Bitcoin (BTC) April 2024 cut block reward will be halved from 6.25 BTC to 3.125 BTC, compressing hash prices and forcing Bitcoin miners to rethink their business models.

Instead of waiting for the fee market to rescue margins, the largest operators have begun signing deals to lease infrastructure to AI tenants.

Core Scientific has committed to supply 500 megawatts of power to CoreWeave for $8.7 billion over 12 years. Cipher locked in 168 MW with Fluidstack for $3 billion over 10 years with Google’s backstop obligations.

These deals are based on the calculation that the same inputs that power SHA-256 ASICs can generate more revenue per megawatt-hour if they are directed toward high-performance computing.

The question is how much non-Bitcoin revenue miners will need to relieve selling pressure on government bonds, what will happen to the network’s hashrate as capacity shifts, and which operators have the balance sheets to perform.

Bitcoin miners control everything needed for AI computing, including cheap electricity, industrial land, cooling infrastructure, and operational expertise.

The revenue curves are different. Mining ties revenue to hash price and coin price. AI colocation delivers contracted dollar revenue per kilowatt month. What matters is the margin comparison in dollars per megawatt hour, and when the hash price is compressed, the unit economics favor hosting.

Security budgets under pressure

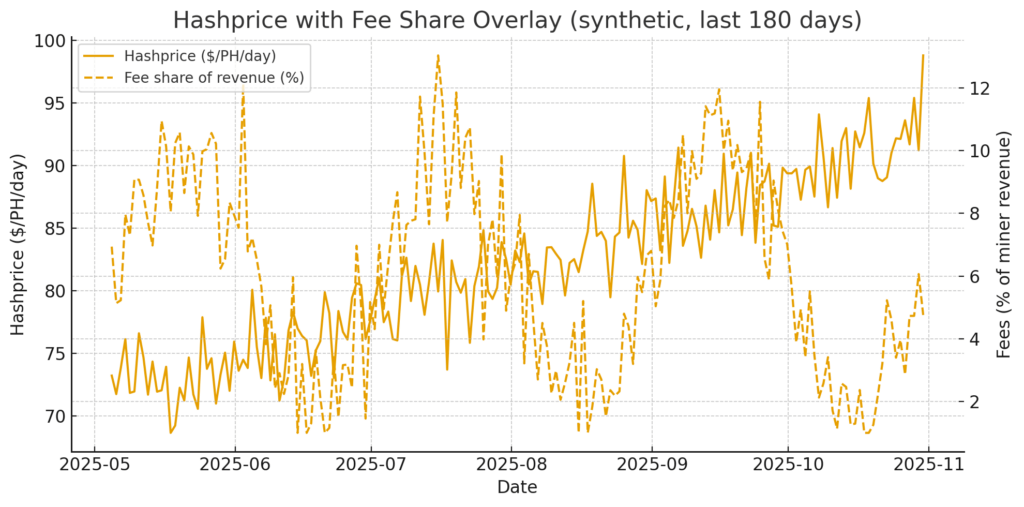

Hashprice measures a miner’s revenue per petahash per day. When it falls, miners shut down their machines or sell their Bitcoins to cover legal costs.

The network’s security budget is equivalent to block subsidies plus fees in Bitcoin terms, but its dollar value has become more volatile since the halving.

A temporary spike in fees when Runes launched during the halving block showed how on-chain demand can impact hash prices, but outside of those spikes, fees have been modest.

Electricity prices are fixed in dollars and profits are earned in Bitcoin. If hash prices remain at $50 per petahash per day, a modern fleet of Antminer S21 class machines running at 17.5 joules per terahash will generate approximately $119 per megawatt hour.

After subtracting the $50 per MWh electricity price, the cash margin is $69 per MWh. The model is operational, but just barely.

If you increase the hash price to $75 per petahash per day, the revenue increases to $179 per MWh, giving you a cash profit of $129 per MWh.

The difference between survival and profitability is narrow and depends on factors outside the miner’s control, such as BTC price, network difficulty, and fee speed.

AI hosting utilizes the same infrastructure that runs ASICs and offers a solution with dollar-denominated contracts that do not fluctuate with hash prices and are locked in over multiple years.

Where Bitcoin miners meet AI

Bitcoin miners and AI operators require the same infrastructure, including affordable power, proximity to substations, industrial cooling, fiber optic interconnects, and expertise to maintain uptime.

Core Scientific’s CoreWeave contract costs about $121 per kilowatt for hosting. Cipher’s Fluidstack contract costs approximately $149 per kW per month.

These are contracts signed with creditworthy counterparties and are not ambitious projections. The revenue structure typically separates hosting fees and power costs, as the tenant reimburses the power consumed and the operator earns a fixed fee per kilowatt.

This transfers commodity risk to tenants and transforms miners’ revenue into infrastructure-as-a-service.

Assuming a power usage efficiency of 1.2, a rack rate of $120 to $180 per kW per month corresponds to a facility revenue intensity of approximately $139 to $208 per megawatt hour.

Since electricity is passed through, much of its revenue is allocated to cash flow excluding non-electricity operating expenses.

Compare this to SHA-256 mining at $75 per petahash per day. Revenue intensity is $179 per MWh, but every dollar of electricity costs are paid upfront.

The hosting model eliminates Bitcoin price volatility and fee volatility, and instead gives you multi-year visibility. For debt-ridden miners, their cash flow profile favors financing.

Unit economics and financial policy

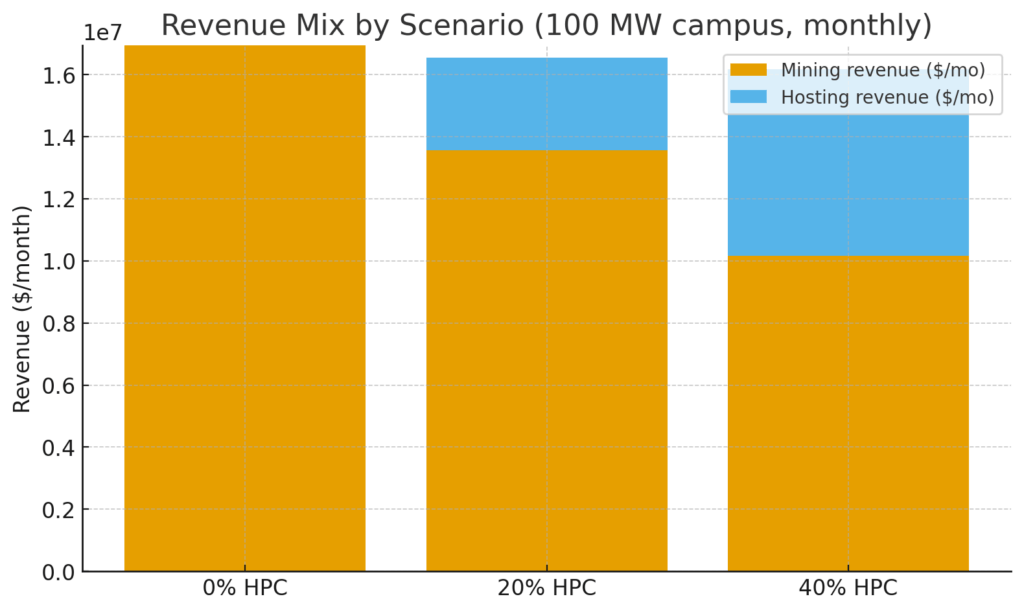

A 100 MW site running SHA-256 at an electricity rate of $75 per petahash per day and $50 per MWh would generate a cash margin of approximately $129 per megawatt hour, which works out to approximately $11.3 million per year.

If you lease the same 100 MW to an AI tenant for $150 per kW per month, your facility revenue intensity will be approximately $174 per MWh.

If the tenant pays for the electricity, the operator keeps most of it as margin. The hosting structure provides significantly more cash flow per megawatt when hash prices fall or electricity prices rise.

Financial policy is important. MARA Holdings held as much as 52,000 BTC of Bitcoin, but sometimes did not sell it at all. Riot Platforms sold 465 BTC for approximately $52.6 million in September 2025 to fund expansion. CleanSpark continues to ramp up, increasing its funding to over 13,000 BTC.

Everyone faces the same statutory expense base, including electricity bills, debt repayments and salaries. Hosting revenue changes the equation. If a miner generates $15 million per year from 100 MW of AI colocation, that’s $15 million without having to sell any Bitcoin.

The Treasury can maintain coin denominations without running out of cash. When hash prices are compressed, that buffer allows miners to weather weak environments without being forced to sell, thereby weakening the selling pressure that typically occurs after a halving.

Less BTC sent from miner wallets to exchanges means less marginal supply.

Hashrate migration and network impact

If a significant share of the hashrate is migrated to AI hosting and not backfilled, the network hashrate will decline until retargeting becomes difficult and equilibrium is restored.

The security budget in BTC remains unchanged and blocks will continue to generate 3.125 BTC plus fees, but lower hashrates may increase attack costs.

The back side is mechanical. Assuming Bitcoin prices and fees remain constant, a lower network hash rate means a higher hash price for the remaining miners.

In a scenario where 10% of the world’s hashrate migrates to AI hosting over 18 months and the network hashrate drops by approximately 10%, difficulty will be adjusted downward and hash prices for the remaining miners will increase proportionately.

Miners who stay with SHA-256 will capture the upside, while miners who pivot to AI will secure their contracted dollar revenue.

There is a trade-off between Bitcoin exposure and cash flow certainty. Fees complicate analysis. If the fee market becomes active through runes, layer 2 payment traffic, or payment volume, hash prices can rise rapidly.

Miners who migrate from SHA-256 to AI hosting miss out on its benefits. AI contracts provide downside protection but limit participation in fee revenue surges.

The optimal strategy will depend on each miner’s cost structure, balance sheet, and view of Bitcoin’s fee trajectory.

Who wins and what breaks?

Carriers with very low power costs, scalable interconnections, and capital flexibility are the best choice. Core Scientific’s post-bankruptcy reorganization pivot to HPC hosting illustrates how a balance sheet reset can enable strategic repositioning.

Google-backed Cipher trading demonstrates the importance of trustworthy counterparties. Bitdeer, Iris Energy, TeraWulf, and CleanSpark have all announced their intention to leverage HPC, reflecting the industry’s growing recognition that AI demand can monetize pent-up power capacity.

The risks are real. GPU cycles change, miners spend capital expenditures on infrastructure, and value can be lost. Counterparty risk is a concern for smaller AI startups without strong balance sheets.

In Texas, grid policy over heavy loads is intensifying. In Texas, ERCOT’s interconnection queues are long, and capacity additions are lagging behind demand growth.

Miners that lease interconnection capacity to AI tenants may struggle to scale back once Bitcoin economics improve.

Interconnection queues are more important than popular discussion acknowledges. Miners with 200 MW of contracted power and grid interconnection approvals can switch between SHA-256 and HPC based on economics.

Miners waiting in ERCOT’s queue cannot earn money from the site until they are approved, which can take years. Miners who moved early gained options that miners who moved later did not.

What to watch in 2026

Over the next year, it would be wise to track power purchase agreement announcements, ERCOT interconnection milestones, miner guidance on non-BTC revenue mix, and Bitcoin fee velocity.

ERCOT’s capacity report provides context for the shortfall in Texas, where large load actions are concentrated. Interconnect capacity is becoming a binding constraint.

Pricing trends will determine whether continuing to use SHA-256 provides the same benefits as AI hosting. If rune or layer 2 traffic drives continued price increases, hash prices could stabilize above $100 per petahash per day, allowing mining to compete with hosting on a risk-adjusted basis.

If prices remain under control, the hosting model wins for cash flow certainty. Miners are hedging. Convert your share to AI hosting while retaining some capacity for SHA-256, preserving your options until the market reveals which model is dominant.

The strategic question is not whether miners will become AI companies, but how they will allocate finite interconnection capacity, power contracts, and balance sheet resources between competing uses.

Winning miners can both maintain SHA-256 operations when the hash price warrants, scale AI hosting as contracts end, and maintain the flexibility to migrate between models as the economy evolves.

The question is whether the Bitcoin mining industry will maintain a disposable identity or become a multi-tenant power monetization layer that happens to protect the blockchain.