, and data analytics news from The Energy Mag. The original article can be found here.

Over the past 12 months, over $33 billion in long-term senior debt has been issued by a small list of Bitcoin mining/AI infrastructure companies, utilities, and power companies. except Convertible banknotes. This is not equity dilution. Debt is hard: fixed coupons. Actual maturity. Actual interest expense.

And the difference between who pays 4% and who pays 9% tells you pretty much everything about how the market is taking on the data center arms race.

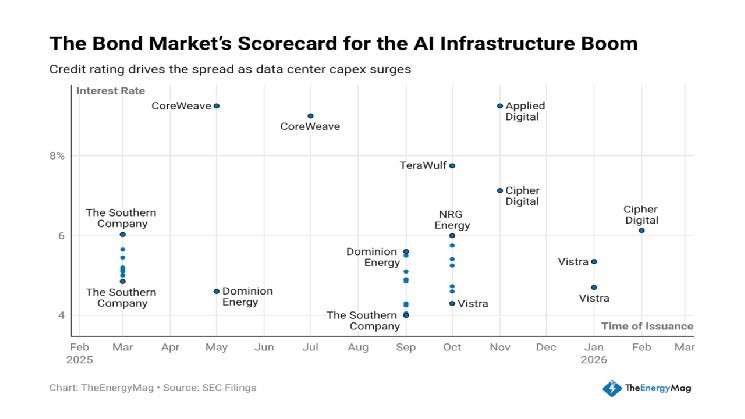

9% Club: AI and Bitcoin Infrastructure

Capital is not cheap in the high-yield sector.

CoreWeave print:

- $2 billion at 9.25% (May 2025)

- 9.00% to $1.75 billion (July 2025)

Applied Digital: $2.35 billion at 9.25% (November 2025)

TeraWulf: $3.2 billion at 7.75% (October 2025)

Crypto Mining (NASDAQ: CIFR):

- 7.125% to $1.4 billion (November 2025)

- $2 billion at 6.125% (February 2026)

Cipher’s February contract is interesting. Despite doubling its issuance to $2 billion, prices improved by 1 percent in just three months. This suggests that there is still demand for “compute-backed” credit, especially where colocation leases and power contracts are in place.

But zoom out and compare this to regulated utilities and power producers.

4-5% world: incumbent energy giants

Now look at the other side of the ledger.

Dominion Energy (NYSE: D): Multiple tranches of 4.6% to 5.65%

NRG Energy (NYSE: NRG): Mostly 4.7% to 6.0%

Vistra Corp.: $2.25 billion at 4.70% and 5.35%

Southern (NYSE: SO) Company: Several issuances clustered around 4%-5.5%

Constellation Energy (NASDAQ: CEG): $2.75 billion in January 2026, multi-tranche, primarily less than 5% depending on maturity.

Same macro environment. The same Treasury curve. Credit pricing varies.

The message from lenders is clear. Regulated loads and contracted generation are still treated as infrastructure. AI and Bitcoin are still treated as growth credits, even when tied to long-term offtake agreements.

The story of spreads is the story of credit ratings.

If we arrange these issuers by coupon, we get a rough risk ladder.

- 4%-5%: Regulated utilities and diverse power producers

- 5%-6%: More powerful independent generator

- 6%-9%: Bitcoin miners and AI infrastructure builders

Regulated or established utilities tend to be located in the investment grade world, with long operating histories, predictable (and often regulated) cash flows, and deep institutional demand for paper.

On the other hand, newer “computing” companies, especially those that are still expanding, building, or proving the durability of their customer base, typically borrow as high-yield/speculative-grade credit. Even when you actually have a contract in place, the market is still pricing in execution risk, refinancing risk, and the reality that capital expenditures will eat up cash before they generate cash.

Why am I accruing so much debt so quickly?

The common topic is not crypto cycles. That’s the demand for data centers.

Utilities are openly revising their capital plans upward. Southern is currently $78.1 billion The investment plan through 2030 is $15.9 billion in 2026 alone, explicitly citing projected increases in load from data centers. Dominion similarly warned that it expects to issue billions of dollars in long-term debt ($6 billion to $9.5 billion in 2026) to support infrastructure expansion by large new data center customers.

On the AI side, the logic is simpler. Securing power first and thinking about monetization later.

For miners moving to HPC, assuming they still have cash flow from Bitcoin mining, the debt stack is becoming a bridge between traditional Bitcoin cash flow and future AI tenants. For AI players like CoreWeave, it’s about scaling ahead of revenue realization under hyperscaler contracts.

Bubble or capital spending supercycle?

That’s the bigger question hanging over all of this.

If demand for AI holds, these coupons may seem perfectly reasonable. Debt refinancing will be reduced. Assets are valued. Power shortage becomes a bottleneck.

But if demand for AI cools, or if hyperscalers’ ramp-up loses momentum, the 7-9% debt stack tied to merchants’ exposed computing assets could quickly become a burden, especially since there is little financial cushion for Bitcoin mining.

Please remember. Most of these maturities are clustered around 2030-2036. The age of infrastructure is not far away. This is no longer just a matter of power. It’s about the balance sheet.

regulatory news

- President Trump announces US tariff rate will increase from 10% to 15% worldwide

- President Trump to announce data center energy deal during State of the Union address

Hardware and Infrastructure News

- Bitcoin difficulty increases by 15%, hash price drops below $30/PH/sec

- Canaan acquires stake in Texas Bitcoin Mines Cipher Inc. in $40 million stock deal

- Bitfarms wins local approval to move forward with Pennsylvania AI data center project

- Wenatchee, Washington fire linked to Bitcoin mining activity

corporate news

- Blue Owl struggles to pay off $4 billion in debt CoreWeave AI Data Centers

- Bitdeer wipes out Bitcoin reserves while refinancing high-cost convertible debt

- Cipher Mining rebrands to Cipher Digital to double AI data center leases

- Cipher CEO establishes new 10b5-1 plan for up to 1.5 million CIFR shares

- NextEra Energy raises $2 billion in equity units to fund power projects

financial news

- Tether reloads on Bitdeer with $42 million buy after selling near 2025 peak

- CoreWeave seeks $8.5 billion in financing as AI infrastructure debt mounts

- Blackwell Ramp drives AI data center sales to NVIDIA’s revenue of over $216 billion

- Hut 8 pledges 4,533 Bitcoins for $200 million Coinbase loan $BTC slide

- US Bitcoin exceeds 6,000 $BTC Holdings after Q4 production, ATM purchases