Vitalik Buterin said over the weekend that Ethereum needs a “better decentralized stablecoin,” arguing that the next iteration must solve three design constraints that today’s model continues to circumvent. His comments landed alongside MetaLeX founder Gabriel Shapiro’s broader assertion that Ethereum is increasingly becoming a “contrarian bet” against what much of the venture-backed cryptocurrency stack is optimized for.

Shapiro explained this divide in ideological terms, saying, “It is becoming increasingly clear that Ethereum is a contrarian bet to much of what crypto VCs are betting on,” citing “gambling,” “CeDeFi,” “custodial stablecoins,” and “neobanks” as centers of gravity. In contrast, he argued, “Ethereum triples down on subverting power to enable sovereign individuals.”

Why Ethereum doesn’t have a decentralized stablecoin

Mr. Buterin’s criticism of stablecoins begins with what they are stabilized against. “Tracking the US dollar is fine in the short term,” he said, but suggested the longer-term version of “nation-state resilience” refers to one that does not rely on a single fiat currency “price ticker.”

“Tracking the US dollar is fine in the short term, but part of the vision of nation-state resilience is that it should even be independent of price tickers,” Buterin wrote. “If you think about it over a 20-year timeline, what happens if we have even moderate hyperinflation?”

This premise shifts the stablecoin problem from simply maintaining a peg to building a reference index that can withstand changes in the macro regime. In Buterin’s framework, that is one of the “problems.” Even if tracking the US dollar remains relevant in the short term, at least the north star is to identify an index that is “better than the US dollar price.”

The second issue is governance and oracle security. Buterin argued that decentralized oracles “must not be acquired for large sums of money,” or the system would be forced into unattractive trade-offs that would ultimately fall on users.

“Without (2), you would have to ensure acquisition cost > protocol token market capitalization, which means extraction of protocol value > discount rate, which is very bad for users,” he wrote. “This is a big part of why I am always critical of financialized governance. There is no inherent defense-attack asymmetry in governance, and high levels of extraction are the only way to stabilize it.”

He linked it to a long-standing discomfort with token holder-driven control structures that resemble a market for influence. In his view, “financialized governance” tends toward systems that must continually extract value to protect themselves, rather than relying on structural advantages that make attacks significantly more difficult than normal operations.

The third problem is mechanical. Staking yield competes with decentralized stablecoins for capital. If stablecoin users and collateral providers are implicitly giving up a few percentage points in return compared to staking ETH, Buterin said that’s “pretty bad” and suggested it will be a permanent headwind unless the ecosystem changes how yield, collateral and risk interact.

He presented what he described as a map of a “sphere of solutions”, which he stressed was “not something I would endorse”. The paths range from compressing staking yields to “enthusiast levels,” to creating staking categories with comparable returns but without the same slash risk, to “making slashable staking compatible with ease of use as collateral.”

Buterin also clarified what “risk reduction” actually means in this context. “If you try to reason this out in detail, remember that the ‘slash risk’ to be wary of is both self-contradiction and being on the wrong side of inactive information leaks, i.e. participating in a 51% censorship attack. In general, we think too much about the former and not enough about the latter.”

This constraint also affects liquidation dynamics. He said that stablecoins “cannot be secured with a fixed amount of ETH collateral,” that large drawdowns require aggressive rebalancing, and that designs for yield from staking must consider how yields turn off or change in times of stress.

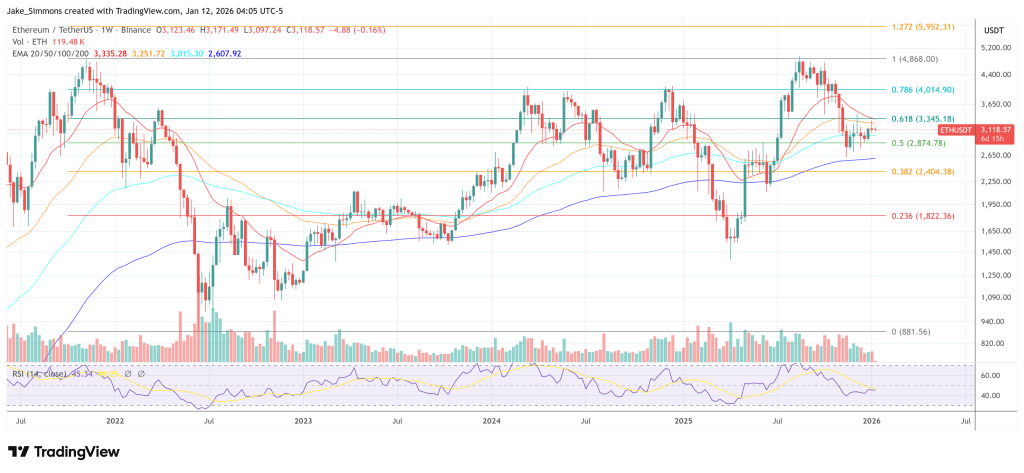

At the time of writing, ETH was trading at $3,118.

Featured image created with DALL.E, chart on TradingView.com

editing process for is focused on providing thoroughly researched, accurate, and unbiased content. We adhere to strict sourcing standards, and each page is carefully reviewed by our team of top technology experts and experienced editors. This process ensures the integrity, relevance, and value of your content to your readers.